The natural gas market today is in perfect equilibrium, which usually means that it's never smooth sailing from here.

But all kidding aside, Lower 48 gas production is reacting exactly as we had thought when prices started to tank in July. Because many of the natural gas producers in the US curtailed production in the form of TILs (turn-in-line wells), the moment prices spiked, they needed just 4-6 weeks to ramp production up. Similarly, as prices started to tank, producers could delay TILs, and let natural decline take place.

The delay in TILs coupled with pipeline maintenance is the reason why we've seen production drop from ~104 Bcf/d at the end of July to ~101 Bcf/d today.

On the surface, natural gas bulls have a lot to cheer about right now.

Natural gas storage surplus is dwindling.

South Central storage surplus is dwindling.

Power burn demand is being materially understated according to implied balances (more on this later).

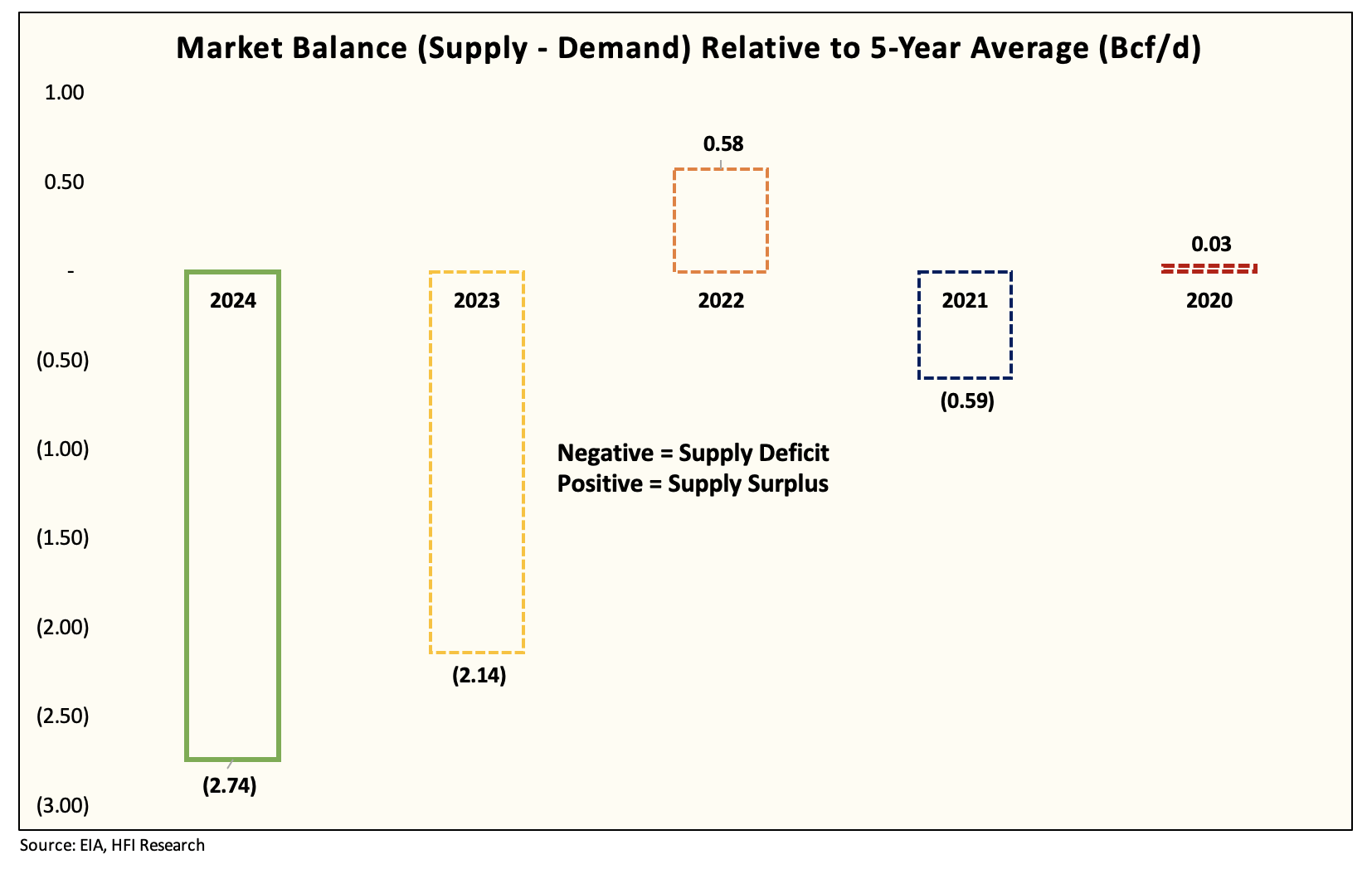

Implied deficit jumping to -2.74 Bcf/d, or the tightest we've seen fundamentals in the last 5-years.

With all of these positive variables in favor of natural gas, why aren't we more bullish on prices?

Well, the sad reality is that low prices are what's creating the deficits we are seeing. The ramp-up in production from June to July is a signal to the natural gas market that producers are ready to react. And since total gas storage remains on pace to hit ~3.9 to ~4 Tcf by November, the market will not allow producers to ramp up TILs ahead of the winter heating demand season.

This is why we are still seeing such a large contango curve in the market today.

And since the market is usually smarter than it looks, we don't expect any meaningful price move higher from now to October. This is the equilibrium and it's in the bulls' favor to have prices remain low for a while longer.