(Guest Post) China Is Starting To Release SPR

Note: This report is from Dr. Anas Alhajji. He publishes a daily energy report that we find very insightful. Please check him out here.

-----

Summary

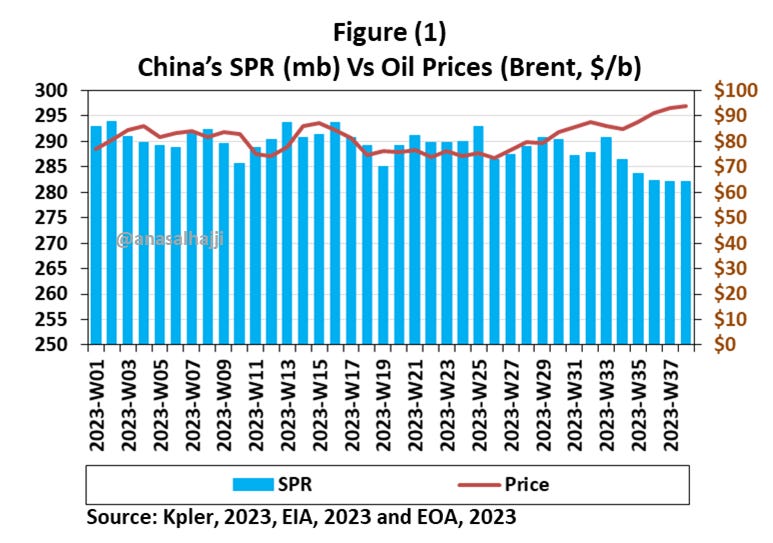

We have been talking about this since last year. Now it is here! China withdrew about 10 mb of crude from its Strategic Petroleum Reserves (SPR), according to Kpler data. Figure (1) above shows trends in China’s SPR and oil prices in 2023 and how the SPR declined as oil prices increased above $73/b.

EOA’s Main Takeaway

Those who followed us for a long time are familiar with our work and predictions. Our modeling shows that China would start withdrawing crude from the SPR at Brent prices around $75. In 2021, the threshold was lower than what our model showed: $70. Now they started the withdrawal at $73.

In a report we published a few weeks ago on the topic, we said that as oil prices rise, the Chinese would lower imports and start withdrawing oil from inventories in an effort to stop oil prices from increasing, and probably lower them. The current withdrawal from the SPR is small, about 10 mb. But we expect this to continue, especially because imports have declined recently. To show how small the amount is, and to avoid any criticism of the chart in Figure (1), we are reposting with the SPR starting from zero (Figure 1-1). Even this chart cannot hide the fact that the SPR declined after oil prices crossed a certain threshold. (Even when we set the price axis from $0 to $350, we can still see the inverse relationship)

Story of the Day

Barron’s: US-Iran Relations are Thawing, which Could Mean Lower Prices

Summary

U.S.-Iran relations seem to be improving, as evidenced by a recent prisoner swap and the U.S.'s decision to release $6 billion in frozen Iranian oil revenue. This might stabilize oil prices. Although Iran's influence in the oil industry is significant, the country is still under U.S. sanctions related to its nuclear program. Experts suggest the U.S. is not strictly enforcing these sanctions to increase global oil supplies, thereby reducing oil prices.

EOA’s Main Takeaway

No. It will not lower prices.

As our readers know from previous reports and charts, Iran has liquidated its floating storage.

Iran is producing and exporting at maximum capacity. In fact, its exports have been declining in recent weeks as shown in Figure (2) below.

It needs massive investment and the help of international oil companies to increase production meaningfully, and that takes time. Two years from now, global oil demand would be about 3 mb/d higher than today, and any Iranian addition would be welcome. With such an increase in demand, why would oil prices decrease from additional Iranian production?

If sanctions are lifted, even partially, economic growth will increase, leading to high domestic oil consumption. That means part of future production increases will NOT go to the international market.

In short, there are no additional oil supplies in the short term. Any additions in the medium and long term would be absorbed by the increasing demand.

News of the Day

Bloomberg: Oil Surge is a Bigger Risk for Europe than for the US, says OECD

Summary

Europe faces a higher risk than the US from rising oil prices, potentially leading to low growth and increased inflation, according to the OECD. Historically, price surges have impacted Europe more since it is a significant energy importer, unlike the US where demand remains relatively unaffected. This distinction is evident in the OECD's recent forecasts, which predict increased growth for the US and reduced growth for the euro area.

EOA’s Main Takeaway

While we agree with this view, the situation globally could be worse as high oil prices and a high US dollar hit poor countries too, leading to lower economic growth, lower imports from Europe, and the possibility of a default on their debt.

For Europe, a recession or low economic growth will reduce the pace of growth in renewable energy and electric vehicles. The irony here is that low oil and natural gas prices will hit growth in renewable energy and electric vehicles through prices (Substitution Effect). High oil and gas prices will hit growth of renewable energy and electric vehicles through lower income and vanishing subsidies (Income Effect). With lower prices, European governments can impose additional taxes and raise prices. In this case, they remain in control of the situation. With higher prices, oil and gas producers are in control. European governments cannot do much except borrow against future income and spend it today on subsidies!

Wall Street Journal: The Unexpected New Winners in the Global Energy War

Summary

Europe is diversifying its gas sources away from Russia, turning to regions like the Sahara and Azerbaijan. In the Sahara, Italy's Eni and Algeria's state firm are tapping new fields, challenging Algeria's traditional alliance with Russia. Algeria is also in talks with European countries and U.S. companies like Chevron and Exxon Mobil for new gas deals. BP is increasing gas production in Azerbaijan. This shift is redefining global gas routes, with Europe importing more from Africa and the U.S.

EOA’s Main Takeaway

Labeling this as “unexpected” is disingenuous! Even before we talked about these issues over a year ago government officials from various European countries vested the Sub-Saharan countries and Azerbaijan. It even resulted is a diplomatic dispute between Algeria and some European countries. It was clear from March 2022 that if the Russian invasion of Ukraine would last to the end of 2022, that the global energy landscape would change and the global energy trade direction would change permanently.

We have covered those changes in more than 15 reports. However, this report ignores the other side of the coin: the truly “unexpected” customers of Russian oil and how Europe continues to import Russian oil indirectly and Russian gas and LNG directly!

Reuters: LNG Crucial to German Energy Strategy, Ministry Official Says

Summary

Germany should retain its LNG capability, established after Russia halted gas supplies, to ensure energy diversity, a senior economy ministry official stated. Despite current lower gas demand, Berlin continues to support these facilities, though there are concerns about their fit in a carbon-free future. Philipp suggested unused LNG terminals could be profitably relocated. Natural gas remains a key transition energy source as Germany moves away from nuclear and coal.

EOA’s Main Takeaway

We have covered this topic extensively in the past from the time the first LNG terminal was planned to the commission of these terminals. We also covered this topic in the Monthly tracker. The latest issue was published last week.

Germany’s LNG terminals are extremely valuable national assets. They will not be moved. In addition, all evidence points to the fact that the US wanted Germany to depend on US LNG. The US will not let Germany replace them with renewables. As Germany attempts to become less reliant on coal it will have to turn to natural gas, and eventually back to nuclear. The energy ministers will keep revising their stories as energy and economic realities force them to do so.

Reuters: China’s Huge Coal Plant Building has Weird Climate Logic

Summary

China is leading global coal-fired electricity generation construction, responsible for two-thirds of the total capacity. Despite this seeming contradiction with its net-zero emissions goal by 2060, there's a broader perspective to consider. China's emphasis on new energy vehicles (NEVs) is rapidly growing, accounting for 36.9% of total vehicle sales in August. This shift from combustion engine vehicles to electric reduces China's reliance on imported crude oil, which currently costs around $250 billion annually.

EOA’s Main Takeaway

Moving from cars that depend on gasoline and diesel to cars that depend on coal is definitely not a climate change solution. But if the coal plants are away from cities and the Chinese government wants to reduce emissions in the cities, electric vehicles are a great way of doing so.

Curbing CO2 emissions to fight climate change is not on China’s priority list. The emissions they are concerned about are in the form of actual pollution—soot emissions that cloud the skies of big cities.

Regardless, we showed in a previous report that China is the largest spender on renewable energy in the world. Looking at its spending in 2022 and the first half of 2023, there is no way that China can achieve net zero by 2060, not even this century. It will take 2011 years, and that assumes every wind and solar installation will stay forever! This means there is no way that China will achieve NET ZERO.

EIA: China Crude Imports at Record High

Summary

In the first half of 2023, China imported a record 11.4 million barrels of crude oil daily, marking a 12% increase from 2022 due to refinery expansions and post-COVID economic recovery efforts. Data from China's General Administration of Customs showed increased imports from 8 out of the top 10 crude oil suppliers compared to 2022. Notably, imports from Russia surged by 23%, Brazil by 49%, and the U.S. more than doubled.

EOA’s Main Takeaway

Our readers were ahead of the curve! We were the first to report this a few days ago: What Does Chinese Oil Data Tell Us about the Oil Market?

Energy Monitor: Fast-Tracking Electricity Access in Sub-Saharan Africa

Summary

Achieving universal electricity access by 2030 is lagging, especially in rural sub-Saharan Africa. Addressing this, SolarAid's "Light a Village" project in Malawi offers an innovative solution where households pay for the electricity they consume, similar to candle expenses, instead of purchasing solar hardware. Launched in 2021, the project has achieved a 99% access rate in pilot areas, with most households previously living without power.

EOA’s Main Takeaway

The problem is always the same: can they scale that up? The answer is no. But it’s always a good way for NGOs and others to ask for additional funding and donations.

The irony here is that small solar and wind projects in the poorest of communities have a larger impact and return on investment than bigger projects in villages and urban areas. But no private investors will do it.

Reuters: Canada’s Trans Mountain Pipe Expansion to Disrupt Oil Flow to US, Boost Prices

Summary

The upcoming Trans Mountain oil pipeline expansion (TMX) in Canada will significantly increase the flow of crude from Alberta to the Pacific Coast. This expansion will redirect oil barrels primarily intended for U.S. Midwest and Gulf Coast refiners and exporters. As a result, U.S. Midwest refineries might see prices increase by up to $2 per barrel.

EOA’s Main Takeaway

Economics dictates that prices of Canadian crude in the US will not increase by more than the toll of TMX and the price differential between certain points in Canada and Asia. However, the story exaggerates the impact because the amount that can be exported through TMX is limited by the pipeline’s “regulated” capacity at a time when Canadian production will continue to increase. In short, while the pipeline will give the Canadian producer optionality, the increase in Canadian oil production limits that optionality.

Reuters: Energy Giants Place Tentative Bets on Wildcat Oil in Uruguay

Summary

Uruguay's state-run energy firm, Ancap, is set to finalize terms for seven offshore exploration licenses next month, attracting interest from major companies like Shell. Despite no previous discoveries in Uruguayan waters, recent finds in Namibia have raised expectations of potential oil or gas off the coast of South America. Santiago Ferro of Ancap highlighted the significant potential of these explorations, suggesting billions of barrels of oil equivalent could be found.

EOA’s Main Takeaway

All of this points out two facts:

1- Additional investment brings additional reserves and production.

2- Nationalism in some countries on the one hand and climate change policies in other countries on the other hand are forcing companies to go offshore. Just another reason why we have been and are still bullish on offshore.

The waters off several Latin American countries are still underexplored and the potential is huge, just look at Guyana!

Business Recorder: WTI Price Surge Shuts Arbitrage Oil Flows from US to Europe, Asia

Summary

The rise in WTI oil prices, influenced by OPEC+ supply cuts and decreased U.S. shale production, is impacting global oil trade. This keeps more U.S. oil domestic, pushing up European and Asian oil prices. U.S. WTI crude futures recently increased over $1 a barrel, affecting Brent prices and indicating a tight supply.

EOA’s Main Takeaway

We have seen this cycle before. As US exports decline, imports increase, inventories build, price differentials will widen, and the current situation will reverse. In fact, Kpler data shows a decrease in exports in recent days.

Bloomberg: Russia’s Crude Shipments Hit Three-Month High as Cuts Tapered

Summary

Moscow has increased its crude oil shipments to the market, even as it commits to extending supply curbs with OPEC+ and Saudi Arabia until year-end. Russia's seaborne flows have reached a three-month peak, with average shipments rising to 3.34 million barrels a day in recent weeks. This surge is primarily seen at the Baltic ports and the Black Sea.

EOA’s Main Takeaway

The saying "Lies, damned lies, and statistics" applies here! Change the dates or look at the long-term horizon and you get a better picture. Figure (3) below shows Russian crude exports. Make your own conclusions! Our expectation is that July, August, and September Exports will be all flat at 4.53 mb/d.

Other News

S&P Global: Equinor signals further capex blowout for flagship Barents Sea crude project

Reuters: Russia considers export duty on oil products of $250/T from Oct. 1 - sources

Bloomberg: Hurricanes Are Veering Away From the US This Month — for Now

Reuters: Shell Opens its Largest EV Charging Station Globally in China