Here's Where I Think Oil Is Headed

The macro-environment is getting tough, but this isn't news to anyone that read the publication last week. I also pointed out signposts we need to be on the lookout for in the oil market in case things turn sideways. Putting all these macro puzzle pieces aside, here's where I think oil is headed.

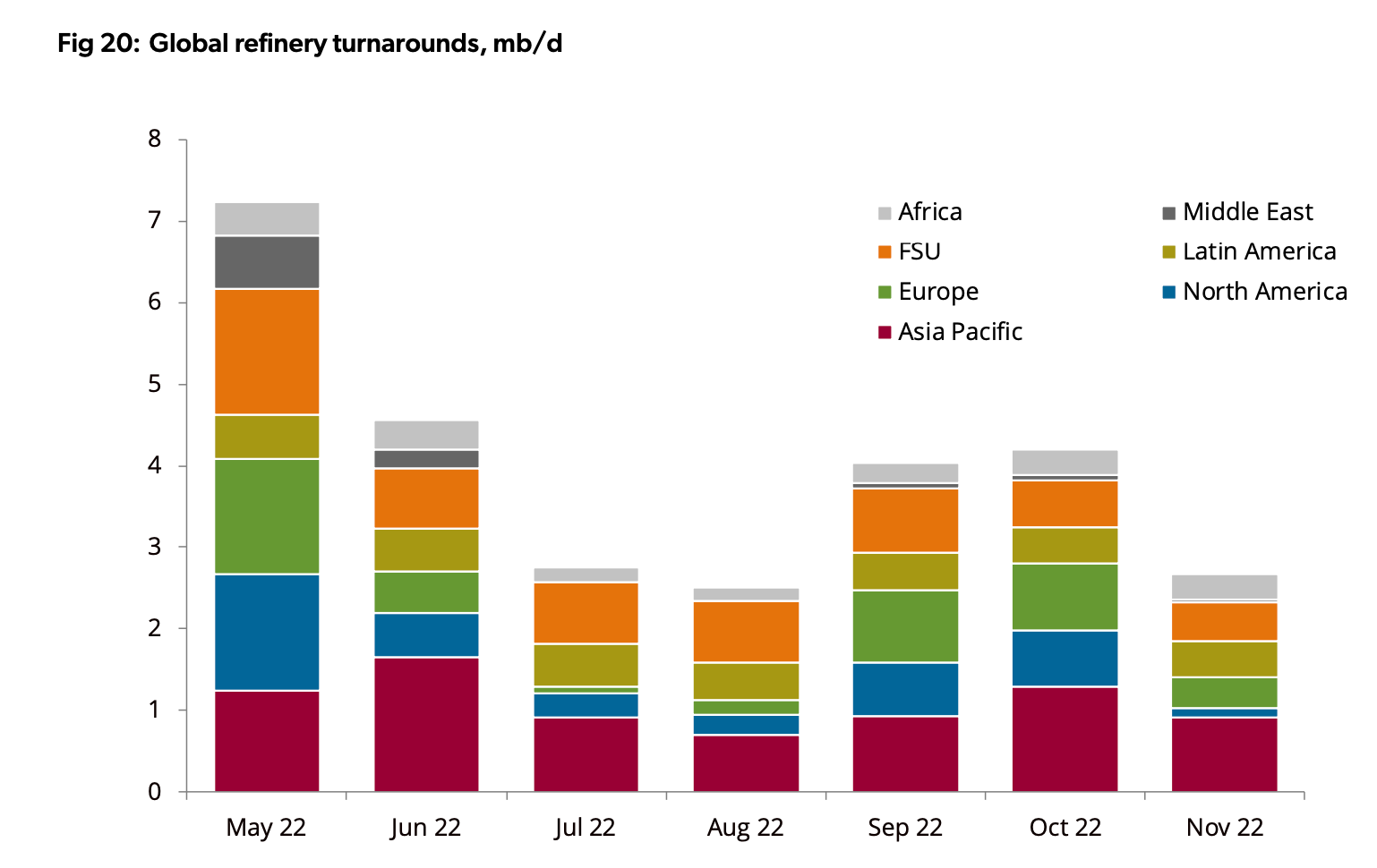

For starters, refinery throughput will be dramatically increasing over the next few months.

Source: Energy Aspects

According to EA, refinery throughput from May to August will increase by ~5 million b/d. Assuming refineries can deliver, then we should see refining margins start to fall.

Source: Barchart.com

Today's price action is also interesting as it appears to confirm the start of higher refinery throughput on the horizon. One thing to keep in mind, however, is that falling refining margins could also be perceived as bearish implied demand, so we need to watch Brent timespreads to confirm that it's just higher throughput and not bad demand.

And if you look at the Brent 1-2 timespread, crude is getting tighter which indicates to me it's just higher refinery demand (higher throughput).

Now this analysis is really important for figuring out where oil is headed. As we wrote last week, consumers are already paying the end price (e.g. crude + refining margins). As a result, if refining margins fall by ~$15/bbl because crude rallied by $15/bbl, the end result is the same.

Using today's 3-2-1 crack spread, we get an implied margin of $53/bbl. Adding that to WTI, the end result is $173/bbl. Refining margins fell by $4/bbl today while crude is flat, so the end result is consumers are paying $4/bbl less. (For those of you thinking in terms of gallons, divide the barrel figure by 42 to arrive at per gallon.)

Looking ahead, my thinking is that refining margins will fall. Demand destruction is real and we are seeing some of that take hold now. With the ~5 million b/d of the expected increase in refinery throughput, I think refining margins fall back to $35/bbl or -$18/bbl from today. The end-user price assuming crude stays flat at $120 is then $155/bbl. This should give crude some room to rally. We could see as high as $135/bbl or $170 end-user price if demand holds up, but that's likely the top of the range.

All things considered, this is a great scenario to have for energy stocks. A price band between $115 to $135 is phenomenal for cash flow generation but for those of you long crude futures, the upside may be a bit limited going forward.

And like all things markets, the oil market will continue to test the different boundaries. For example, if oil demand surprises to the upside, then refining margins could rebound and crude could go up with it. This would then test another ceiling for where demand destruction starts to kick in. Similarly, the opposite would be true as well. If demand surprises to the downside, refining margins would fall, and crude falls along with it. The market will want to see at what price demand starts to rebound.

This is likely the market we are headed towards. We know that oil demand will be sensitive to global economic forces, but the price has always been a key determinant of where demand is headed. As a result, we think oil price will likely stay in a band, refining margins will fall, and crude spreads should move into further backwardation.

Energy stocks remain a buy, so pick your spots well and manage your risk.