If These Two Variables Pan Out, It's A Matter Of How High Oil Prices Can Go

IEA released its latest oil market report last week. And in it, this is the most important chart:

Source: IEA

According to IEA's data, Q4 oil market balances turned out to be net builds as the builds were primarily driven by non-OECD and oil-on-water.

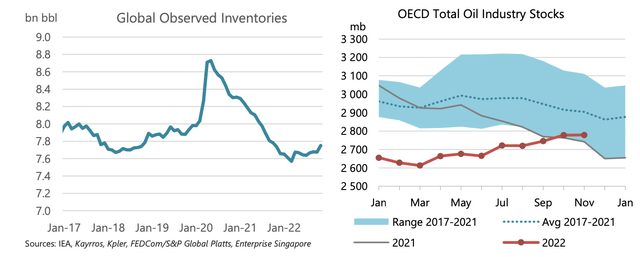

Oil-On-Water and Floating Storage

For November, IEA noted that global observed oil inventories increased by ~79.1 million bbls. And since Q4 turned out to be builds as opposed to the draws we had expected, this alters the calculus for Q1 balances. From the high-frequency data points we collect, OECD inventories are expected to be down slightly in Q4, this was validated by the IEA data. But the builds in non-OECD and oil-on-water need to be accounted for. One thing to consider though is that oil-on-water has since normalized and fallen back into the normal range.

In essence, IEA expects oil market balances to remain in surplus in Q1 before tightening into year-end. The two main drivers will be Russia and China.

Russia

According to the IEA, it believes that by the end of Q1, Russia will have to shut in ~1.6 million b/d versus pre-invasion production levels because of the product export ban. As a result, IEA expects Russian oil production to fall ~1.3 million b/d y-o-y.

Source: IEA

We think this is overwhelmingly optimistic as Russia's energy minister has already guided to ~500k b/d to ~700k b/d of decrease. In addition, for those of you that remember IEA's warning back in April 2022 about Russia losing ~3 million b/d from "self-sanction", this appears to be another one of those optimistic assessments.

In aggregate, if we shave off ~800k b/d from the Russia supply loss analysis, we still come to the conclusion that global oil markets will be in deficit by Q3.

China

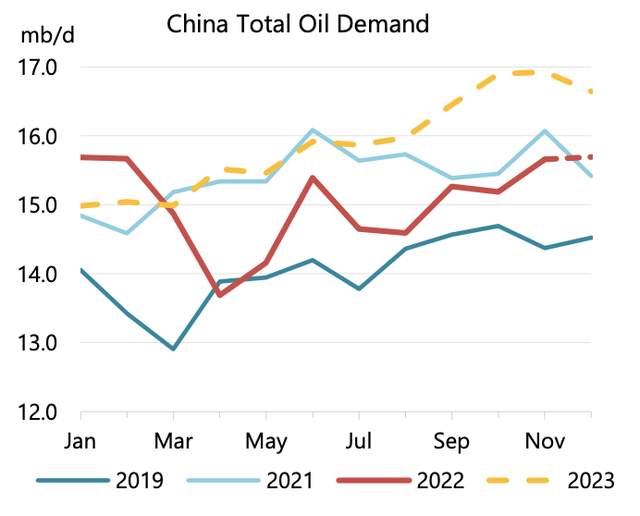

This is really the key variable that will determine whether oil prices will shoot above $100 by Spring or not.

Source: IEA

According to IEA, 2022 saw China's oil demand fall ~388k b/d y-o-y. And if you look at the segment breakdown, most of that was in motor gasoline and jet fuel (mobility related). Other products are essentially offset by the other various product segments, so we won't take that into account.

So assuming mobility increases (which is precisely what we are seeing) and given that all restrictions have been lifted, we should see a material jump in oil demand in the coming months.

Source: IEA

And as you can see, 2023 demand starts to eclipse that of 2022 by a significant margin starting in April. Remember that in April 2022 was when we saw the Shanghai lockdown, so the y-o-y delta will be massive.

In essence, we are leaning towards the camp that IEA is underestimating the amount of demand rebound we will see from China. We think IEA could be below the real figure by ~500k b/d to ~700k b/d by year-end.

Interestingly enough, China's potentially higher oil demand will offset the optimistic supply loss in Russia. In aggregate, the net result is the same, which means that if IEA's analysis holds, then we will see the global oil market balance tip into a -2 million b/d deficit by year-end.

And there are material implications of this on price and government policies. For starters, if by the middle of this year, China's oil demand is surprising to the upside, and Russia actually shows some type of production loss, then IEA will start to echo concerns that another global coordinated SPR release will be needed.

Source: IEA

The problem they will encounter this time around is that OECD government stocks cover by days will be below 30 days. This is, theoretically, the danger zone.

So we will have to see whether politicians have the appetite for more SPR releases. And given that there are no elections this year, we think there's a higher chance of them stomaching higher oil prices than jeopardizing more SPR releases.

Conclusion

China and Russia will be the main drivers of the oil market this year. "How much will Russia's oil production fall" and "how fast will China's oil demand recover" will be the two key questions to solving how high or how low oil prices can go this year.

If things go our way and Russia does in fact lose ~500k b/d to ~700k b/d, while China shows +1.3 million b/d y-o-y in oil demand growth, then it will be a question of how high and how fast oil prices go.

If things don't go our way and Russia doesn't lose any production, while China only shows +0.5 million b/d y-o-y, then the Q4 deficit will fall from -2 million b/d to -0.4 million b/d. But even in this scenario, oil prices will remain elevated between $85 to $95.

In my view, the set-up is asymmetric for the second part of this year. The only question we don't know from now to H2 2023 is how much global oil inventories will build in Q1. Going back to our baseball analogy, the crappy hitters are up first, so we still need to remain cautious.