In all my years of following the natural gas market, I have never seen summer-month contracts trade as volatile as the past 3 days. After bottoming on Thursday near $3.426/MMBtu, August contracts v-shaped recovered back to $3.745/MMBtu before falling to $3.448/MMBtu today.

Did fundamental factors justify such a chaotic price move? No.

But the bullish variables that were supposed to propel prices higher diminished over the weekend:

Cooler weather on the horizon.

Higher Lower 48 gas production.

What does this mean going forward?

As we wrote in last week's NGF, the weak cash market continues to be a headwind on financial prices. This did not change over the weekend, and I suspect some traders who went long into the weekend thought fundamental balances would tighten to warrant higher cash prices.

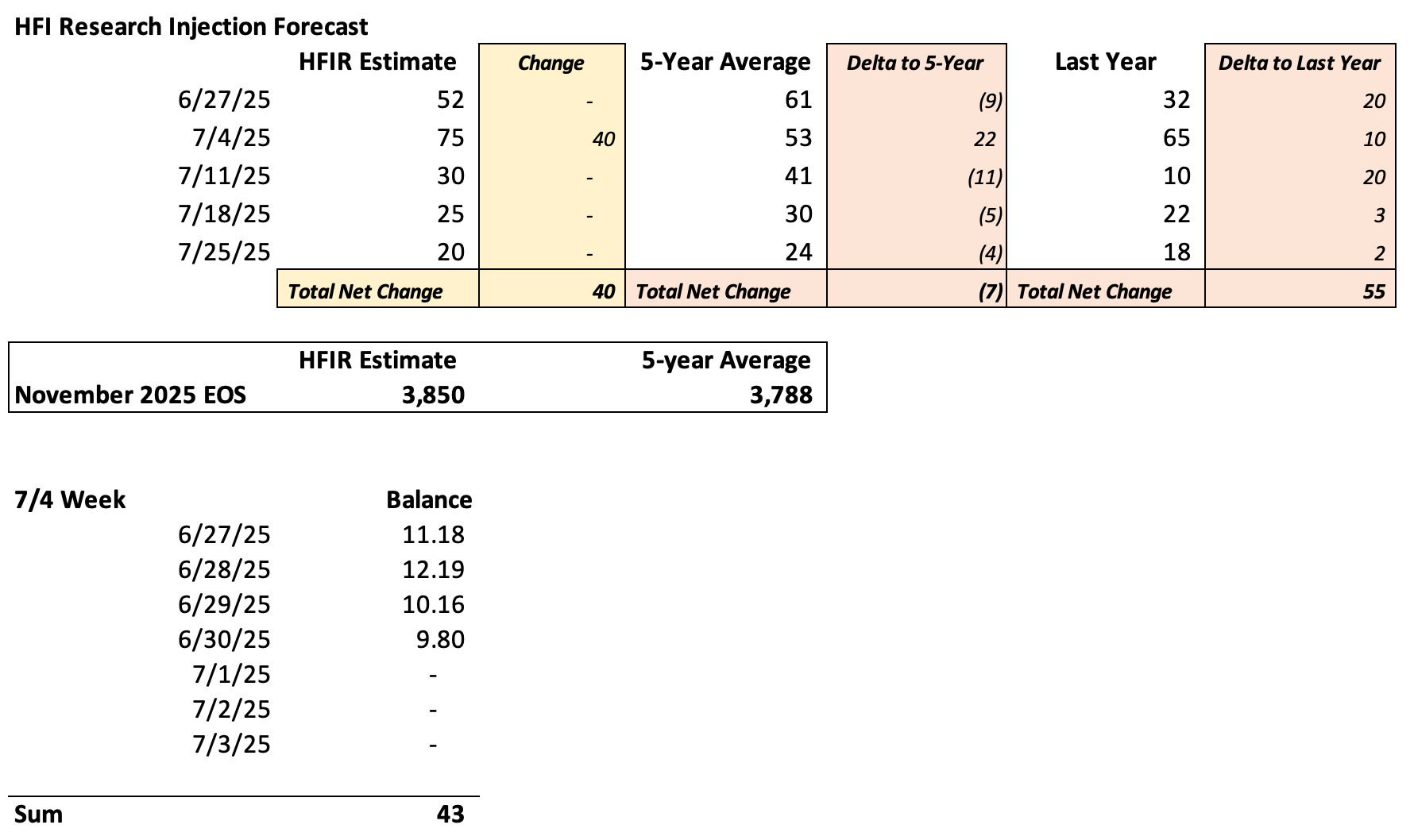

Looking at the implied balances for 7/4 week, our previous assumption was for storage injection to be between 35 to 45 Bcf. This would have been much tighter than the 5-year average of +53 Bcf and last year's +65 Bcf.

Instead, storage balances saw cumulative injections of 43 Bcf already and there are still 3 days left for the week. This implies a balance closer to +75 Bcf, which has also pushed our November 2025 EOS higher by ~50 Bcf.

Couple this with ECMWF-EPS weather model updates showing cooler weather in the back-end, and the market just sold first and asked questions later.

But even though everything seems bearish, there are a few facts that need to be known.