Note: On June 1, all "new" new idea write-ups will be published on Ideas from HFI Research. However, because Veren is a core holding in the HFI Portfolio, subscribers will receive full write-ups along with updates on this name.

Veren (VRN:CA)—the former Crescent Point Energy—produces approximately 195,000 boe/d comprised of 59.1% oil and condensate, 9.7% NGLs, and 34.2% natural gas.

The company possesses everything we look for in an E&P holding: outstanding management, consistently strong operations, superb capital allocation, and cash flow torque to commodity prices. We see significant upside potential in Veren shares over the coming years.

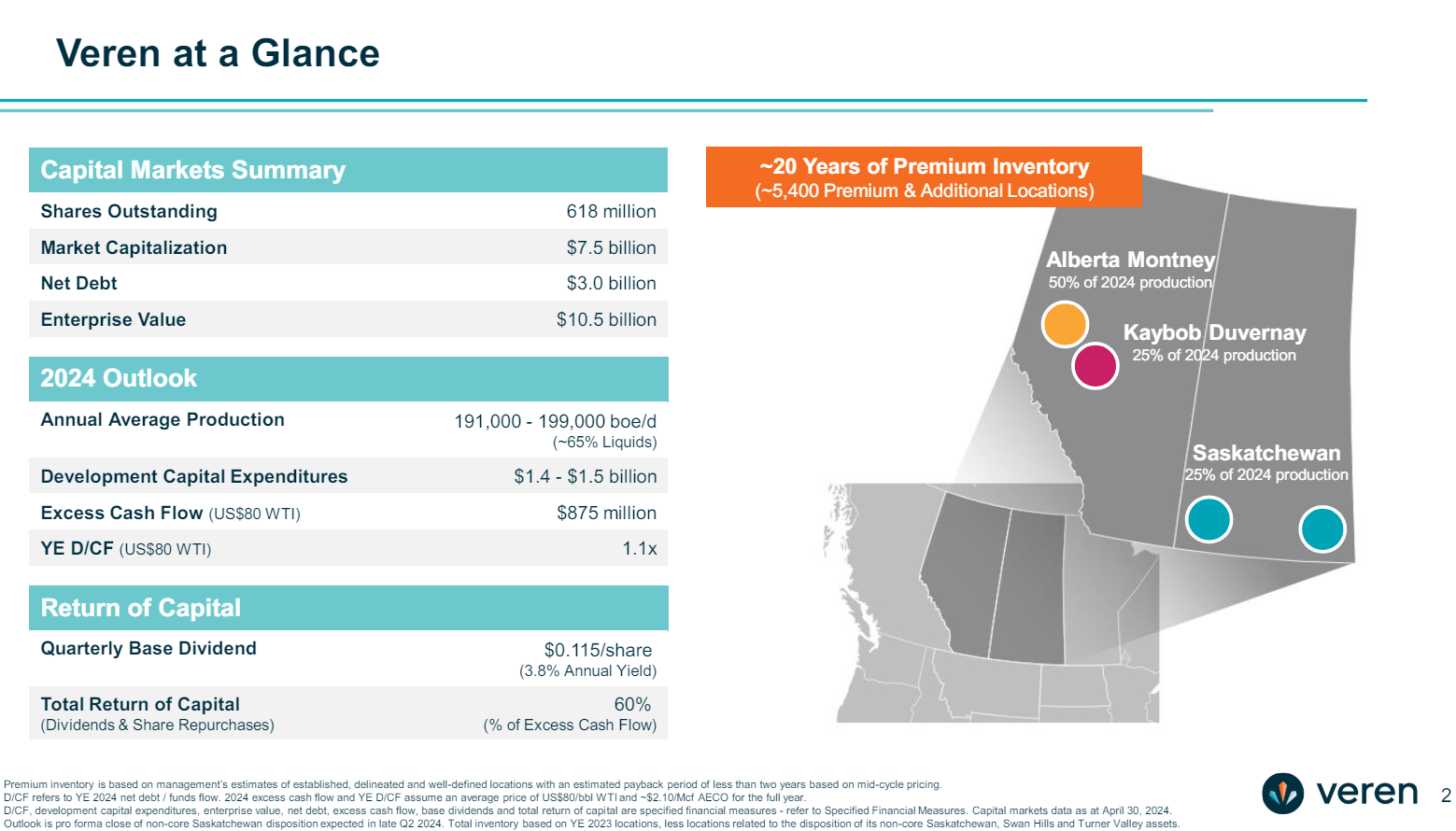

A snapshot of the company is shown below.

Source: Veren Investor Presentation, May 2024.

Veren’s most notable feature is its remarkable success over recent years in amassing dominant acreage positions in the Alberta Montney and Kaybob Duvernay. This process involved a continuous reshuffling of assets through divestitures and acquisitions, illustrated in the following graphic.

Source: Veren Investor Presentation, May 2024.

Veren has now emerged as one of the largest leaseholders in the Montney. The asset has provided it with some of the most economic drilling prospects in the play, a vast inventory of drilling locations, and the opportunity to improve drilling results further. In recent years, management has dramatically improved Veren’s capital efficiency while reducing its breakeven cost and improving long-term growth prospects.

Veren's transition has involved several major deals, beginning with its $900 million Kaybob Duvernay asset purchase from Shell (SHEL) in 2021. In January 2023, Veren enhanced its Duvernay position with a $370 million acquisition from Paramount Resources (POU:CA).

The company grew its Montney position in 2023 through its $1.7 billion acquisition of Montney assets from Spartan Delta (SDE:CA). The acquired assets produced 38,000 boe/d from acreage that was contiguous with Veren’s existing assets. They extended the longevity of Veren’s Montney drilling inventory to more than 20 years.

Later that year, Veren’s disposed of its North Dakota assets for $675 million. The assets had been producing 23,500 boe/d comprised of 89% liquids. The assets possessed a limited drilling inventory and were expected to decline over the coming years. The deal allowed Veren to pay down debt taken on to fund the Spartan Delta acquisition.

In November 2023, Veren further consolidated its position in the Montney by acquiring publicly-held Hammerhead Energy for $2.55 billion. The acquisition significantly increased the company’s total production, though Hammerhead’s approximately 50% natural gas weighting reduced Veren’s liquids production weighting. Concurrent with the deal, Veren issued 48.55 million of stock at $10.30 per share for proceeds of $500 million of common shares in a bought deal financing.

Then, in the first quarter of 2024, Veren executed smaller asset sales of Southern Alberta, Swan Hills, and Turner Valley acreage for a combined $118.6 million.

Veren announced its most recent major deal on May 10, when it sold certain oil-weighted Saskatchewan assets to Saturn Oil & Gas (SOIL:CA) for $600 million. The deal will accelerate debt paydown and eliminate asset retirement obligations.

Veren’s Five-Year Plan

In the near-term Veren has shown strong well results while outperforming financially. The company has drilled some of the best wells in its plays, as noted by management and confirmed by multiple third-party specialist sources.

Veren reported strong first-quarter results, which it reported on May 10. Cash flow per share of $0.91 beat consensus expectations of $0.86 by 5.8% due to higher production, which came in at 198,551 boe/d versus expectations of 192,000 boe/d. Greater than expected liquids production growth drove the total production beat.

Longer term, we expect Veren to continue to execute by increasing production, enhancing capital efficiency, and growing free cash flow per share at a relatively high rate relative to peers and its own history. We were pleased to hear Veren's CEO, Craig Bryksa, clearly state that the company is taking a “good long pause” from deal activity. Management and the board of directors are satisfied with Veren's current asset portfolio and its ability to generate the growth called for in its recently announced five-year plan.

While five-year plans for E&Ps are notorious for going off the rails, Veren’s management is of sufficiently high integrity to put some serious weight behind its intentions. We consider Veren's five-year plan a reliable guide to what it is capable of achieving over the coming years.

Through year-end 2028, Veren expects to grow its production from approximately 195,000 boe/d to 260,000 boe/d. The lion’s share of production growth will be sourced from the Montney and Duvernay, both of which are expected to increase production by 40% over the period. Moreover, the contiguity of Veren’s acreage should allow it to realize economies of scale that allow it to increase operating cash flow while keeping costs low, thereby boosting the growth in free cash flow per share over time.

Source: Veren Investor Presentation, May 2024.

Management intends to grow free cash flow at a 7% compounded annual rate. Inclusive of the impact of share repurchases, the growth rate is expected to increase to 15%.