Editor's Note: Starting on July 1, all idea write-ups will be published on Ideas from HFI Research. Vermillion Energy is part of the HFI Portfolio, so all future write-ups will be included for HFI Research main subscribers.

Vermilion Energy (VET:CA) shares remain among the most beaten down in the Canadian oil patch. For years, they have traded at a discount to peers. Based on our 2024 estimates, VET shares trade at 2.5-times cash at today’s commodity prices. If they traded at a peer multiple of 3.4-times, they would trade at $20.68, representing 33% upside from their current price of $15.50.

The persistent discount and hope of a multiple re-rate have made VET a favorite holding among oil and gas bulls, who point to its:

Cash flow torque to higher oil prices.

Growth prospects in Canada and Europe.

Attractive natural gas price realizations.

Reasonable debt level.

Net debt target being hit, leading to 50% of excess cash flow being allocated to debt reduction and 50% being returned to shareholders.

Large share repurchases, with 4.3 million shares repurchased year-to-date, 2.7% of shares outstanding.

3.1% dividend yield.

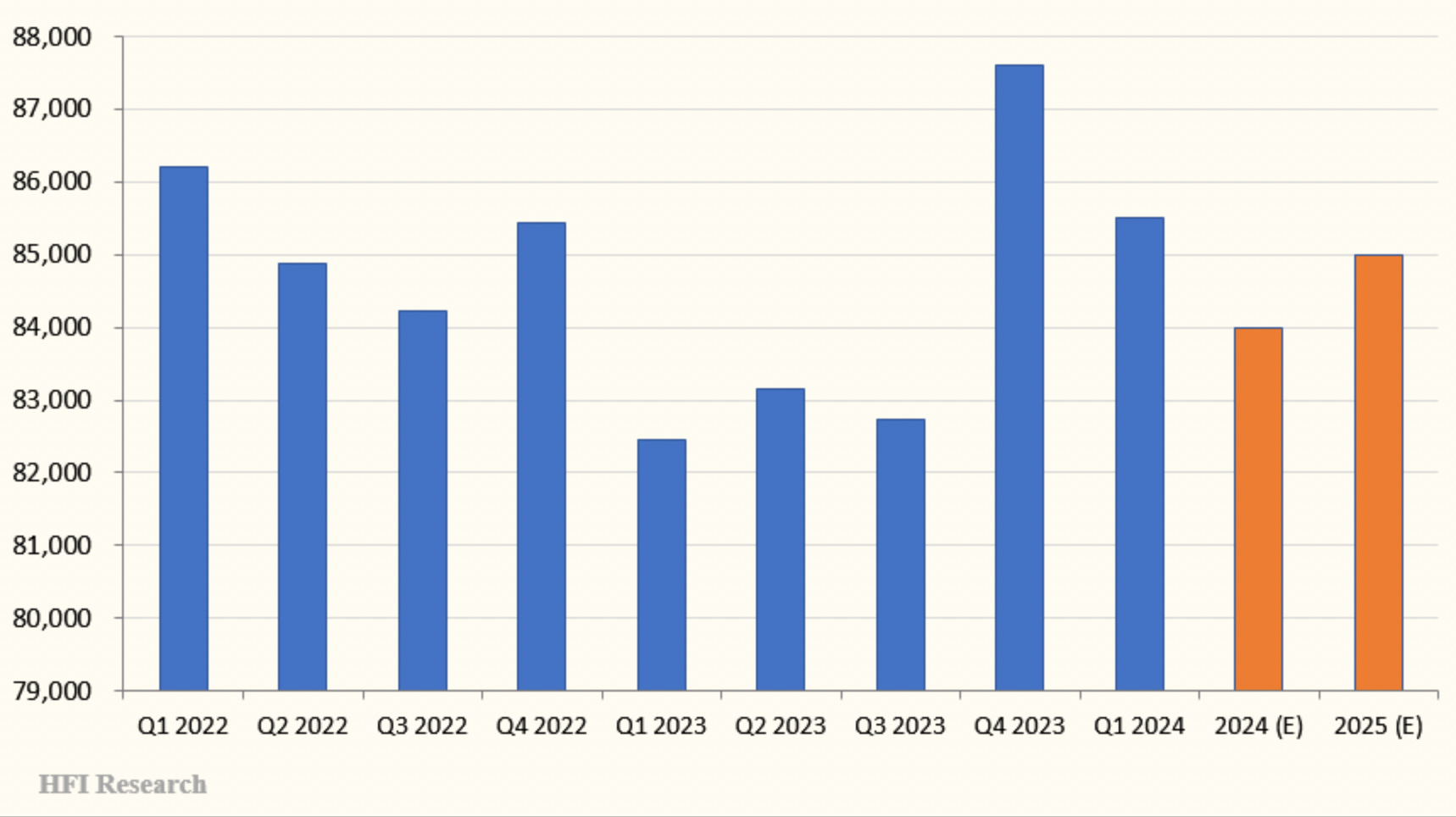

Moreover, recent results have outperformed. First-quarter production beat consensus expectations, coming in at 85,506 boe/d versus expectations of 84,000 boe/d. The company is seeing success in new wells drilled in Germany and Croatia. It plans to expand operations in those countries. VET has continued to focus capex on its Montney operation, with progress in developing the infrastructure necessary to boost production in the basin from 16,000 boe/d to 22,000 boe/d.

While VET’s momentum is clearly favorable, we see good reason for its shares to continue trading at a discount.

A Closer Look Reveals Concerns

Our first concern with VET is that despite the recent drilling successes, production isn’t growing. In the second quarter, production is expected to fall to 82,000 boe/d, while management is guiding for full-year 2024 of 84,000 boe/d. We expect only a slight increase in 2025 to 85,000 boe/d, which remains in line with the previous three years.

VET Quarterly Production

In itself, lack of growth isn’t a problem. However, VET has also been challenged to grow its reserves. In fact, PDP has trended lower since 2019, as shown in the second column in the table below.

Failure to replace depleting reserves will spell trouble for VET shareholders in the future. This is one reasons for the stock’s valuation discount.

Aside from declining PDP volumes, there have been other concerning signs for VET’s reserves. In the fourth quarter of 2023, the company reported a $1.0 billion impairment charge tied to a technical revisions to its reserves caused by higher-than-expected well costs in its French operations and poor drilling results in its Saskatchewan and U.S. acreage. These revisions contributed to an 8% decline in proved reserve volumes and a 13% decline in proved-plus-probable reserve volumes.

After the revisions, VET’s proved reserves span 8.75 years and proved-plus-probable reserves stand at 14.0 years. While not a cause for concern, if the company fails to replace its reserves, even sustained flat production will turn it into the E&P equivalent of a melting ice cube.