Iran Is Already Back On The Market

In our base case assumption, we are assuming Iran is already back on the market and producing close to ~3.3 million b/d. In this article, we will explain how we arrive at this conclusion and what this means for the global oil market going forward.

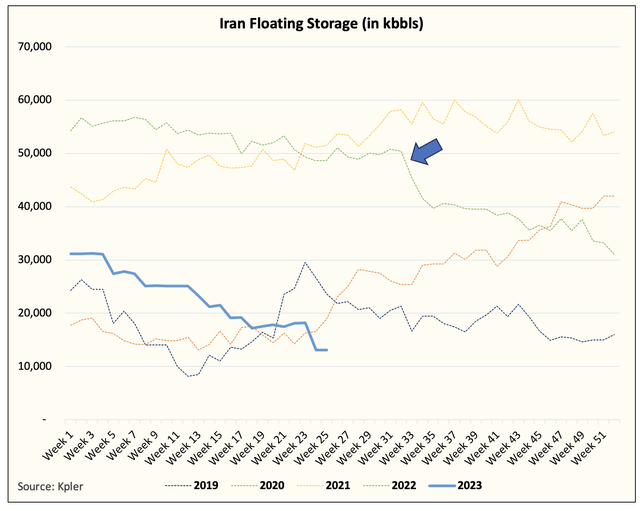

For readers that have followed our analysis closely, you may remember the chart on Iranian floating storage.

We pointed out before that the material decline came in Q3 2022 and just before the US midterm elections. Interestingly enough, the timing of the floating storage decline coincided with the IEA global coordinated SPR release. Keep in mind that China was still in COVID lockdowns during that timeframe, so buying was more or less muted.

The sudden decrease prompted us to rethink the Iran variable in our model. This was further sparked by a tweet from Javier Blas pointing to insanely high Chinese crude imports from Malaysia. So I wanted to dive deeper into the data, and this is what I found.