The oil market is entering an interesting dichotomy. On one end, visible inventory figures like the one from EIA show an unbelievably bullish setup going into the summer draw months.

Crude Storage

Crude + 3 Products

On the other end, high-frequency data shows that there are inventory builds in non-OECD, and global oil inventory balances are still higher YTD.

Global

Source: JPM

OECD

Source: JPM

But in light of the contradiction in the two datasets, one question we must ask is, "Dude, where's the oil?"

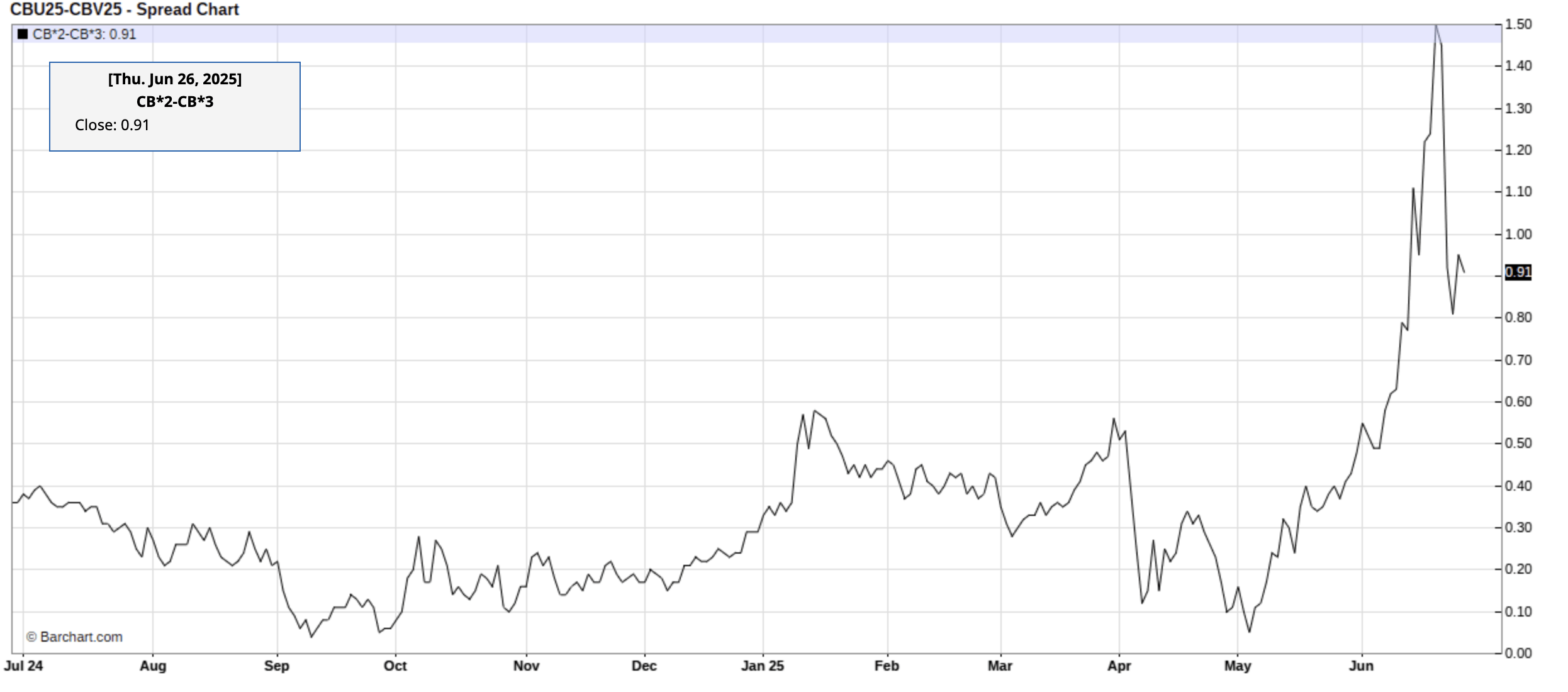

Because let's face it, non-OECD inventories are murky at best. They aren't from official government sources and are subject to change after the fact. And even after the geopolitical risk premium evaporated from the oil price, timespreads remain steeply backwardated.

Source: Barchart.com

This is despite the fact that OPEC+ crude exports are higher month-to-date vs May by ~800k b/d. And if the global oil market is indeed "massively" oversupplied like the IEA and sell-side analysts contend it to be, where's the oil?