In the past 48 hours, we've had:

Possibility of tariffs going on Mexico and Canada only to have it delayed by 30 days.

"Strong" sanction enforcement on Iran being announced.

US/China trading tariffs.

Russia saying it is ready (along with OPEC+) to increase production in April.

Weather model roulette, first showing signs of a polar vortex over the weekend, and now the models are saying this is less of a possibility.

It's safe to say that we nailed it when we wrote in our WCTW on Jan 21, 2025, titled, "More Noise Than Ever." But like I wrote at the time, it's my job to help you stay on track on the things that matter especially when it comes to energy investing.

This week's WCTW should deliver on that. The important things in energy investing continue to be:

An intense focus on non-OPEC supply growth, namely the US.

Global oil demand.

Energy stock-specific fundamentals.

The underlying supply & fundamentals (near-term) for both oil and natural gas.

I hope for the next 4 years, the mixture of both short-term and medium to long-term oriented articles will help you navigate what I think will be best described as "extremely noisy."

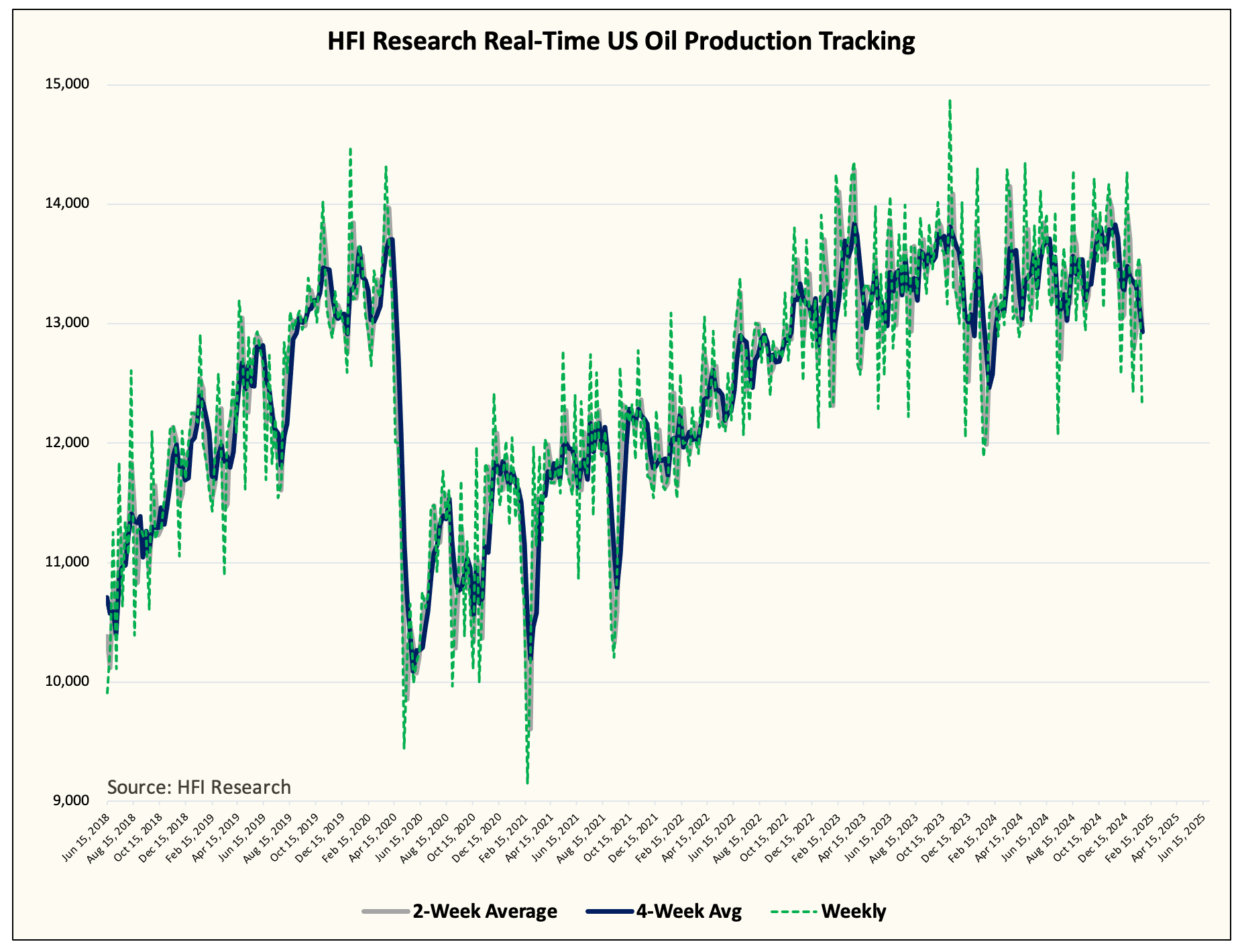

Non-OPEC Supply Story #1: US Oil Production

EIA 914 was published last Friday with the headline US oil production in November coming in at 13.314 million b/d down from 13.436 million b/d in October.

The decline came mostly from the Gulf of Mexico (now called Gulf of America). The decrease was 108k b/d. Outside of that, Texas saw a month-over-month decrease of 70k b/d and New Mexico saw a decrease of 38k b/d.

The adjustment factor in the EIA PSM came in at +390k b/d following October's -145k b/d. Total crude supply in November came out to 13.704 million b/d or smack in line with our projected figure.

Using the 3-month average, US oil production came in at ~13.294 million b/d or right in-line with where we had the weekly US oil production figure for November.

Looking ahead, our real-time US oil production proxy shows that November was the peak in US oil production.

At the moment, US oil production has fallen to ~12.5 million b/d last week due to the colder-than-normal weather. January production is currently averaging ~12.75 million b/d after December averaged only ~13.05 million b/d.

For the EIA 914 report for December (published at the end of February), we expect EIA to report 13.3 million b/d or in line with November production, but the adjustment figure will be -250k b/d reflecting the overstated US oil production level.

This is our current forecast for US oil production for 2025: