The Iran conflict has gripped the global energy markets by surprise, and while everyone fixates on the disruptions to the oil market, the natural gas market is really the one that could catch a lot of people offguard. No, I’m not talking about the European natural gas market where TTF has doubled in just 2 trading days. I’m talking about Henry Hub (US gas market) and the interesting dynamic we are about to see.

Trade Background

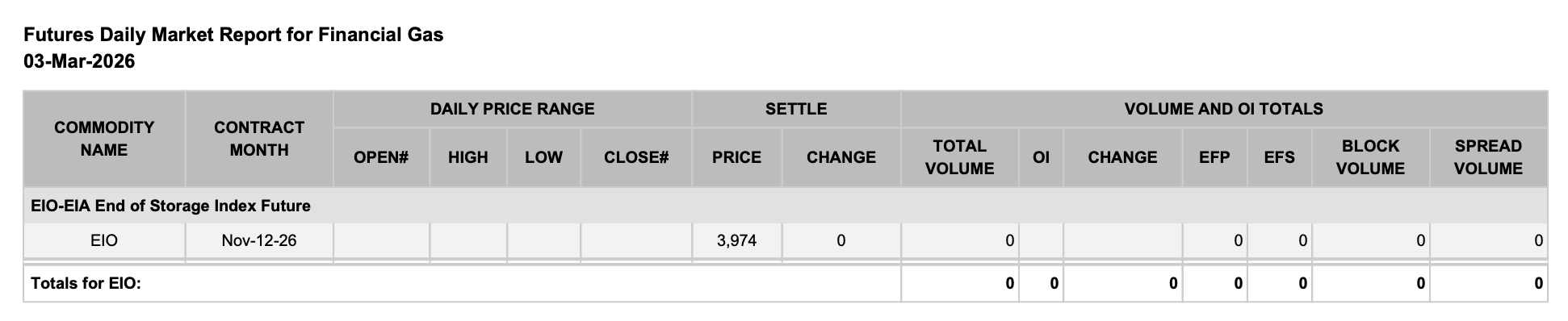

The market believes, rightly or wrongly, that the US natural gas market will be adequately supplied this year. The winter heating demand season is coming to a close, natural gas storage will finish near the 5-year average, and November natural gas storage is headed for 3.974 Tcf.

Source: ICE

The consensus believes that:

The structural demand from LNG/Mexico is already in the balance. No surprise on the demand side until 2027.

Lower 48 gas production will move higher with additional takeaway capacity coming online from the Permian. Higher rig counts in Haynesville should support supply growth.

Higher renewable capacity increase this year will foreshadow the same power burn decrease we saw (for natural gas) in 2025. If natural gas prices are elevated this summer, more gas-to-coal switching will displace more power burn demand.

In 2027, the global LNG market will be in a glut with additional capacity coming online from Qatar pressuring US exports.

These factors will pressure natural gas prices. This is one of the main reasons why we aren’t seeing much higher prices today.

But the geopolitical conflicts that unfolded over the weekend changed all that. In particular, the most notable event was Qatar announcing force majeure on its LNG gas exports. Qatar is the 3rd largest LNG exporter in the world. Most of its contracts are long-term. Qatar exported ~90% of its LNG capacity to Asia.

With LNG tanker rates spiking amidst the geopolitical turmoil, US LNG gas exports suddenly become the most attractive place to lock in long-term commitments.

Take a stepback and think about this for a moment. Elevated geopolitical conflicts in the Middle East have just demonstrated how vulnerable LNG flows can be. And since natural gas is a time-sensitive commodity (needed during the winter heating demand season), having an adequate supply on time is vital for the buyers.

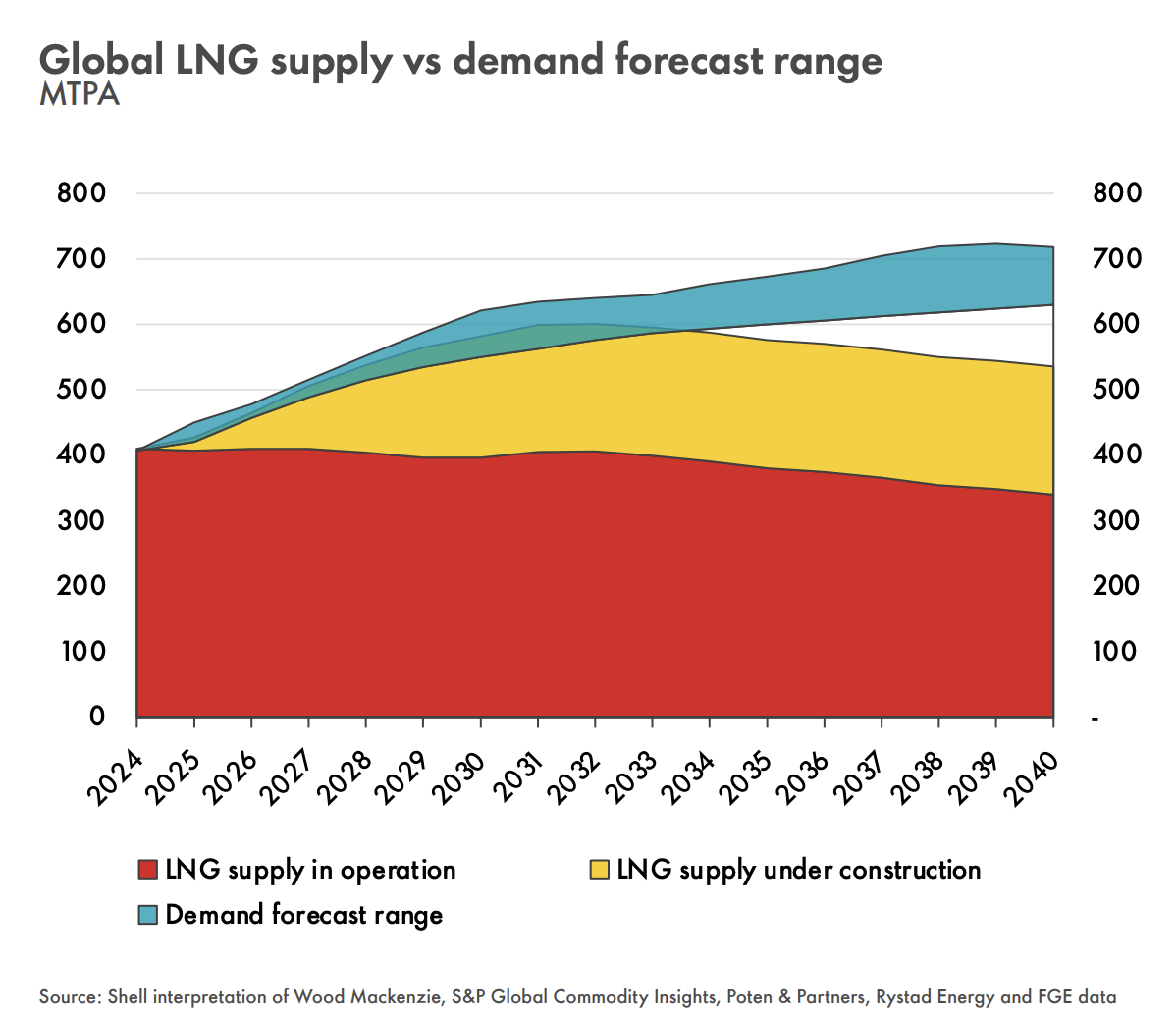

Everyone in the industry expected the global LNG market to be in surplus through 2030. Here was Shell’s 2025 LNG outlook:

As you can see, the demand forecast range varies as it depends on 1) weather, 2) price, and 3) adoption rate. Assuming everything goes perfectly, demand outpaces supplies by 2030. But if any of the steps meet a hurdle, we could see the global LNG market tip into a surplus, which would pressure prices.

Now, couple this outlook with the current anticipated LNG export demand increase in the US, and you can draw an interesting conclusion. Supply uncertainty in the Middle East will prompt buyers to want to lock in long-term contracts with US LNG exporters.

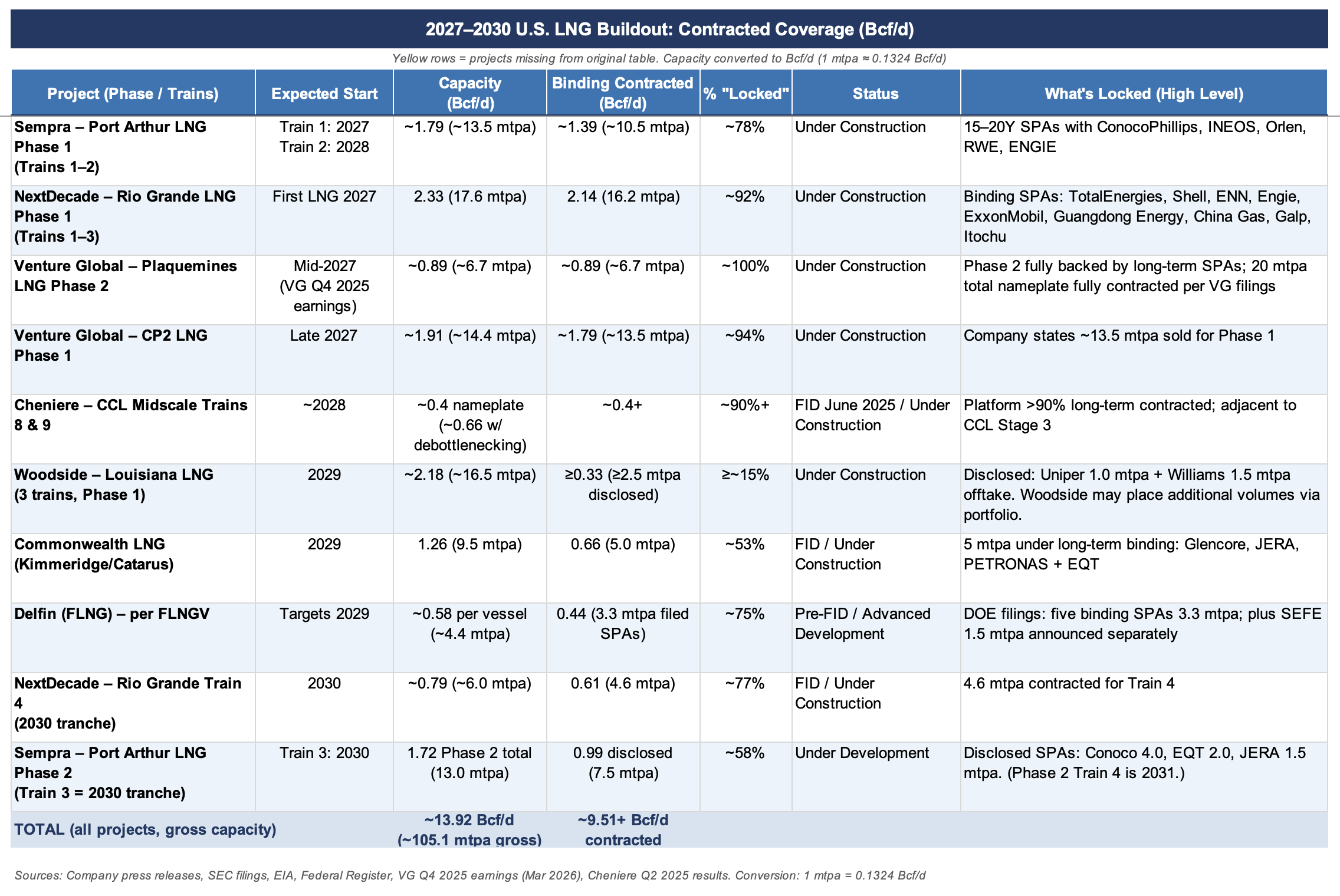

Source: S&P

This insight was first brought to us by Dr. Anas Alhajji, whom we thank greatly for sharing this unique and differentiated take.

Between 2027 to 2030, only 68% of the incoming LNG facility buildout is contracted.

The increasing instability in the Middle East, especially if the conflicts are prolonged, will be very beneficial for US natural gas producers and exporters. The US is already the largest LNG exporter by far. US shale gas producers have some of the best economics in the industry. Not to mention that Permian, the key US shale oil region, is selling natural gas today below $0/MMBtu.

In our view, the Qatar force majeure will have altered the global LNG landscape for the years to come.

Why is this important for the trade setup?