2024 Global Oil Supply & Demand Balance Favors The Bulls

We are now halfway through 2023 and as we compiled our global oil supply & demand balance for 2024, we can't help but reach a few very straightforward conclusions:

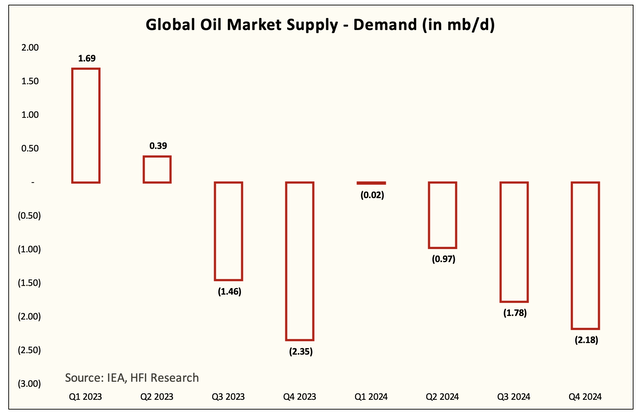

The deficit of H2 2023 will persist into 2024.

US oil production growth or lack thereof is an asymmetric variable for the bulls.

Saudi and Russia's participation is key to maintaining a large deficit this year, but by H2 2024, spare capacity will need to be materially reduced to avoid catastrophe.

Global oil demand growth centered in non-OECD. OECD demand is expected to decline y-o-y in our model.

Despite extremely conservative demand assumptions, we have a material inventory draw in 2024.