December Oil Data So Far Is Quite Revealing Of Where We Are Headed

We are halfway through December and there are some data points that really show the true color of the oil market. For starters, we are still dealing with a minor contango in the 1-2 month Brent timespread. But as readers will note, the 2-3 month and the months following that are back into backwardation. We think the temporary weakness in the 1-2 is not an illustration of what's to come, while the latter part of the curve is a better reflection.

As you will see in the data we share in this article, there are some very interesting developments going on with the oil market heading into 2023.

Unfortunately, before we begin, we have to revisit 2018 one more time. The resemblance to 2018 this year is quite uncanny.

Midterm elections

US SPR release vs Iran sanction waivers

Geopolitical uncertainty from Russia/Ukraine compared to Iran sanctions

A global macro slowdown from Fed raising interest rates vs China/US trade war

Fed starting QT

But there is one key fundamental difference that has separated the two years. The oil market is in a structural deficit.

Source: IEA

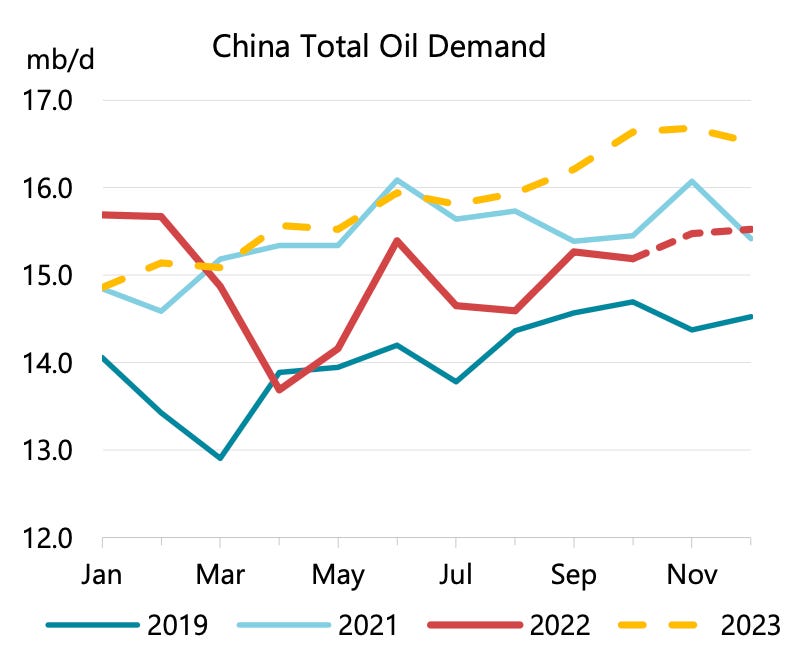

As you can see in IEA's latest oil market report, oil market balances flipped from a steep deficit in 2021 to a minor build starting in Q2. The delta in this balance flip is largely because of China's COVID policy, which is in the process of being lifted entirely.

Source: IEA

You can see this best illustrated in the y-o-y demand decline that started in April when Shanghai was entirely locked down.

Moving forward, with China now lifting COVID restrictions, China's oil demand is going to pop and it will rise much faster than the market is expecting. Why am I saying this? Because China's crude imports are surging for December and once refined product inventories are drained, the incoming buying demand will ripple across the financial market.

This is going to be a key tailwind for the oil market going forward because again, the only reason why oil balances were weak in 2022 was because of China's demand drop y-o-y.

In addition to the return of China's oil demand, OPEC+ crude exports are finally starting to drop. Russia's crude exports are down ~700k b/d m-o-m, and OPEC+ crude exports are down ~1 million b/d.