(Idea) Mach Natural Resources - A Transformational 2025 Will Drive Income Growth And Appreciation In 2026 And Beyond

By: Jon Costello

Please see our previous public write-up on MNR 1.10%↑.

(Public) Mach Natural Resources Enters The Buy Zone

·

November 12, 2025

Please read our previous article on MNR for context.

Mach Natural Resources LP (MNR) exited 2025 as a fundamentally different company than it was when it entered the year. The company’s growth, its improved prospects amid higher oil prices, and its enhanced exposure to natural gas—all while its units sold at an undeserved discount—led me to buy the units in January of this year at an average cost of $10.83 per unit. I detailed my reasoning here.

Mach’s fourth-quarter results showcase the company’s improving prospects, which support our long-term investment thesis.

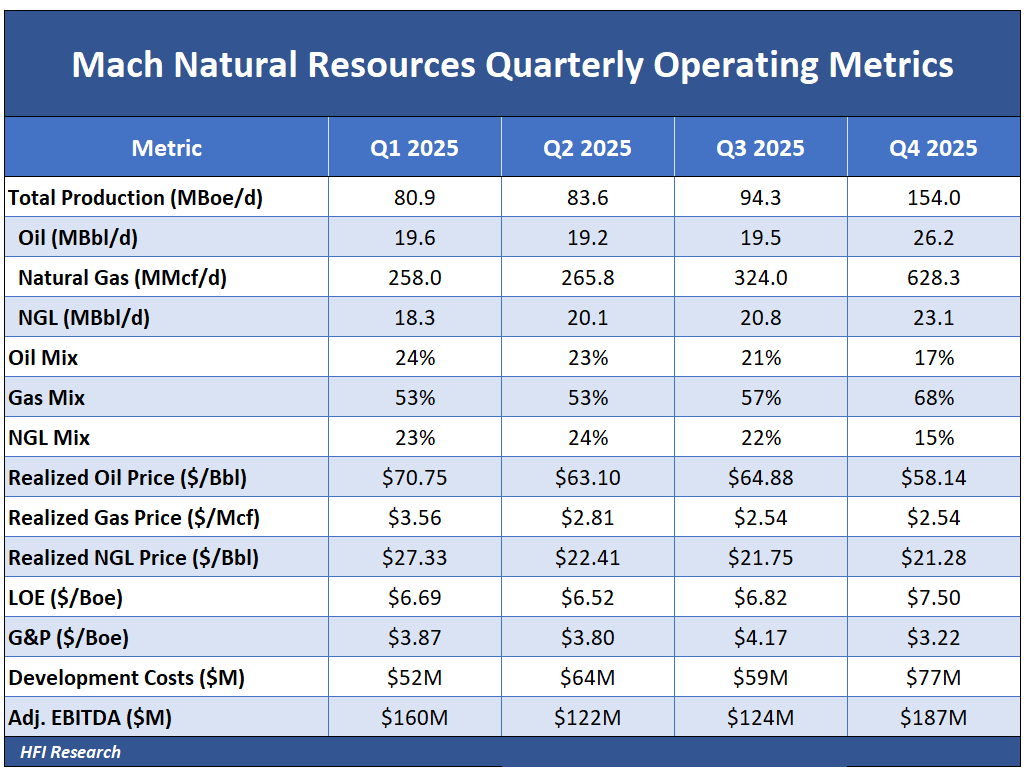

Fourth Quarter Results: The First Post-Acquisition Quarter

Mach’s IKAV and Sabinal acquisitions, which closed on September 16, transformed the company from an 84 Mboe/d Anadarko Basin operator into a 154 Mboe/d multi-basin E&P with significant natural gas exposure across the San Juan Basin. The fourth quarter was Mach’s first full quarter of consolidated operations following the September acquisitions.

During the quarter, production averaged approximately 154 Mboe/d, up from roughly 84 Mboe/d in Q2 2025 prior to the deals’ closing. Mach’s product mix shifted meaningfully toward natural gas, which now dominates the production profile, a direct result of the San Juan Basin assets acquired from IKAV.

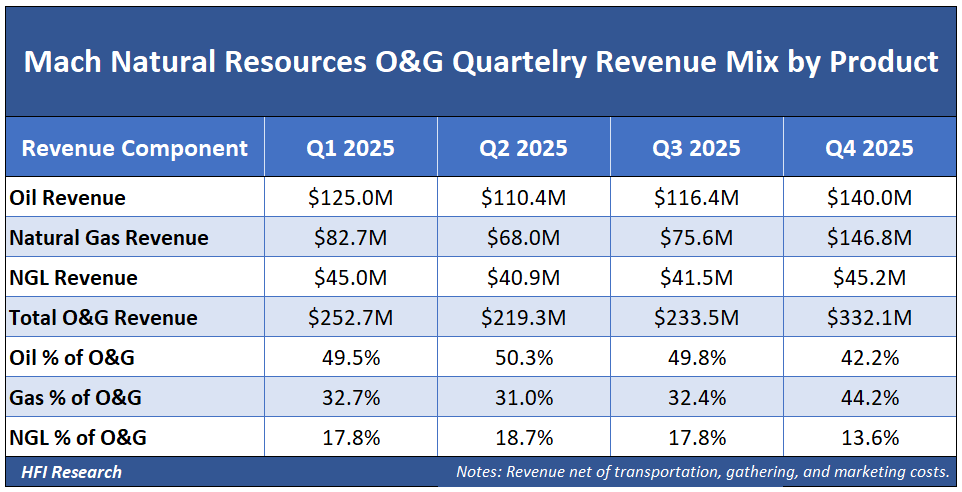

The pivot toward natural gas was evident in Mach’s quarterly financial performance. Nevertheless, the company still generated 42% of its revenue from crude oil sales.

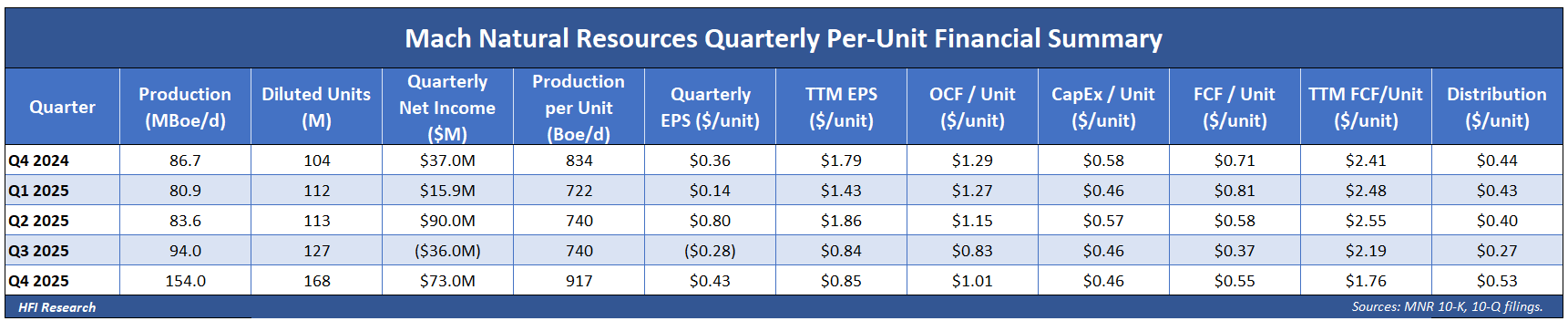

The fourth-quarter distribution of $0.53 per unit reflects the post-acquisition unit count of 168.2 million and the low average commodity prices prevailing during the fourth quarter.

The company refrained from debt reduction during the fourth quarter but will likely pay down significant debt with the increased cash flow generated at current commodity prices.

Full-Year 2025: Setting the Stage for Distribution Growth

For the full year 2026, Mach produced 21.1 Mboe/d of oil, 369.9 MMcf/d of natural gas, and 20.5 Mboe/d of NGLs at average realized prices of $63.72/bbl, $2.76/Mcf, and $23.00/bbl, respectively. Fourth-quarter production results are in line with management’s full-year 2026 guidance, so they provide a good baseline for estimating future performance.

Revenue hit $1.18 billion with operating cash flow of $507.0 million, capex of $262.2 million, and free cash flow before acquisitions of $244.8 million.

Revenue included $81.3 million in realized derivative gains, attributable to oil prices declining throughout the year against Mach’s hedge book. Operating cash flow reached $507.0 million, while capital expenditures for oil and gas development totaled $262.2 million. Free cash flow before acquisitions came to $244.8 million. In the third quarter, Mach recorded a $90.4 million non-cash ceiling-test impairment, driven by a 12-month trailing price decline following the acquisitions. Net income for the year was $143 million, or $1.09 per diluted unit on a weighted average of 131.5 million units.

Fourth quarter’s $0.53/unit was declared on February 12, 2026, payable against 168.2 million units outstanding, 77% more units than a year earlier. The per-unit figure reflects the impact of Mach’s February 2025 public offering, in which 14.8 million new units were offered at $15.50, and its 49.6 million units issued as consideration for IKAV and Sabinal. Despite the unit issuance, per-unit results remained positive amid volatility in commodity prices throughout the year.

Total cash distributions for 2025 were $244.5 million, nearly equal to free cash flow. The high payout percentage demonstrates management’s consistent execution of Mach’s income-focused model. The variable distribution model works as designed. The amount of cash distributed to unitholders fluctuates in proportion to commodity prices and the company’s capital program.