(Idea) Athabasca (Revisited)

Note to readers: Dollar references are to Canadian dollars unless otherwise specified.

Please note that we've written up ATH.TO before. Please see our first write-up.

We’ve long favored Athabasca Oil (OTCPK:ATHOF) (ATH:CA) as one of the best E&Ps for gaining exposure to higher oil prices. The shares have outperformed peers in 2023 but continue to trade at a discount to our intrinsic value estimate. The shares are attractive due to ATH’s conservative balance sheet, torque to higher oil prices, exposure to a narrowing WTI-WCF differential, massive asset value, and production growth prospects. We rate ATH shares as a Buy with a price target of $5.50, implying 37.5% upside from their current price of $4.00.

ATH Overview

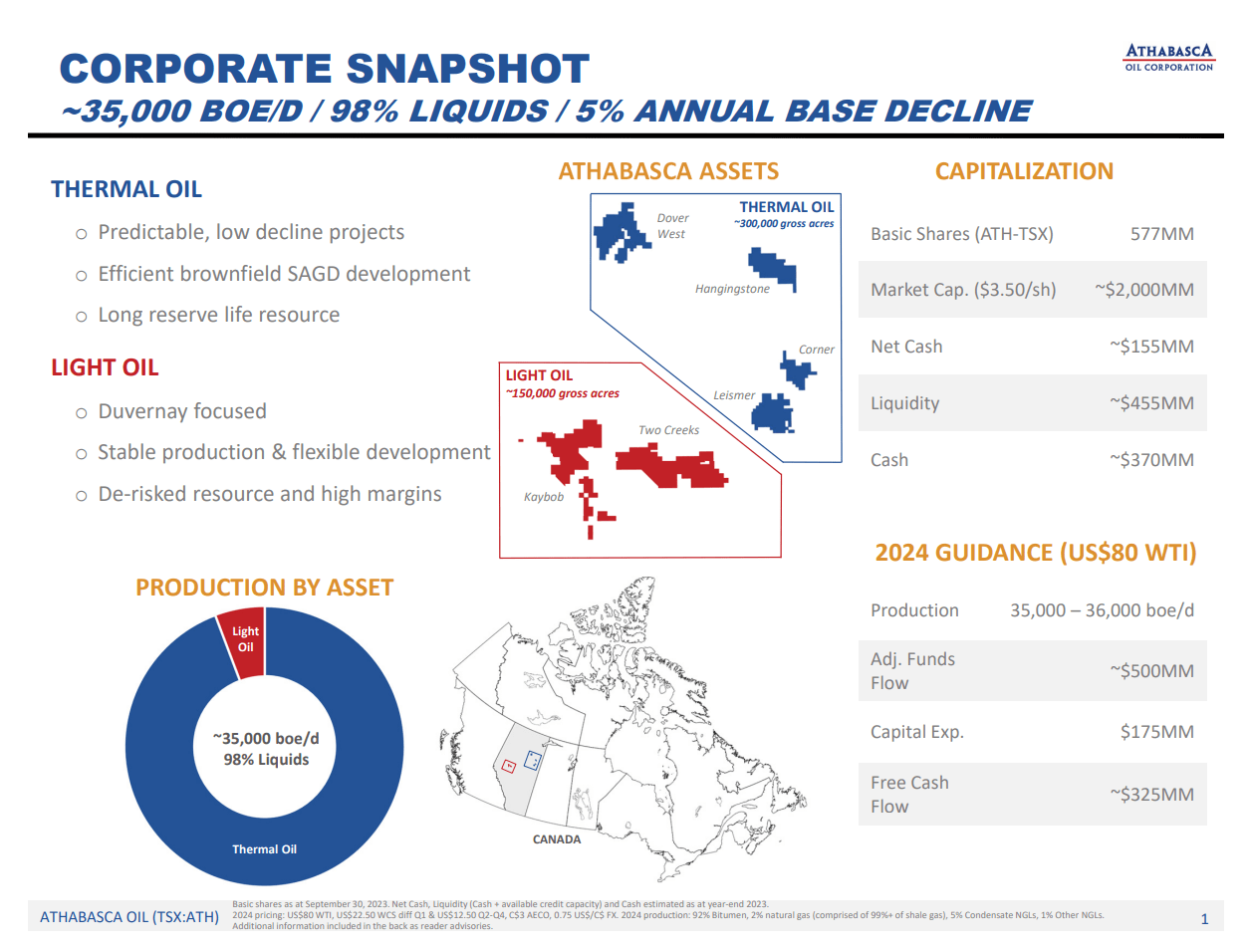

ATH operates heavy oil and light oil properties, as shown below.

Source: ATH December 2023 Investor Presentation.

In the third quarter, ATH produced 36,176 boe/d, which was comprised of 93.1% crude oil, 1.5% NGLs, and 5.5% natural gas.

The largest of ATH’s three main operating assets is its Liesmer thermal oil asset. Leismer produces 24,232 bpd of 100% oil. Proved-plus-probable (2P) reserves stand at 698 million barrels. At the current production rate, its proved reserves will produce for 40 years and its 2P reserves span 85 years. Leismer has a low 5% production decline rate. Most of ATH’s near-term growth plans are focused on this asset.

ATH’s second main asset is its Hangingstone Thermal Oil Project, which produces 7,459 bpd of 100% oil. Proved reserves are estimated to produce at the current rate for 25 years. The asset has 170 million barrels of 2P reserves, which have a life of 60 years at the current production rate. ATH plans to keep Hangingstone’s production flat and use its cash flow to fund other capital allocation priorities.

ATH’s Duvernay light oil acreage is located in the Greater Kaybob area. In the third quarter, it produced 4,458 boe/d. It produced 55% liquids and has 24 million barrels of 2P reserves. The production is primarily liquids-rich natural gas, which serves to benefit ATH’s thermal operations by hedging its condensate diluent costs. The reserves possess unproduced oil, as well. ATH estimates its Duvernay acreage has 500 drilling locations.

The company also sits on a huge undeveloped asset, its Corner thermal project, which is an extension of Leismer. Corner has 2P reserves of 353 million barrels. Like Leismer, it has regulatory approval for expansion to 40,000 bpd. Corner is fully de-risked, but due to its large size, it will require outside capital for development. Development to 20,000 to 25,000 bpd is expected to cost between $750 million and $1 billion. Project sanctioning to first oil production is estimated to take approximately 36 months.

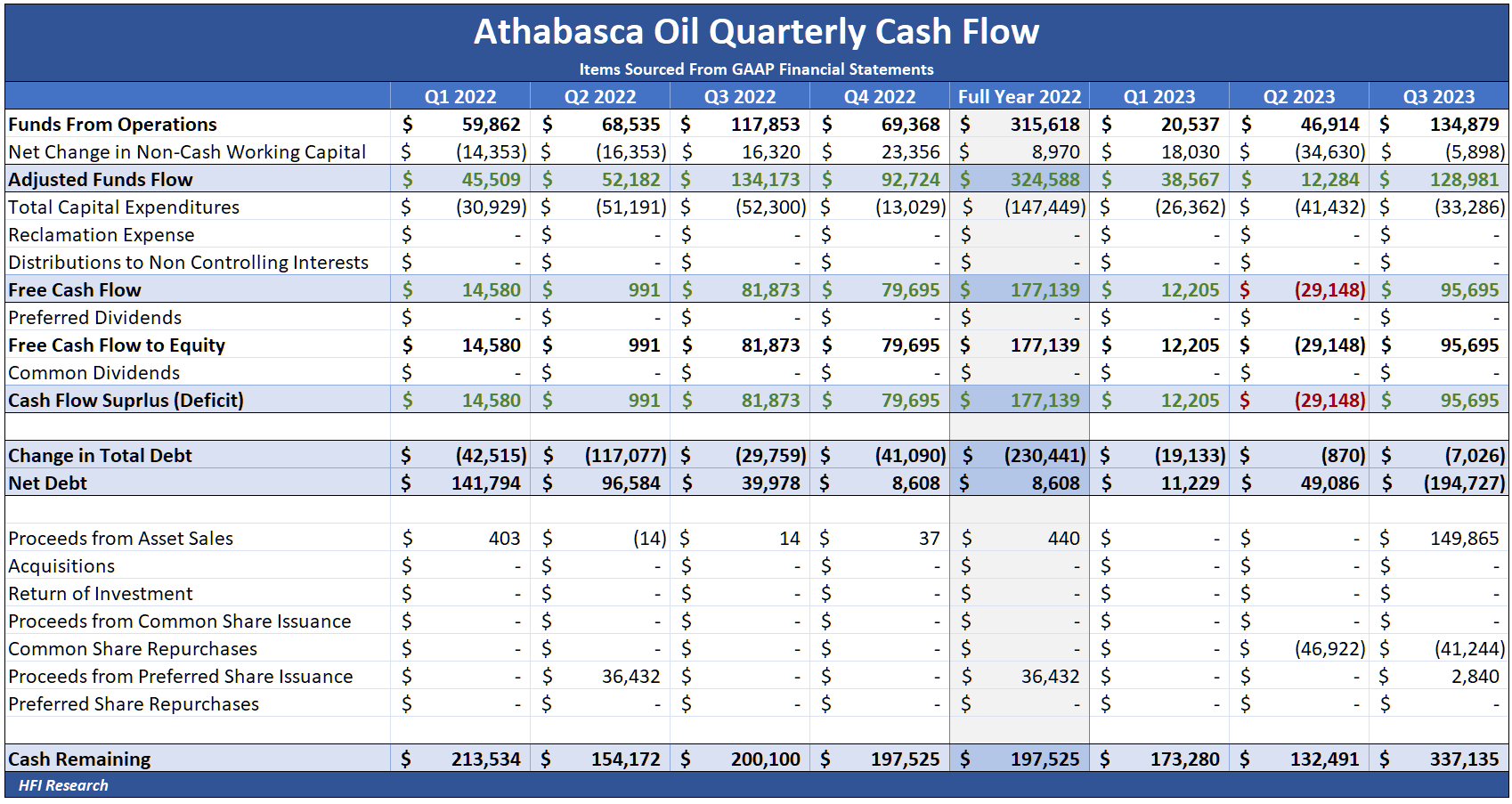

In the third quarter, ATH closed on the sale of its Montney acreage for $165 million to an unnamed private company. Management considered the acreage to be small and uncompetitive with its other assets. The acreage produces approximately 2,500 bpd. ATH realized a $174.6 million loss on the sale. Importantly, the sale put ATH into a net cash position.

For the past few years, the focus of ATH’s capital allocation has been shoring up its balance sheet. After surviving as a heavily indebted operator generating low levels of free cash flow at sub-US$70 per barrel oil prices, it has used the higher prices since 2020 primarily to pay down debt.

This year, with debt falling to low levels, ATH stepped up its share repurchases. As of December 6, it had repurchased 39 million shares year-to-date at an average price of $3.51 per share.

ATH's Conservative Capital Structure

At the end of the third quarter, ATH had $337 million in cash. Long-term debt was comprised of $212.3 million of senior secured second lien notes due 2026. Year-to-date, it has redeemed $24.9 million of the notes, reducing the principal balance 55% below its original $350 million in 2021. The notes bear interest at 9.75% per year, and ATH can redeem them any time before November 1, 2024, at 100% of principal value plus an applicable premium. After November 1, the redemption value increases to 104.875% of par before dropping back down to 100% on November 1, 2025, through maturity one year later.

ATH issued 350,000 warrants in conjunction with its 2026 senior secured second lien notes. Each warrant is exchangeable into 227 ATH shares and has an exercise price of $0.9441 per share that expires on Nov. 1, 2026. Since they can be exercised at any time, the company carries them on its balance sheet as a current liability.

As of Sept. 30, 2023, 75% of the original 350,000 warrants had been exercised. Approximately 20 million remain to be exercised. These warrants and the 22.9 million shares associated with stock-based compensation represent the sources of dilution to public shareholders. The company has offset most of this dilution this year by repurchasing 39 million shares at an average price of $3.51 per share as of December 6.

ATH also has $2.8 billion of tax pools, $2.3 billion of which are fully deductible. These will shield income from taxes for many years.

Capital Budget Supports Growth

Management’s stated objective is to increase cash flow growth on a per-share basis. Given the company’s tremendous reserve size—which spans 80 to 100 years at current production rates—as well as its conservative balance sheet and robust cash flow generation, management considers ATH shares to be significantly undervalued. It therefore believes the best way to increase ash flow per share is to maximize share repurchases. In 2024, it plans to return 100% of free cash flow to shareholders exclusively by way of share repurchases.

ATH will also invest in growing its production. First, it plans to extend Leismer’s production capacity to 28,000 bpd by mid-year 2024. It will then increase Leismer’s production to its regulatory capacity of 40,000 bpd. We expect the project to be completed in 2027 if oil prices and the WTI-WCS differential cooperate. In 2024, Leismer expansion capex will be aimed at expanding treating plants. The project has an attractive capital efficiency of $15,000 bpd.

The company’s second capital investment priority is to increase its Duvernay production. Management expects to accelerate the acreage’s development and production in 2024.

ATH’s production growth over the next few years will be a clear positive for shareholders, given the company’s extensive reserves. It demonstrates that ATH can grow organically on its own without taking on capital-providing partners or additional debt. The growth will bump maintenance capex from $125 million this year to approximately $150 million. It also can also step up its growth by initiating the development of its Corner asset.

Bullish Tailwind from a Positive Differential Outlook

ATH is very sensitive to the WCS-WTI differential, as a widening differential negatively impacts cash flow by increasing diluent expense relative to heavy oil revenues.

The differential outlook is set to improve once the Trans Mountain Expansion (TMX) project is complete. The expanded pipeline will increase egress out of Western Canada by 590,000 bpd.

We expect the WTI-WCS differential to settle in the $12 to $15 per barrel WTI range in the first half of next year. The toll is likely to be stable over the next few years until Western Canadian production reaches takeaway capacity.

TMX has approved preliminary tolls of $11.46 per barrel to shippers that have signed 18-year contracts and that are transporting less than 75,000 bpd. We see differentials holding stable at approximately $12 to $15 per barrel until production increases to capacity over the next few years.

TMX was reportedly 96% complete as of September 30, with less than 16 kilometers of pipe left to install. Mechanical completion was expected in the first quarter of 2024, at which point it plans to begin commercial service.

But for those few who expected the delays to end, TMX faced another setback this week. Its contractor, Canadian government-owned Trans Mountain, threatened the Canadian Energy Regulator (CER) to delay completion by as much as two years and increase costs by billions of dollars if the CER doesn’t reverse its previous decision to reject a requested change in the pipeline’s construction plan. Anything is possible given the scale of incompetence at play in this project, so there’s always a chance TMX’s completion gets pushed back beyond early 2024.