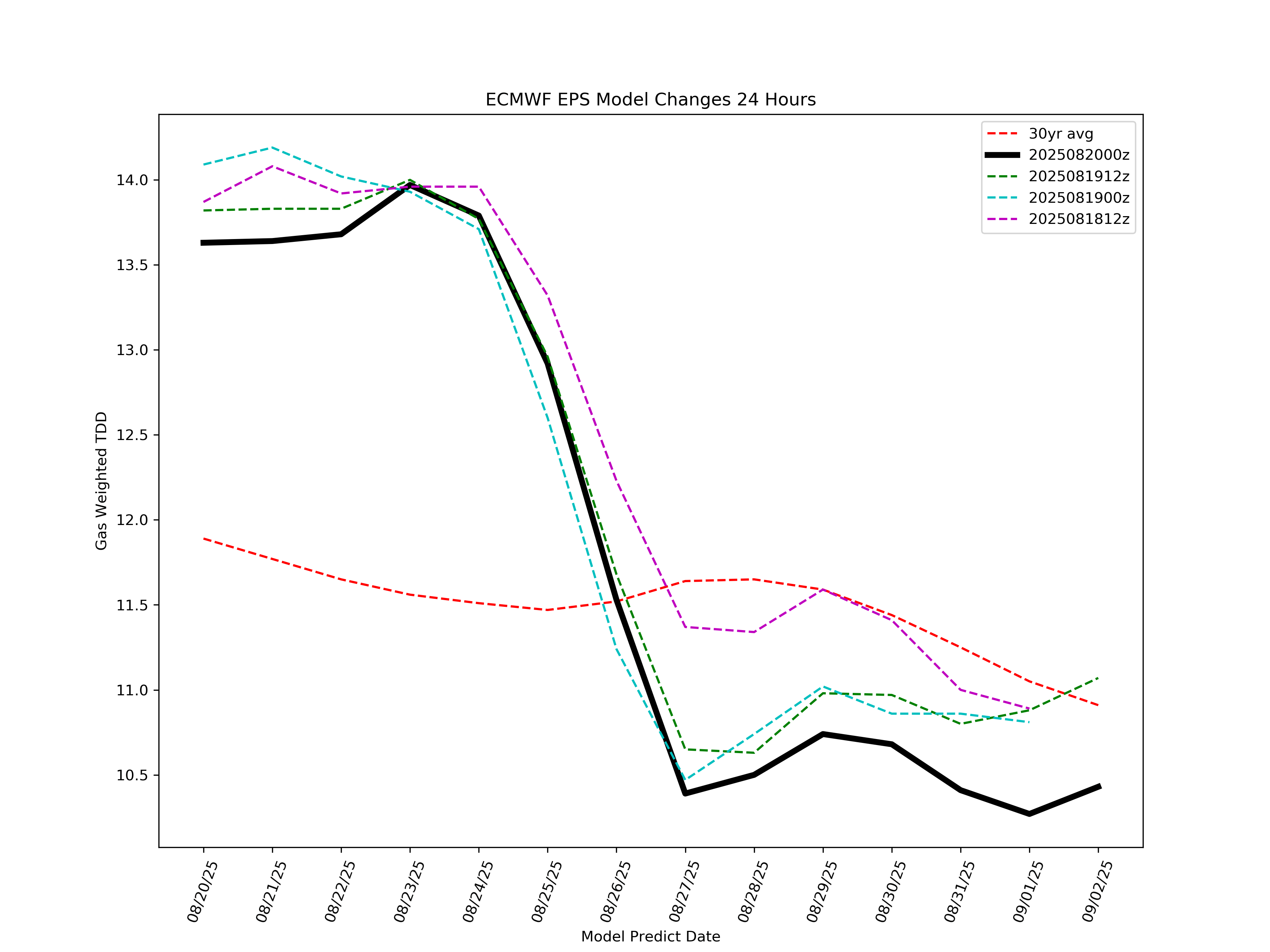

The summer power burn demand season is coming to an end, and what a disappointment it was. The back half of August has progressively turned cooler than normal to the point of making August 2025 the coolest August since 2017.

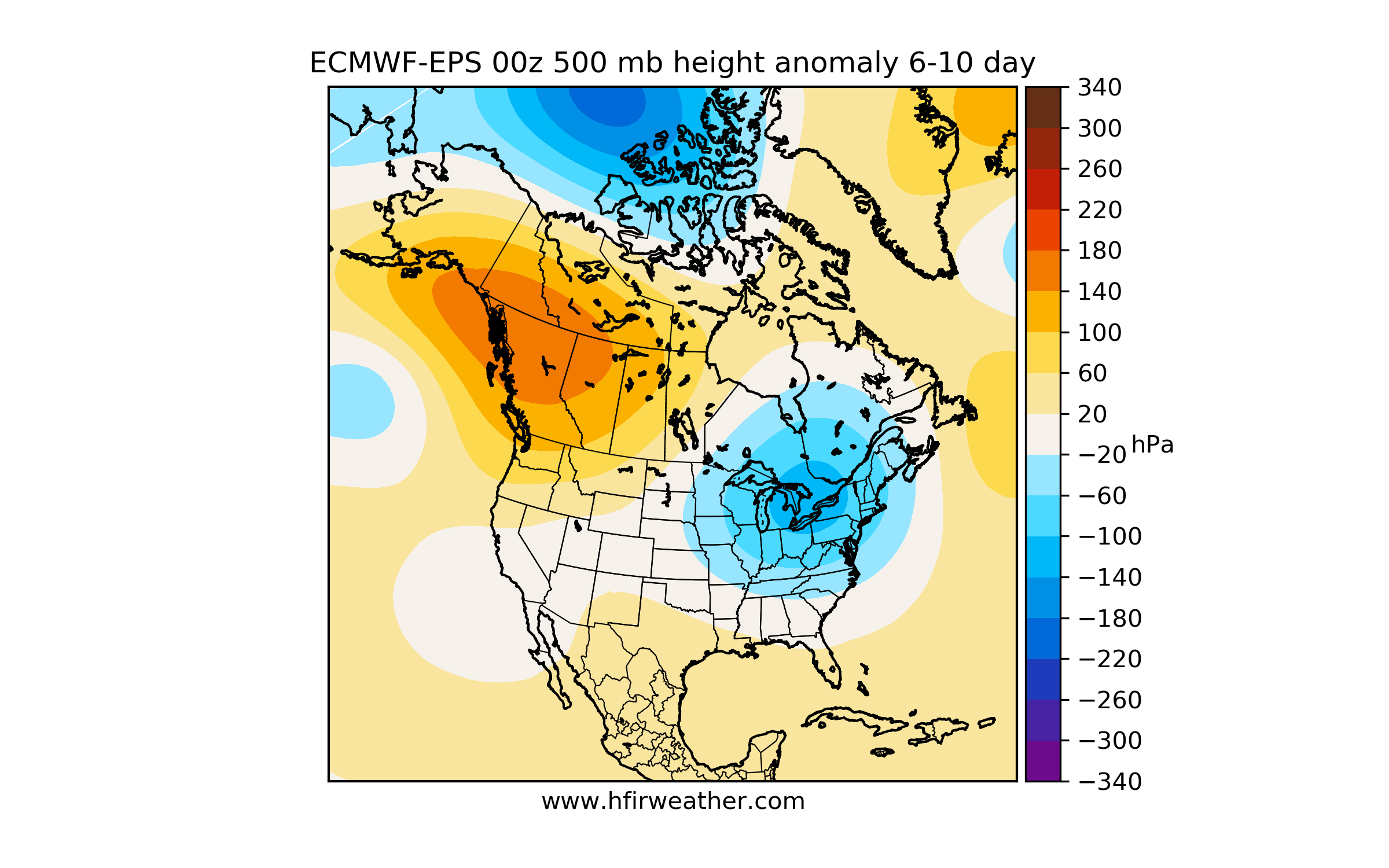

Looking at the TDD chart, you can see the material drop-off in cooling demand starting on August 26. From a weather model standpoint, this is what it looks like.

This is the type of weather pattern you want to see in the heart of winter, not the heart of summer.

The market, as a result, sent September contracts down to $2.75/MMBtu, which is ~$0.21/MMBtu below the Henry Hub cash of $2.96/MMBtu. As power burn demand starts to drop into the month-end, the cash market will gradually weaken, which is what traders are banking on (with the price drop).

But the other important message the market is sending right now is the one it's telling producers: stop increasing production.

The recent drop has pushed the 2026 curve below $4/MMBtu, and it doesn't matter that there's +3 Bcf/d of LNG capacity coming on by year-end or +4.3 Bcf/d by early 2027. All that matters is the near-term market balance, and traders are sending a clear message: stop.