My Latest Thoughts On Oil Amidst Iran Tensions And Natural Gas

The energy markets are moving fast these days. Since we started combining the two (oil and natural gas) into one article at the beginning of the year, reader engagement has increased, and we’ve received some very positive feedback. With that said, these types of updates are more related to trading purposes than the WCTW articles, which are tailored towards long-term themes.

As we always caution readers, the long-term is made up of short-term events. In order to be directionally right, we also need to understand the key short-term drivers of the markets. In both the oil and natural gas markets, this becomes obvious the longer you are in the business.

With that said, let’s go straight in.

Oil Market

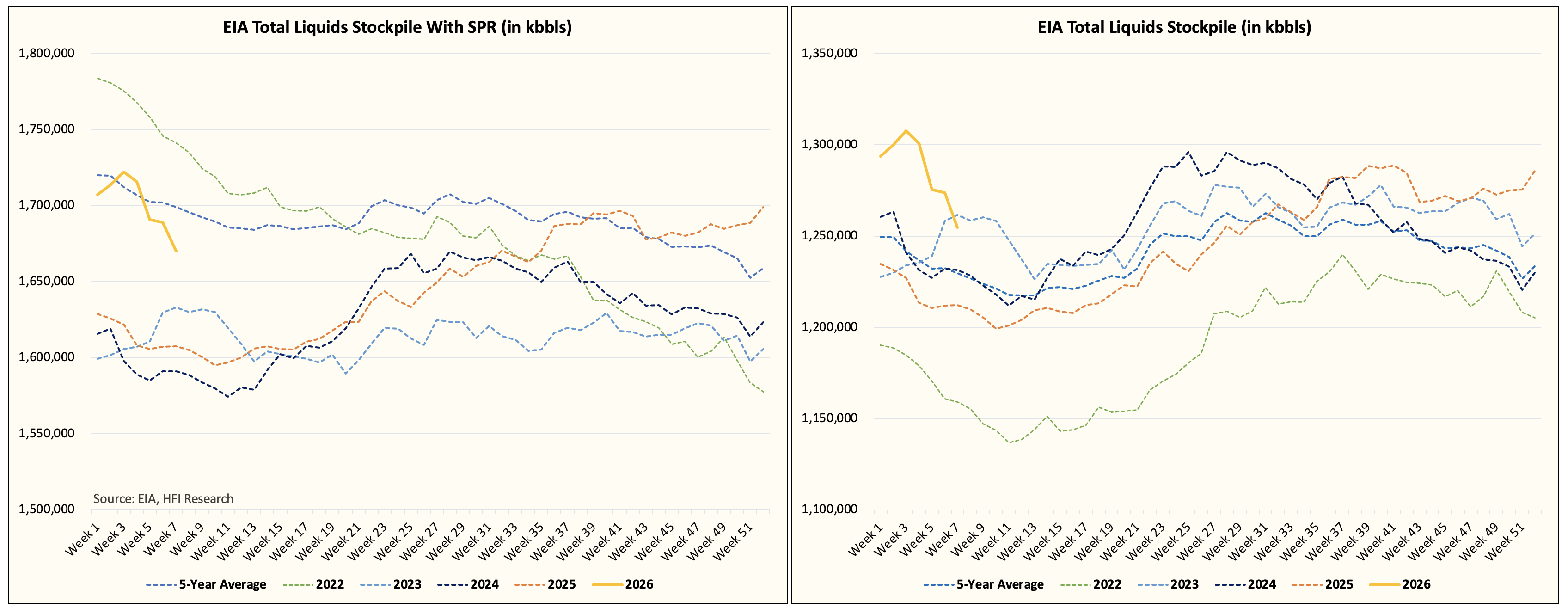

Oil prices have been on a nice run as of late. EIA reported a very bullish oil storage report with total liquids down ~19.1 million bbls.

This is in stark contrast to the massive builds everyone had coming into 2026. As we said in January, most of the people who follow the oil market have no idea how much a cold blast impacts supply & demand balances. In this case, both the freeze-off in US crude oil production and spike in heating-related demand have pushed balances to the bull side.

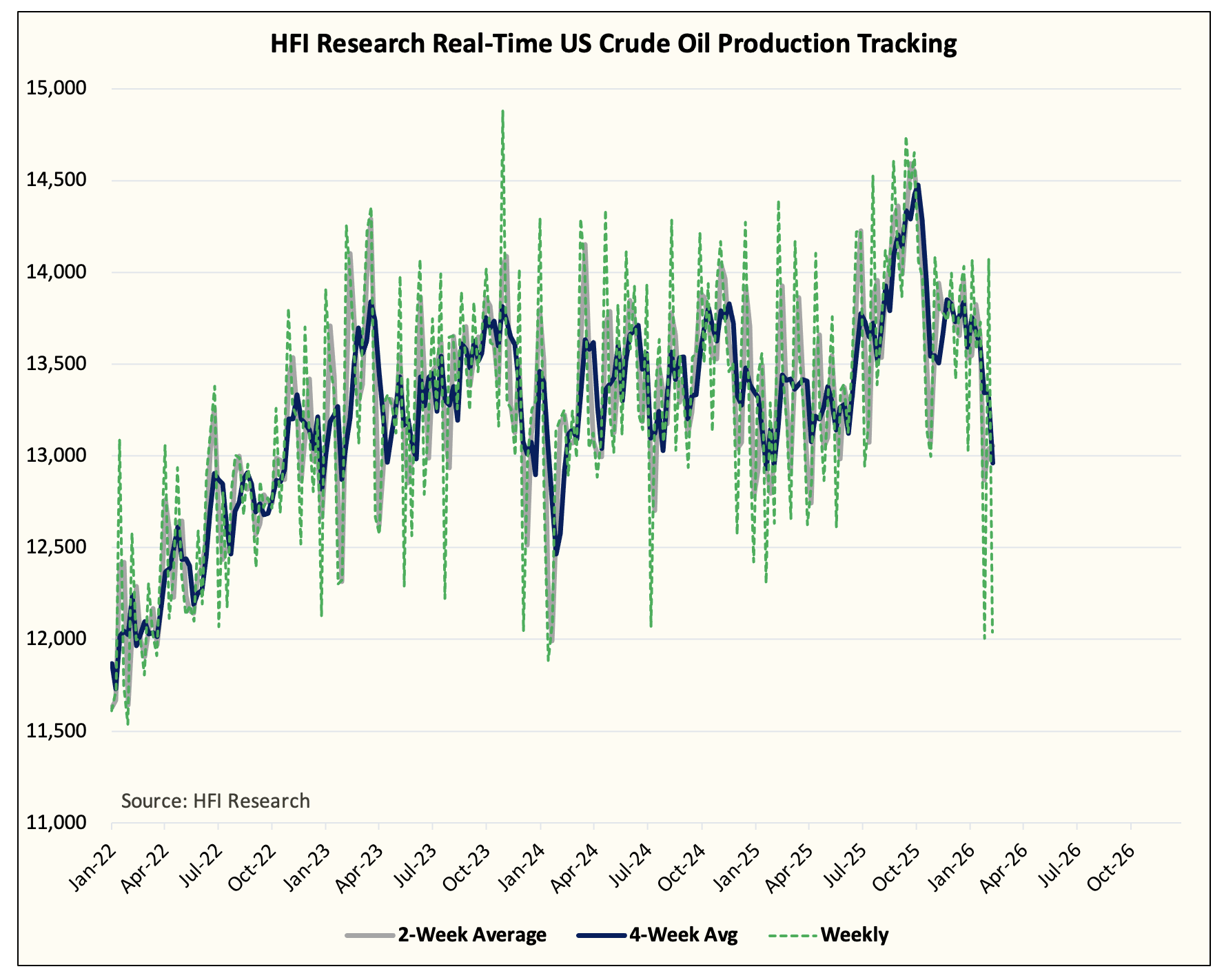

Today’s EIA oil storage report was particularly notable because of the big drop in implied US crude oil production.

We do think data quality issues have resurfaced following the cold blast. Our modified adjustment figure suggested real-time US crude oil production reached ~14 million b/d last week before plummeting to ~12 million b/d this week. To take the noise factor out, we revert to the 4-week average.

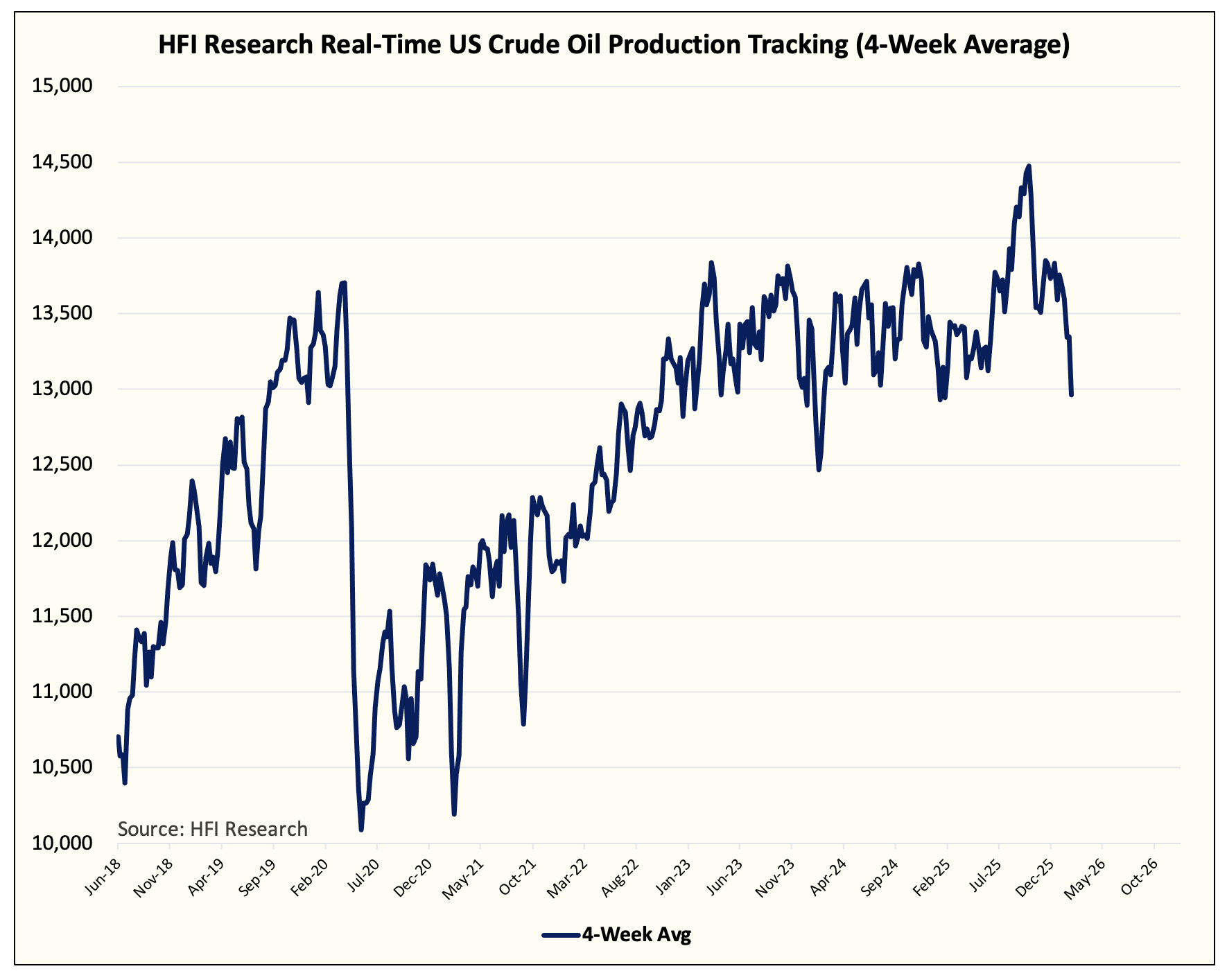

Our real-time US crude oil production model shows no real uptrend in growth. The big jump we saw in September last year was the result of data quality issues arising from the US government shutdown. Now that’s passed, those elevated production numbers were not sustained.

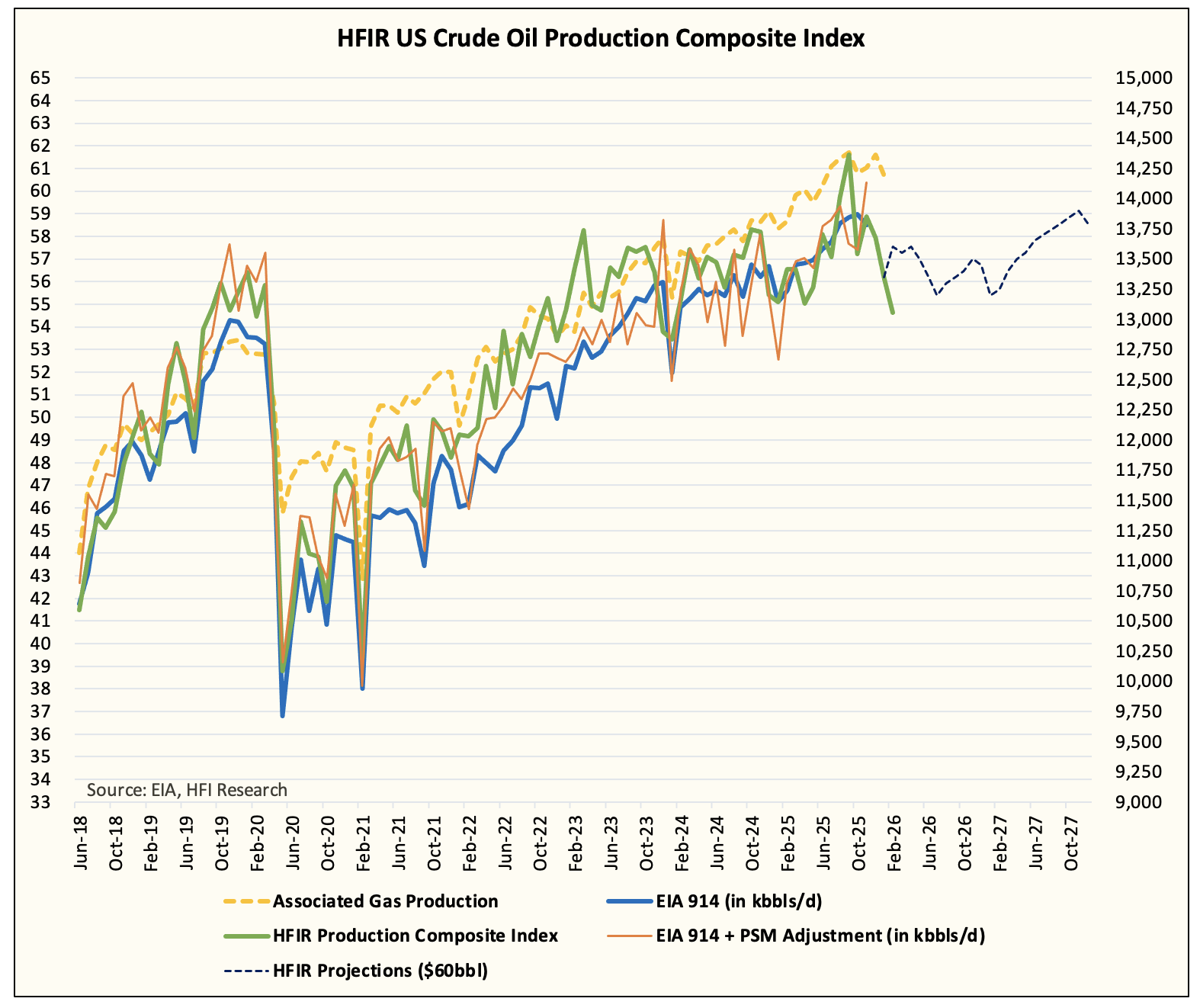

Looking at our US production matrix, the disappointment in February is larger than we had expected. We still have two more weeks of data to digest before the numbers are finalized, but it appears US crude oil production will settle in February around ~13.3 million b/d. This is a major drop from the ~13.8 million b/d we saw at the end of 2025.

With US total liquids disappointing the IEA’s massive glut narrative, I think more and more oil analysts are starting to realize that balances in 2026 are not as bad as advertised.

But now is not the time to get even more bulled-up. No, now is the time to be cautious!