Ferrellgas Partners (OTCPK:FGPR) caught our attention last week as we were preparing our Energy Income Weekly. The MLP’s units jumped 60.4% during the week.

We’ve covered FGPR for years in articles that can be found here, here, and here. The units possess massive upside if the company can meet certain obligations to its Class B units and avoid dilution to its Class A units. The weekly unit performance makes us wonder whether the company might be getting closer to addressing the issue.

The move higher came after FGPR insiders purchased Class A units on the open market. Insiders may sell for various reasons. But they buy for one reason only: to make money.

Source: BamSEC.

Due to these insider purchases—and the high stakes involved for FGPR’s Class A unitholders—we believe the prospects are good that the company will find a way to meet the remaining $207 million obligation necessary to avoid ruinous dilution to the Class A units. If it succeeds, the units offer explosive multi-bagger upside.

However, even if FGPR avoids dilution, it will remain overleveraged. We’re hard-pressed to find an obvious course in which FGPR emerges without an overly risky balance sheet. And as long as it does, the equity will remain at risk of total loss.

At the moment, we don't believe the rewards offered by FGPR equity justify the risks involved, though that could change depending on how events play out.

FGPR’s Class B Unit Obligation

FGPR was put in financial peril after a disastrous acquisition in 2015. The company remained in financial distress until it filed a prepackaged bankruptcy in January 2021.

In bankruptcy, it reshuffled its capital structure to give its equity holders a chance at recouping some of the billions of dollars of market value they lost leading up to the bankruptcy. FGPR replaced $700 million of senior notes—on which it defaulted—with $700 million preferred stock issue and $357 million of Class B equity units.

Over this five-year period, once FGPR pays Class B unitholders $357 million, it has the option to convert the Class B units into Class A units or redeem the Class B units for a redemption price that provides a 15.86% internal rate of return for Class B unitholders over their holding period. If FGPR fails to pay the $357 million to Class B unitholders, Class B units convert to Class A units at a conversion rate that increases annually and becomes progressively more dilutive to the Class A units.

FGPR cannot issue additional Class A units without the consent of the Class B unitholders. It is also restricted from making cash distributions to Class A unitholders.

So far, FGPR has paid Class B noteholders $150 million, bringing its remaining balance to $207 million, which it must pay by April 1, 2026 to prevent significant dilution to the Class A units. At the end of January, FGPR also held $128.4 million of unrestricted cash. The company has maintained a large cash balance in recent years to manage liquidity.

If we assume $100 million of the unrestricted cash can be allocated to the Class B units, the remaining Class B balance would fall to $107 million. In light of the high stakes for the common equity and its largest owner and company founder, James Ferrell, FGPR is heavily incentivized to generate the $107 million to address the Class B units.

Challenges for Reducing Debt

For FGPR, the problem with restructuring is, first, that the company lacks the capacity to take on additional senior obligations, and second, that its debt is so high and free cash flow after preferred distributions is so low that deleveraging after a refinancing will be exceedingly difficult. Common unitholders must be attentive to the long-term risk even if the company succeeds at meeting its Class B obligation.

It’s difficult to gain insight into how management plans to approach FGPR’s balance sheet. Management is extraordinarily opaque in its public comments. It discloses minimal useful information on its quarterly conference calls, only accepting pre-selected questions submitted to its investor relations department.

On the most recent call, held on March 8, management stated the following on its plans for FGPR’s balance sheet.

Source: BamSEC, Ferrellgas Partners, LP Q2 2024 Earnings Conference Call, March 8, 2024.

Management’s comments suggest that it intends to address FGPR’s Class B units through the company’s improved credit profile and favorable credit market conditions. Management noted that the yield on the market price of FGPR’s senior notes declined to the 6%-to-7% range, not significantly above the rate paid on the senior secured notes that it issued when prevailing interest rates were lower.

The low yields imply that the credit market considers the option represented by FGPR’s common equity to have value. At the current $11.83 price of the Class A units, they have a market cap of $379 million.

Cash Flow Consumed by Interest and Preferred Distributions

FGPR doesn’t have much room to add debt without putting the company in greater financial peril. Net long-term debt plus preferred obligations remain high.

The last time the balance of obligations senior to the equity stood this high was after the company’s disastrous acquisitions in 2015.

Meanwhile, interest expense and preferred distributions consume all operating income.

Cash flow figures tell a similar story. After interest and preferred distributions, FGPR is essentially cash flow neutral. In a good year, it can generate a cash flow surplus after preferred distributions in the $20 to $40 million range, assuming annual capex of $100 million. A refinancing, which is likely to add higher-cost debt, is likely to significantly eat into this slim cash flow cushion.

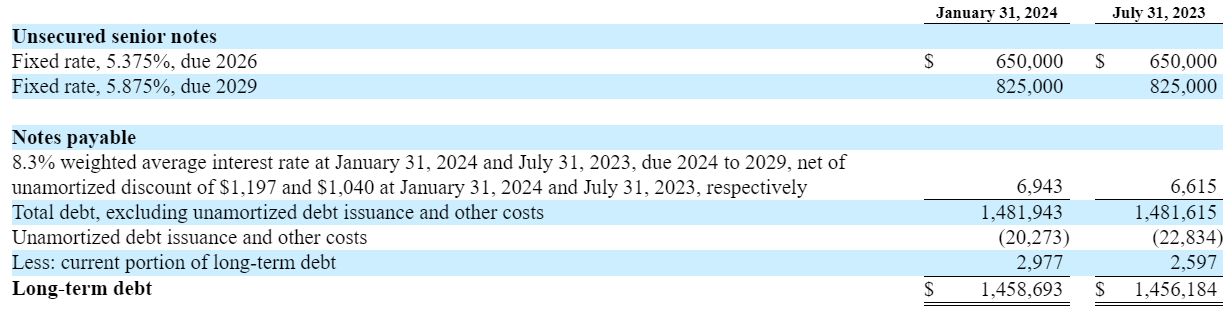

For instance, FGPR has $650 million maturing in 2026, which it will want to address by 2025 at the latest.

If the debt is refinanced at an interest rate of 8%, it would add $17 million to interest expense annually.

Then there is the issue of FGPR’s high-cost preferred units. Its $700 million of preferreds currently pay a distribution rate of 8.956%. Any viable balance sheet restructuring would have to address the $63.4 million in distributions associated with these units. FGPR can redeem the preferreds before 2031, but the redemption price on the units locks in an internal rate of return so high as to make redemption unlikely, given FGPR’s strained balance sheet. The company has the option to pay preferred distributions in-kind for an unspecified number of quarters, but doing so would increase the Class B redemption amount, so it would frustrate efforts to address the Class B unit obligation.

From an EV/EBITDA perspective, FGPR is approaching the maximum enterprise value acceptable to investors. The company generates Adjusted EBITDA of around $300 million. An appropriate EV/EBITDA ratio of around 8-times would allow for an enterprise value of $2.4 billion, which is roughly in line with FGPR’s current enterprise value.

Debt-to-EBITDA among peers runs at slightly less than 5.0-times. If we include FGPR’s preferred units with debt, its debt-to-EBITDA is significantly higher, at 7.3-times.

What FGPR Has Going for It

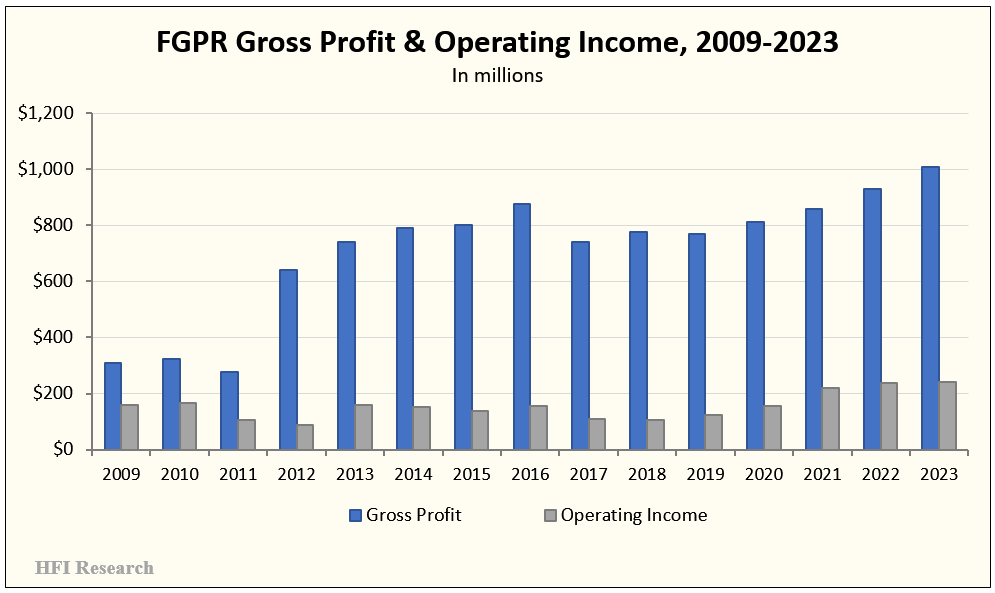

FGPR’s business is fundamentally healthy. In fact, results have improved over the past few years relative to the company’s history. Gross profit and operating income have been on an uptrend since 2019 after the adverse impacts of the disastrous acquisitions were worked through.