Back On Track, This Is A Good Sign

Product draw, something we've been harping on for weeks, has finally arrived.

Thanks to the large draws in gasoline (-4.5 million bbls) and distillate (-4.1 million bbls), product storage is now in line with 2023.

Rightfully, the market responded with the vanilla 3-2-1 crack spread inching higher despite the +595k b/d rebound in refinery throughput.

Note: Please divide figure by 3 to arrive at 3-2-1 crack spread.

While this was a very positive report, the market will want to validate further the strength we are seeing in products with more consistent product draws. US refinery throughput is finally starting to move up after a long period of low utilization, so if product draws continue with a flat crude storage outlook, then not only will WTI hold the $79 to $80 range, but we see it moving closer to $85 by mid-April.

Looking at our US commercial crude storage projection, we see peak US crude storage upon us:

Next week's preliminary data shows very low levels of crude exports and imports.

But thanks to higher refinery throughput, we see US commercial crude storage peaking around ~450 million bbls. If we are right about US oil production stagnating, then we could easily see a scenario where US crude storage hits low ~400 million bbls over the summer.

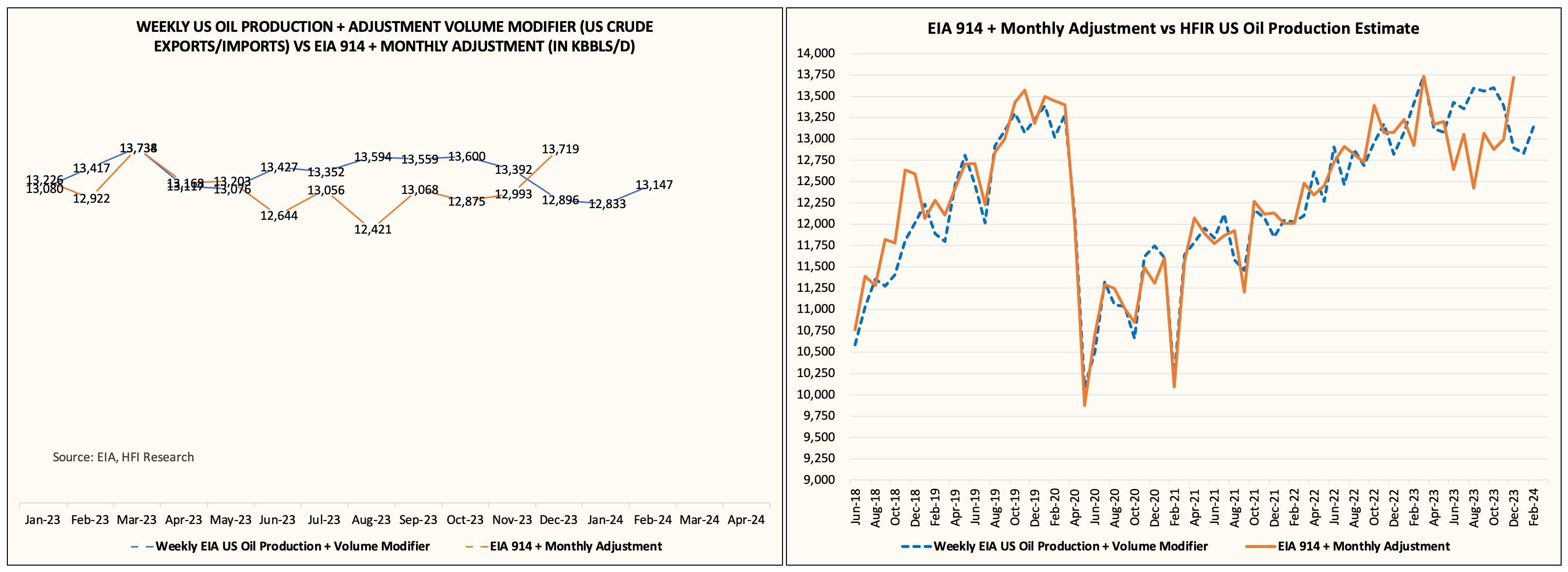

Speaking of US oil production, our real-time data shows high-frequency production right around ~13.15 million b/d for February.

The delta between our figure (~13 million b/d used in the weekly estimate vs EIA's 13.2 million b/d) stems from the "transfers to crude oil supply" line item. Note that we are using ~700k b/d, while EIA is only reporting ~460k b/d for transfers to crude oil supply.

One possible explanation for this is that with natural gas production falling (thanks to low prices), NGL production has also been impacted which reduces the blending element of US oil supplies. Total crude oil supply remains around the ~13.7 million b/d level, so depending on how much EIA uses for transfers to crude oil supply, US oil production will vary.

Note: Higher transfers to crude oil supply lower implied US oil production and vice versa.