(Idea) Peyto Exploration

Note: Dollar references are to Canadian dollars, except where otherwise specified.

Peyto Exploration (PEY:CA) is the fifth-largest natural-gas-focused E&P in Canada, producing 128,000 boe/d. Peyto’s main attraction is that it’s one of the lowest-cost operators with one of the highest returns on capital among North American E&Ps.

The company produces natural gas and NGLs in the Alberta Deep Basin, where it has focused its operations since its inception in 1998.

Source: Peyto Exploration website.

The Deep Basin’s geology is characterized by a lack of mobile water in its sandstone formations, which reduces risk in recovering hydrocarbons and increases recovery rates. Hydrocarbons are stacked underground in formations that resemble a layer cake. Since Peyto can use the same surface infrastructure to develop multiple layers, the geology results in cost-efficient production.

Petyo’s Competitive Advantage

Peyto’s competitive advantage lies in its low cash costs. This advantage stems from the favorable geology underlying the company’s acreage, management’s knowledge of its operating areas, and the company’s ownership, operation, and control of its infrastructure—much of which it built from the ground up.

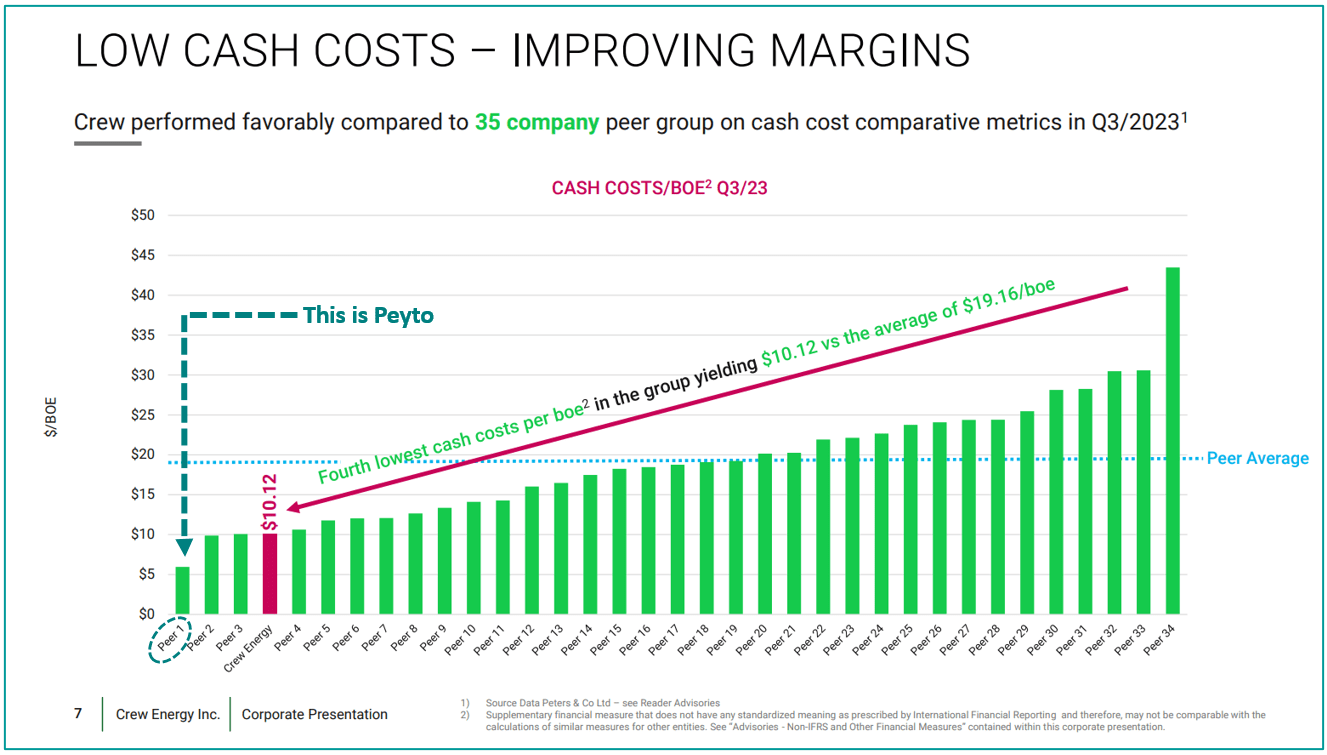

Peyto’s cash costs are some of the lowest among intermediate Canadian E&Ps, as shown in the following graphic taken from a recent Crew Energy (CR:CA) investor presentation. The data is sourced from Peters & Co., an investment bank specializing in the Canadian energy industry.

Source: Crew Energy January 2024 Investor Presentation. Blue-green dotted lines and text added by author.

The company’s cash costs stand at less than half its peer-group average shown in the chart, which is just shy of $20 per barrel of oil equivalent (boe). The low costs reduce the risk of value destruction to shareholders stemming from sustained low natural gas prices.

In previous articles, we’ve mitigated this risk by favoring natural-gas-weighted E&Ps with heavier liquids weighting, but which still operate with low cash costs. Spartan Delta (SPE:CA) is a good example—we continue to view SPE as a top contender for natural gas exposure. But for investors who prefer to avoid liquids-weighted E&Ps and seek a natural gas E&P with low risk, Peyto is our top choice.

The company has sustained its cost advantage since its founding, and given the consistent operating culture and philosophy embraced by successive leadership teams, we don’t expect that to change.

Hedges and Marketing Agreements Stabilize Revenues

While keeping its costs low, Peyto also takes measures to support its top line. For one, it hedges a substantial portion of its production. In addition, it diversifies its revenue through supply agreements with customers far afield from its operating areas.

The company’s competitive advantages drive its successful hedging program. Its sustainably low costs allow it to lock in wide profit margins at natural gas prices that generate only marginal profitability for many of its higher-cost peers. To capitalize on this advantage, Peyto maintains a longstanding programmatic hedging policy.

On the marketing side, Peyto’s gas is distributed through major Canadian export pipelines into the U.S. Its extended reach allows it to hedge its gas in various markets, reducing risk and minimizing exposure to volatile AECO. Its marketing strategy allows it to forward sell and hedge blocks of production in a diversified manner to further minimize risk. One example of the company’s unique strategy is its recent agreement to supply approximately 8,700 boe/d of natural gas to Kineticor’s 900MW Cascade Power Plant. The deal not only diversifies Peyto's revenues, but the company will realize a substantial premium over AECO, as its gas will be priced based on Alberta power prices. Moreover, Peyto’s Swanson natural gas processing plant is connected to the power plant through a newly constructed 23 km pipeline.

Full-Cycle FCF Generation

Peyto’s unique combination of diversified revenues, hedged production, and low cash costs allow it to achieve some of the consistently highest returns on capital in the energy sector. Its return on capital employed hovers around 15%, while its return on equity is regularly in excess of 20%. By contrast, the average return on capital employed for E&Ps over a full cycle is typically in the 8% to 10% range, with return on equity averaging a few percentage points higher.

Robust cash flow generation and high returns have enabled Pety to grow its value per share at high rates for decades. The following graphic illustrates the company’s superior long-term value creation.

Source: Peyto Exploration January 2024 Investor Presentation.

Peyto’s hedged, diversified revenue and low-cost structure also allow it to generate a consistently positive netback, a proxy for gross profit per barrel. In fact, Peyto has remained profitable in every natural gas pricing environment.

The following chart illustrates the company’s consistent profitability through different macro conditions, which include some of the best in 2022 and some of the worst in 2020. It contrasts quarterly U.S. natural gas prices—to which Canadian AECO prices are closely tied—and Peyto’s cash netback, or gross profit per barrel. Quarterly natural gas prices are pictured in the table at the top, and Peyto’s quarterly netback is pictured in the lower table.

Source: Peyto Exploration Q3 2023 Results Press Release, Sept. 6, 2023.

Other intermediate E&Ps haven’t fared nearly as well, whether weighted toward gas or liquids. Most lack Peyto’s advantages. Also, since their revenues tend to be more liquids weighted, their lifting costs are structurally higher.

Peyto’s robust cash flows can be allocated at management’s discretion. Recent quarterly capital allocation is shown below. Management favors debt reduction and dividends over share repurchases.

Consistent cash flow generation also allows Peyto to reliably cover its dividend down to levels we estimate at less than $2.00 per mcf, where natural gas trades today. As Peyto’s peers run up debt to cover their dividends or are forced to slash their dividends outright, its shareholders can rest assured that their payout will be forthcoming in every phase of the market cycle.

Peyto’s cash flow has allowed it to pay a dividend consistently since 2003, as shown below.

This is a rare feat among E&Ps. The dividend has been paid monthly, with the exception of the 2020-2021 period, when it shifted the payout to quarterly.

The Repsol Acquisition

In November 2023, Peyto closed on its acquisition of acreage previously owned by Repsol (OTCQX:REPYY). The acquisition was a home run for Peyto. It boosted production capacity at a reasonable cost, brought a significant increase in reserves, and created significant production growth opportunities. All these features will accrue to the long-term benefit of Peyto shareholders.

In the deal, Peyto paid $468 million for a 65% working interest in 455,000 net acres of land. It funded the deal by issuing 16.9 million new shares at $11.90 for proceeds of $201 million while funding the remainder through long-term debt.

The acquired acreage fits hand-in-glove with Peyto’s existing Greater Sundance Area acreage, which it has developed for 25 years. The map below shows the fit:

Source: Peyto Exploration January 2024 Investor Presentation.

At the time of acquisition, the acreage produced 23,000 boe/d, which translates to a reasonable acquisition price of $20,348 per flowing barrel of oil equivalent, or $3,391 per flowing mcf of natural gas. It increased Peyto’s production by 25%, and its proved, developed, producing (PDP) reserves by 24% on a boe basis.

The deal included valuable infrastructure, namely, Repsol’s gathering system, five operated gas processing plants, and 2,200 km of existing pipeline infrastructure. Much of the acquired infrastructure was underutilized. Due to the contiguous nature of the acquisition, it can also be serviced through Peyto’s legacy infrastructure.

The acquired assets feature a low production decline rate of 12%. As a result, the wells are approximately 30% more productive than Peyto’s legacy wells. The additional new production will reduce Peyto’s corporate decline rate from 29% to 25%, which, in turn, will reduce the amount of capital necessary for the company to sustain and grow production.

Due in large part to their low decline rate, the acquired assets possess a very low and attractive capital efficiency of $9,500. Adding them to Peyto will bring Peyto’s capital efficiency on its future production from $12,500 before the deal to $10,500, an impressive 16% improvement.

Peyto plans to grow production on the assets from 23,000 boe/d at the time of the acquisition to an annual average of 33,000 in 2024. By 2026, management expects the assets to drive Peyto’s production growth from slightly more than 100,000 boe/d in 2023 to 160,000 boe/d by the end of 2026.

The one negative feature of the asset is that they have higher cash costs than Peyto. However, as production increases on existing infrastructure, unit costs will decrease. We also expect Peyto’s management to reduce cash costs associated with drilling and infrastructure over the coming years.