(Idea) Tamarack Valley

Note: Dollar references are to Canadian dollars unless otherwise specified.

Tamarack Valley Energy (TVE:CA) shares are the second-worst performer year-to-date among Canadian mid-cap and large-cap E&Ps. Only natural gas-weighted Birchcliff Energy (BIR:CA) shares have fared worse. Investor sentiment toward TVE has suffered as management under CEO Brian Schmidt repeatedly assured investors that increased capital returns were imminent, only to make a large acquisition that added debt and pushed back the capital return time horizon.

While management has failed to properly set investor expectations and has a penchant for acquisitions, it has outperformed from an operational perspective. The company holds some of the most economic acreage in North America. TVE's asset quality is evident in its drilling results. Since acquiring its Clearwater acreage, it has drilled some of the best wells in Canada.

Investor sentiment has pushed its shares far below our estimate of intrinsic value. While management hasn’t sworn off acquisitions, we don’t expect another major deal, at least until debt is paid down to less than $500 million. Meanwhile, operations should continue to perform well, and cash flow surges as WTI trades above US$80 per barrel.

We rate TVE shares as a Buy with a $5.00 price target. The shares offer 58.7% upside to our price target from their current price of $3.15.

Introduction

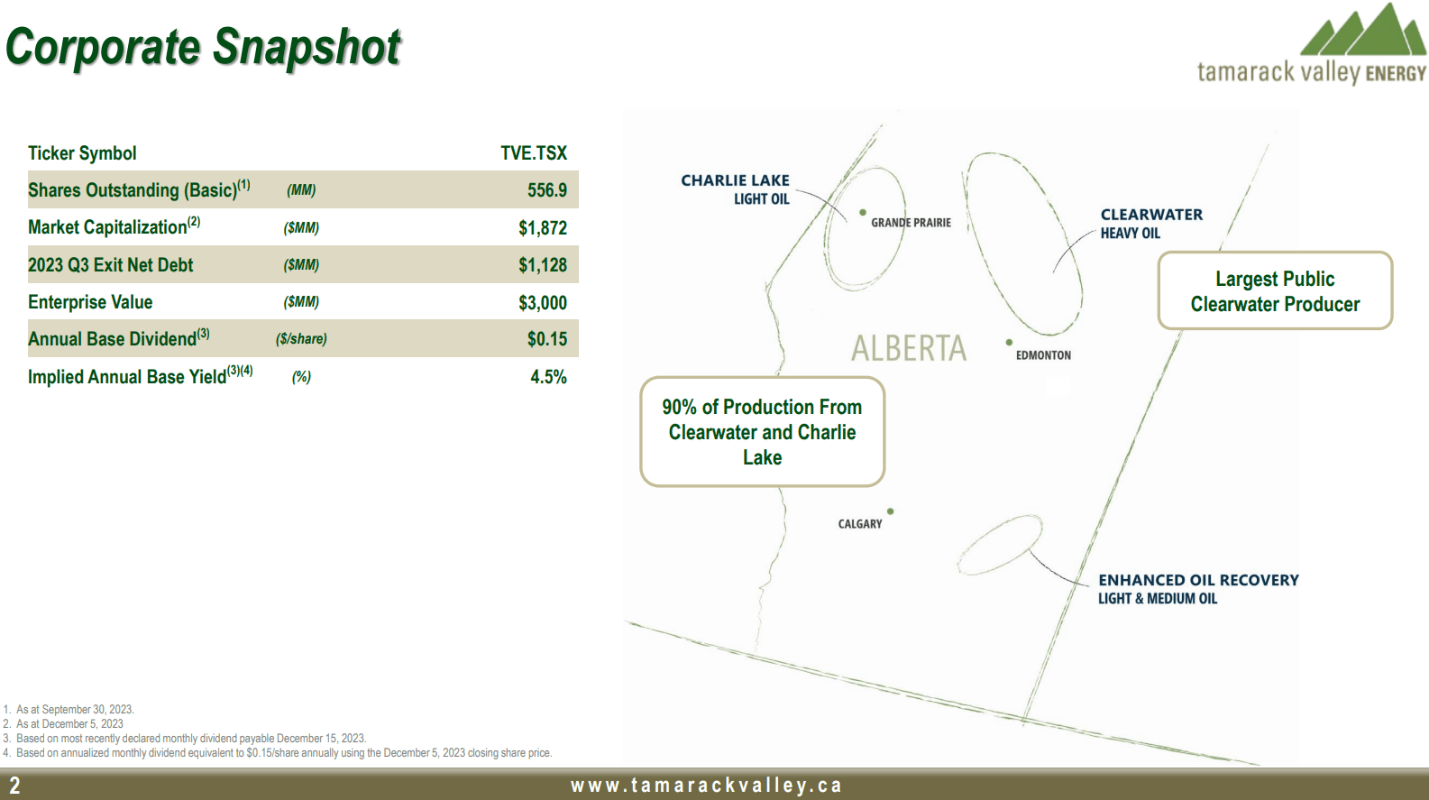

TVE operates in three regions in Alberta. It holds high-quality core acreage positions in the Clearwater heavy oil play, where it produces approximately 35,700 boe/d, as well as in the Charlie Lake light oil play, where it produces 16,200 boe/d. It also has a portfolio of enhanced oil recovery opportunities in southeast Alberta that produce approximately 14,800 boe/d.

Source: TVE December 2023 Investor Presentation.

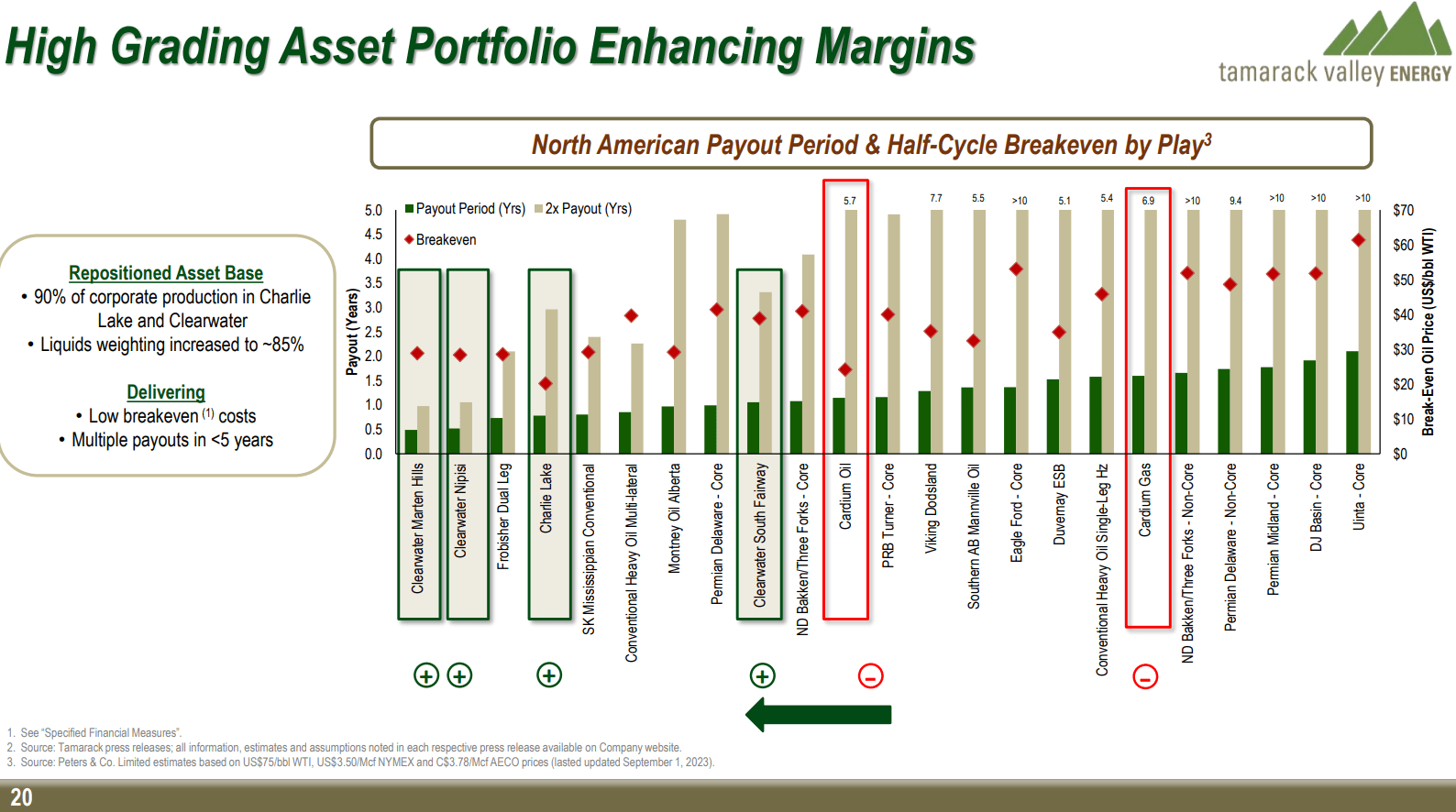

TVE has spent the last few years high-grading its portfolio by increasing its presence first to Charlie Lake and, more recently, the Clearwater. It has also disposed of lower-quality, non-core assets. Management touts TVE’s asset quality, as well as its move away from the lower-quality Cardium play, in the slide below.

Source: TVE December 2023 Investor Presentation.

After several acquisitions in 2022, TVE has emerged as the largest producer in the Clearwater. In February 2022, it acquired Crestwynd Exploration, a privately owned Clearwater producer, for $184.7 million, paying $92.6 million in cash and 26.3 million TVE shares at $3.50. Crestwynd produced approximately 4,500 boe/d of 100% liquids. Then in June 2022, TVE acquired privately-owned Rolling Hills Energy for $93 million and other assets in the Peavine area of the Clearwater. Rolling Hills produced approximately 2,100 boe/d.

TVE’s biggest leap into the Clearwater came in October 2022, when it acquired privately owned Deltastream Energy for $1.425 billion. At the time, Deltastream was producing approximately 20,000 boe/d of 93% liquids. Its production accounted for 21.5% of the Clearwater’s 93,000 boe/d of total production. TVE financed the deal with $825 million of cash, $300 million in a deferred acquisition payment note, and $300 million of TVE shares at $3.75.

TVE Shares Remain in the Doghouse

TVE shares have been penalized ever since the Deltastream deal. The shares failed to get as much traction as peers as oil prices rose in mid-2023. When prices collapsed later in the year, they sold off even more.

While the long-term impact of TVE's Clearwater acquisitions is open to debate, the fact of the matter was that in 2022, the company had to do something to address its shrinking reserve life. TVE’s 2021 reserve report estimated its remaining proved and probable reserve life at 8.8 years—too short for shareholder comfort. The Clearwater deals in 2022 lengthened its reserve life to 11.3 years and gave TVE sufficient scale to improve its results. They also allowed the company to replace 118% of its produced reserves in 2022 through the drill bit.

The clear negative was that TVE chose to pay up for quality. Moreover, it did so in mid-2022, when WTI was trading above US$90 per barrel. TVE paid $66,261 per flowing barrel for Deltastream, one of the highest-priced acquisitions that year.

Admittedly, “per flowing barrel” is a flawed, back-of-the-envelope metric, but it can be useful in gauging what an acquirer gets relative to the consideration they give. Comparing the Deltastream deal with other recent deals illustrates its high price. For starters, TVE's Rolling Hills acquisition earlier in 2022 was made at a far more reasonable $44,285 per flowing barrel. Recent peer acquisition metrics were also much lower, as shown in the table below.

Clearwater core acreage could fetch a higher price due to its nearly 100% liquids weighting, lower decline rate, breakeven costs than the Montney and Duvernay plays, and enhanced oil recovery opportunities. But there are negatives that offset these positives. For one, the play produces heavy oil that trades at a discount from lighter grades. Heavier grades are exposed to the volatility inherent in the WTI-WCS differential.

Adding insult to injury for TVE shareholders in the wake of the Deltastream deal, management proceeded to overpromise and underdeliver on the deal’s anticipated financial benefits. Its guidance of accelerated debt paydown shortly after the deal closed never materialized. The same can be said for its guidance of increased shareholder returns. While a large part of management’s underperformance was lower-than-expected prevailing commodity prices, it should have known better than to have promised so much on the basis of US$85 per barrel WTI.

Further complicating matters was that Deltastream’s largest shareholder, Arc Financial, became TVE’s largest shareholder after the deal, holding approximately 11.7% of TVE shares. Over the next few quarters, Arc dumped TVE shares onto the market, putting downward pressure on TVE’s share price and likely playing a role in the shares’ inability to rally despite surging oil prices.