Murphy’s Law: Anything that can go wrong, will go wrong.

Isn’t that the truth in natural gas trading?

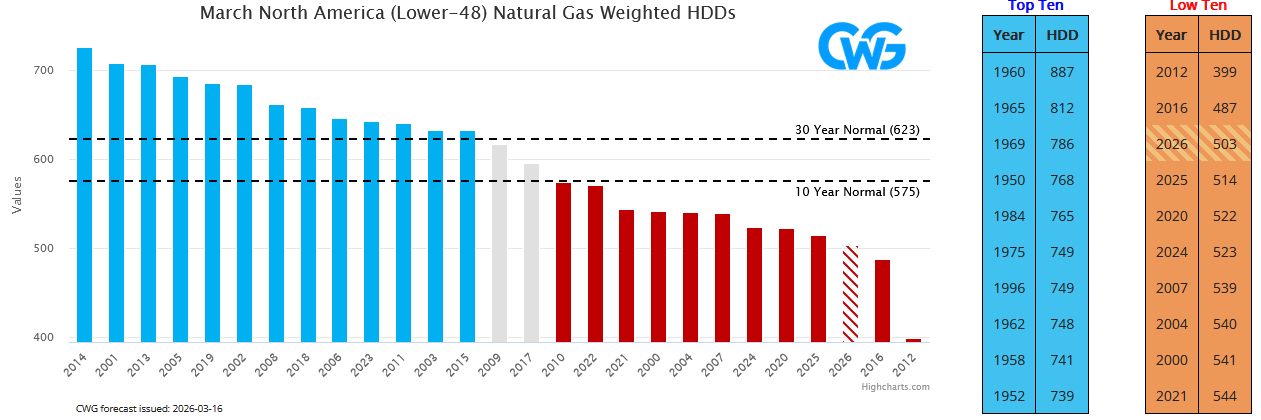

One of the assumptions going into March was that heating demand would at least be better than in 2025.

Source: Commodity Wx Group

Well, sorry for asking for too much. March’s projected heating demand is expected to be lower than in 2025. It is now the 3rd lowest heating demand (March) since 2000.

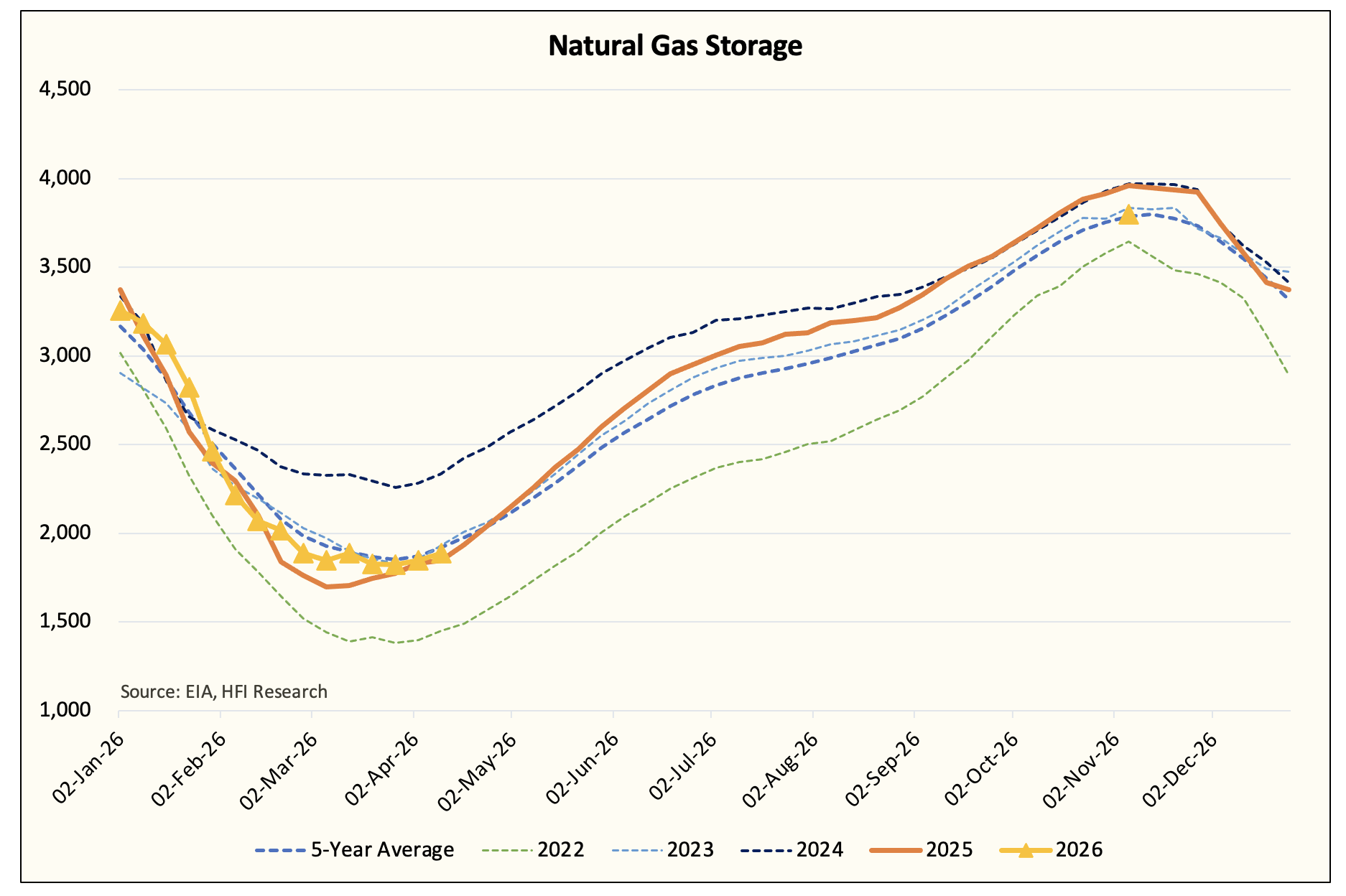

But thanks to better fundamentals, natural gas storage did finish near the 5-year average.

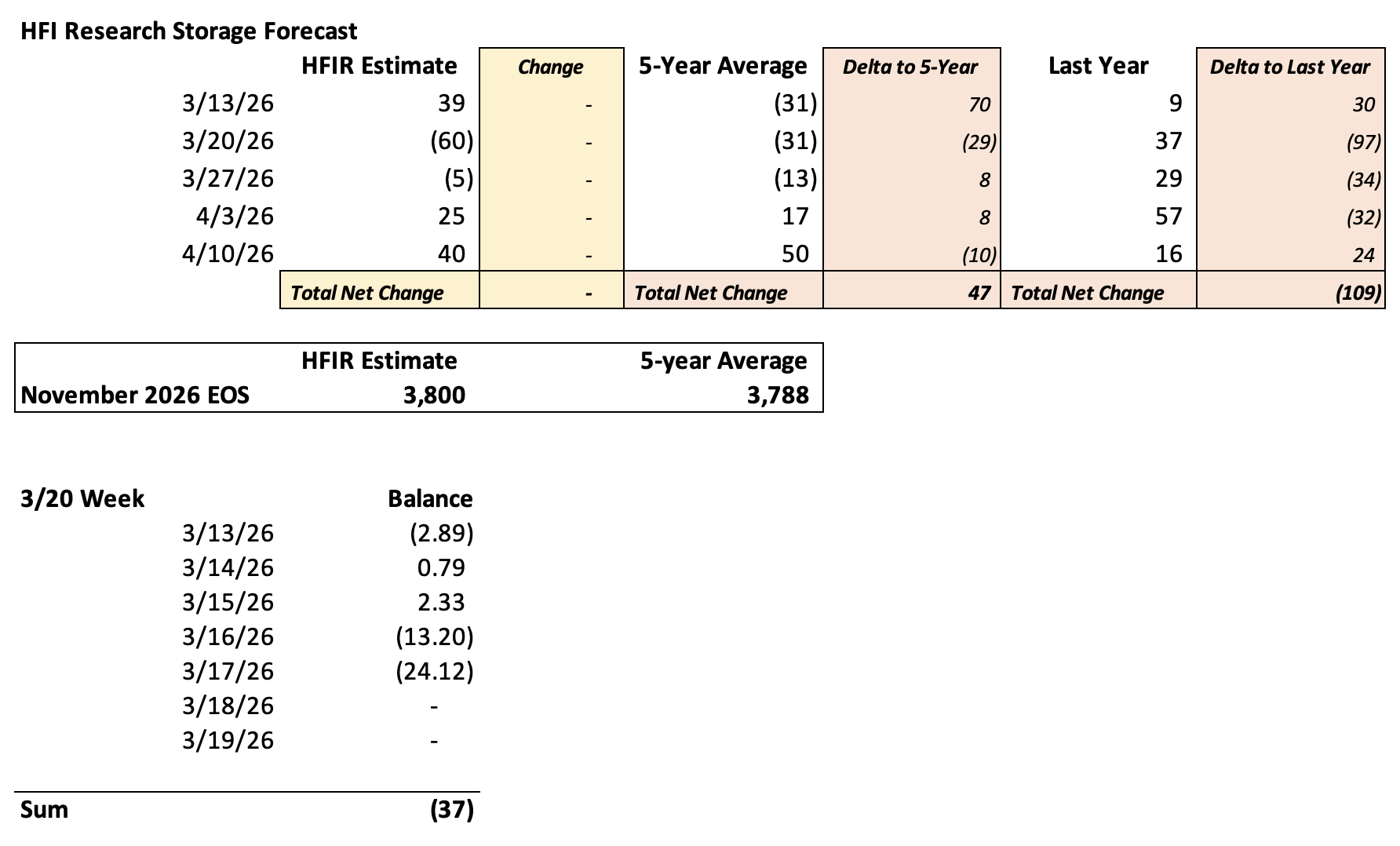

Readers should expect this week’s EIA natural gas storage report to show an injection of ~39 Bcf.

We are projecting November 2026 EOS at 3.8 Tcf, which is slightly above the 5-year average of 3.788 Tcf. If you are wondering why natural gas prices aren’t trading higher, then look no further than this storage projection.

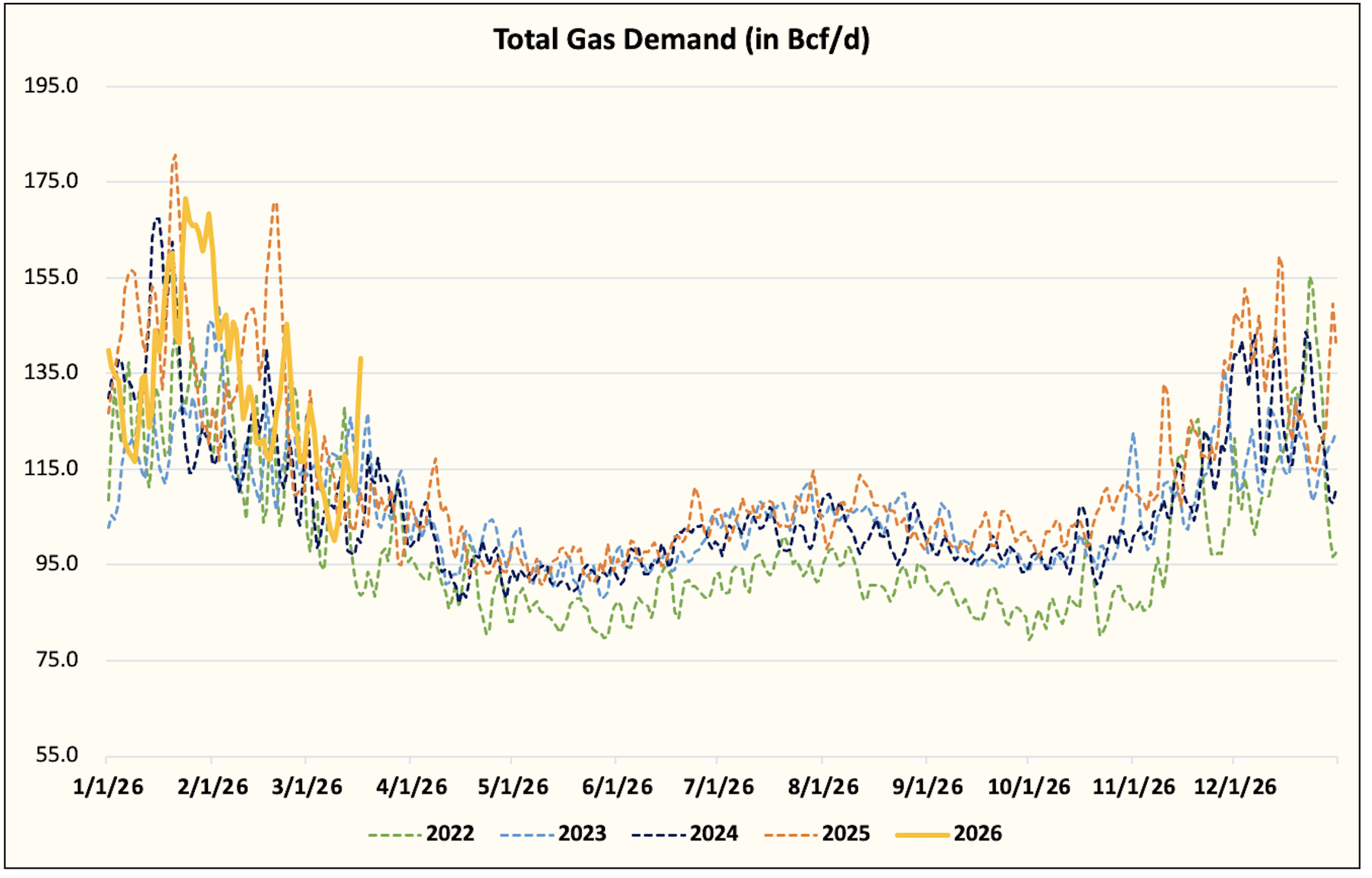

On the fundamental front, we have officially seen the peak in heating demand for this winter. Even if April turns out colder-than-normal, we will not see heating demand get anywhere near the highs we saw in January.

Overall, this winter’s heating demand was slightly below the 10-year average. We managed to reduce the surplus we had at the beginning of this winter back to the norm. Thankfully, a lot of the fundamental forces that drove the tightening will remain favorable for the injection season.