For Oil Bulls, It's All About Surviving Q1

I have good news and bad news. Let's start with the bad news first:

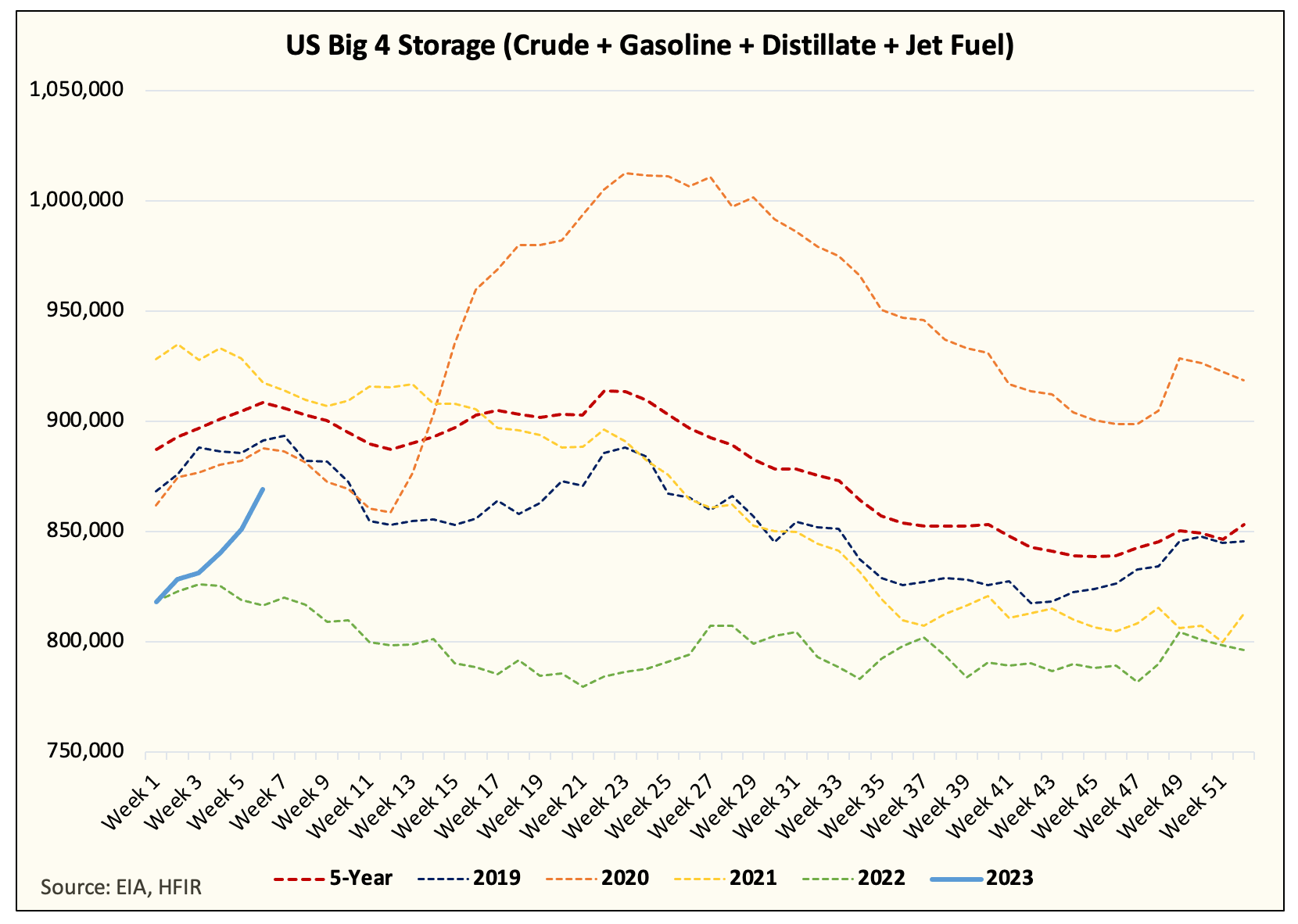

US oil data has been very bearish. Here's a chart illustration:

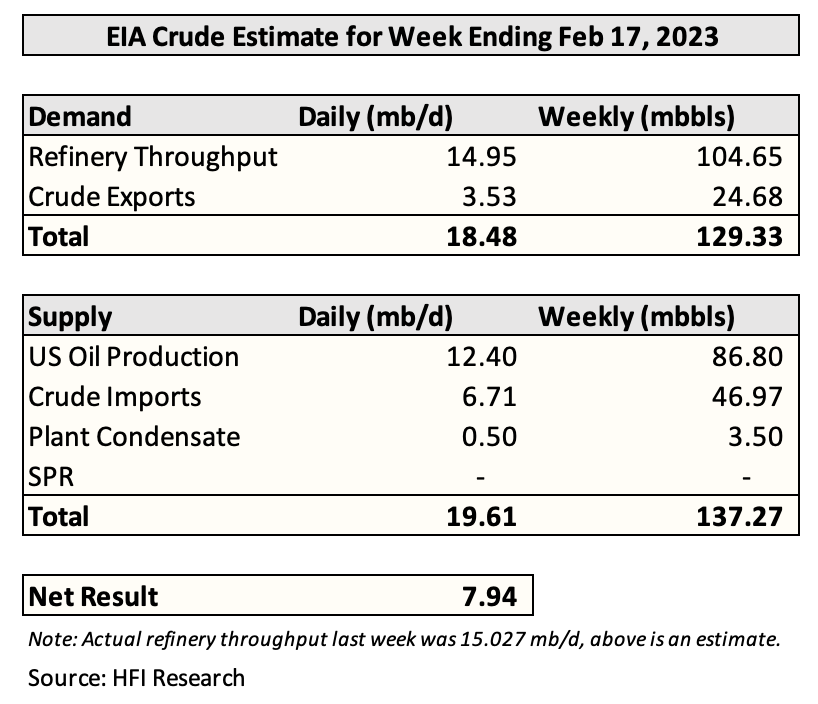

Next week's implied crude storage figure isn't likely to get any better.

This is a preliminary estimate. Finalized estimate will be out later this week.

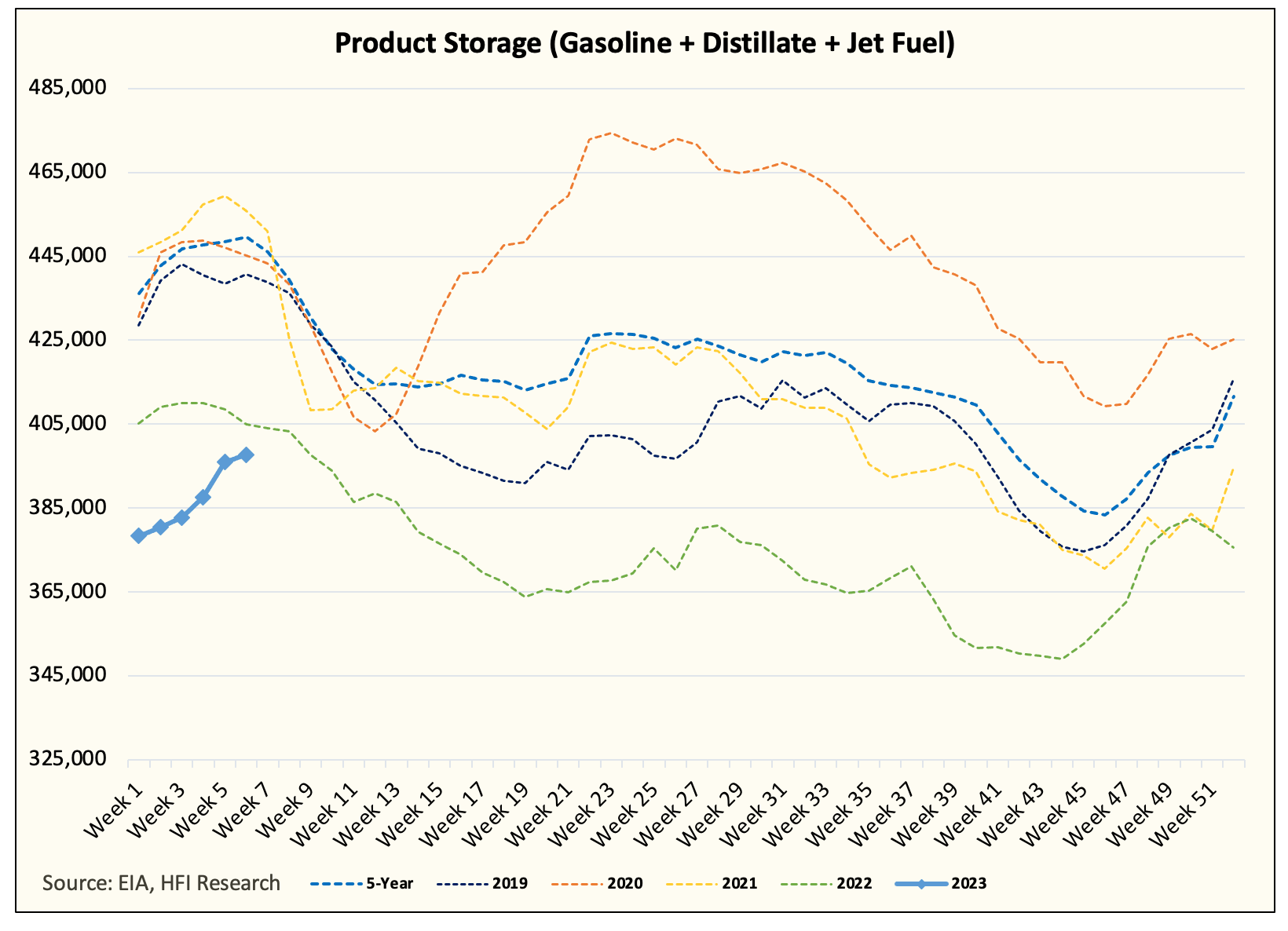

US implied oil demand remains weak.

While this is clearly bearish, readers should note that this was expected. As we entered into 2023, we wrote here and here about the importance of surviving Q1. Inventories were expected to build, so none of this is a surprise. And while the pace of the build, especially crude (more on this later), is clearly bearish, we do hope the next segment gives you a better insight into how we are thinking about the path going forward.

Now for the good news:

Despite hefty builds, product storage is finishing just below 2022 levels going into refinery maintenance season.

Starting this week, product storage on a seasonality basis drops ~35 million bbls over the next 6 weeks. Even taking into account some implied demand weakness, we have likely seen a peak in product storage for this year.

The hefty build in US crude storage is a one-off event due to a spike in the modified adjustment. According to our dataset, this is the highest-ever recorded modified adjustment.

You can also see this illustrated in our US oil production tracking sheet:

Notice how after every wild spike, the modified adjustment drops? That's because there is usually some error that occurred in the EIA dataset, and the correction comes in the following weeks.

What's likely going to happen is that EIA will surprise to the downside vs our crude storage build estimate. We've seen this "compensation" mechanism time and time again when the modified adjustment spikes wildly.

Surviving Q1

For oil bulls, the key is to survive Q1. Q1 is showing oil inventories build as expected. Low refinery throughput in the US throughout January coupled with low crude exports have resulted in hefty crude builds. And as we go through the rest of the refinery maintenance season, US crude storage will continue to build.

As of this writing, incoming US crude exports are expected to start trending higher in the coming weeks. China's return to the physical oil market has also cleaned up much of the recent overhang and should result in even higher US crude exports down the road.

So while US crude storage will enter May/June time period at a very high level, the potential draw down the road is equally as great. Our preliminary estimate shows that US crude storage will peak somewhere between ~495 to ~505 million bbls. Afterward, if our implied balance calculation is correct, then US crude will mimic something similar to what we saw in H2 2022 (-0.6 million b/d).

By year-end 2023, we could see US crude storage return to as low as ~400 million bbls.

For now, the key is to survive Q1. We need to see product storage draws in the coming weeks to confirm we are on the right track. In addition, the recent strengthening signs on the physical oil market front are encouraging, but more is needed.

Source: Barchart.com

For readers, higher backwardation + product storage draws will indicate we will indeed see the light at the end of the tunnel. If not, then we have to do a full reassessment.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours.