Mother Nature has not been kind to the natural gas bulls. In particular, ECMWF-EPS, nicknamed King Euro, has repeatedly disappointed the bulls with overly optimistic heat projections only to lose it in the following weather updates.

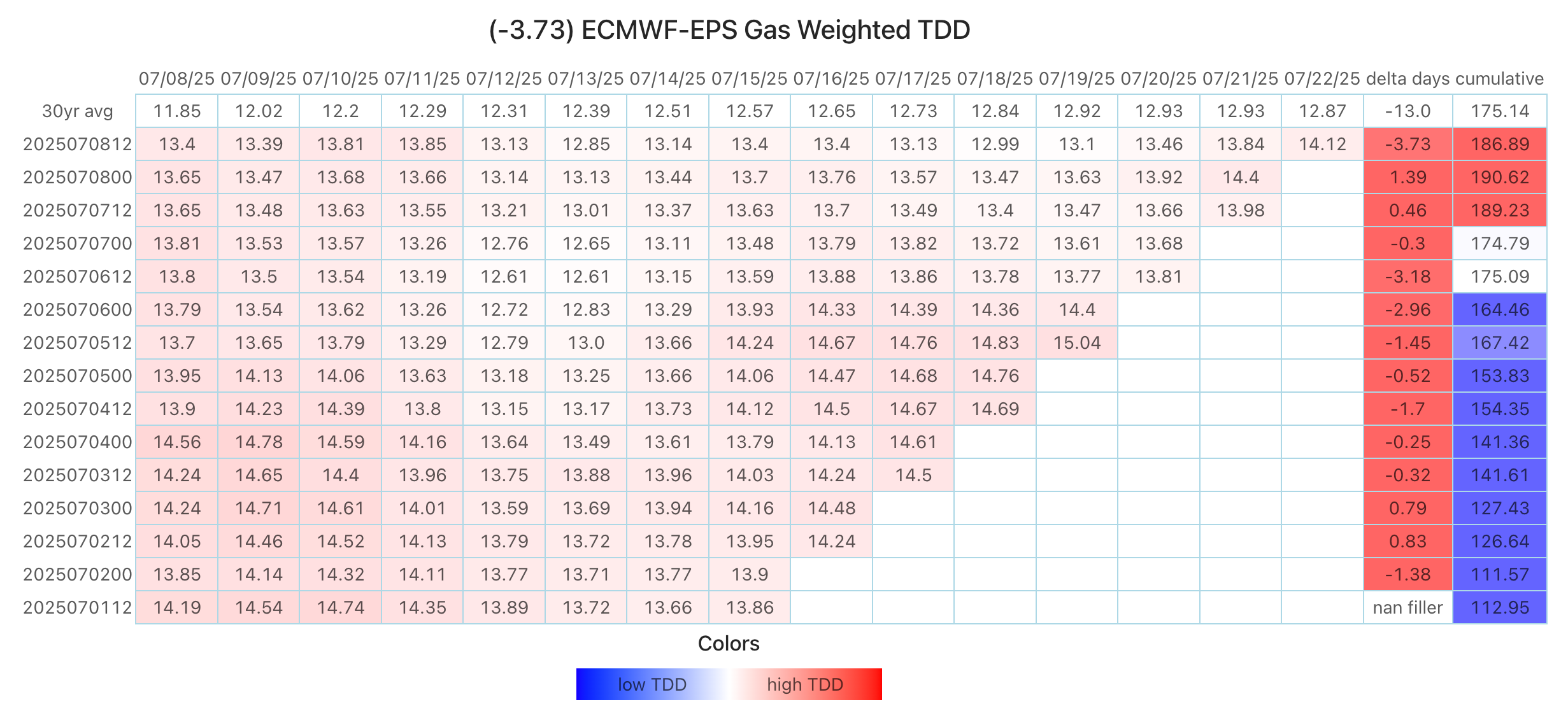

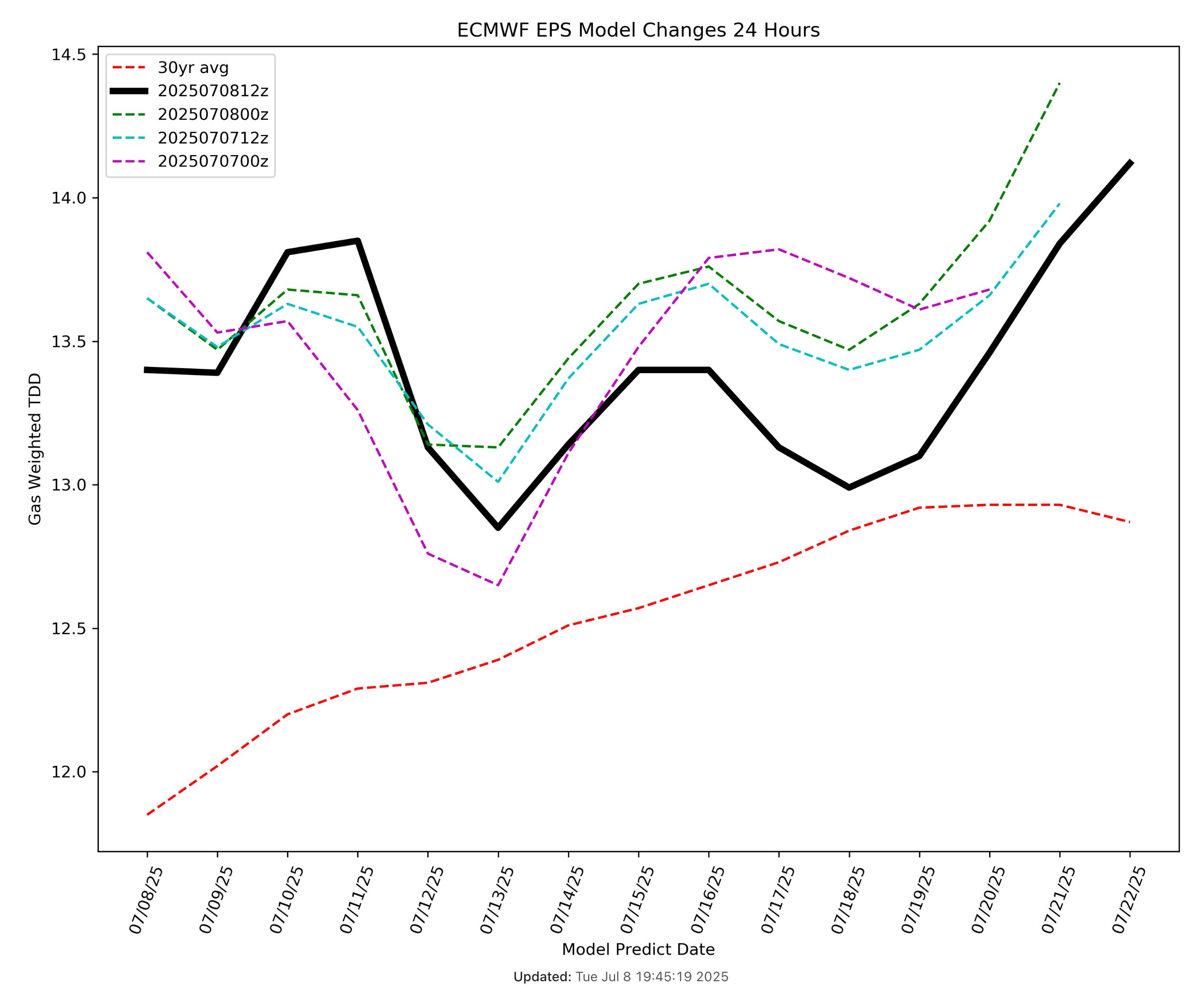

Our weather demand projection table best illustrates the recent phenomenon. On the right-hand side under the "delta days" column, you can see that since July 4th, ECMWF-EPS has consistently lost cooling demand.

The next 15 days show TDDs above the 30-year norm, but far from the "heat dome" prediction the model predicted at the end of last week. So while readers can look at this chart and conclude that the overall weather trend remains supportive, the issue is that the current cooling demand projection is insufficient to push prices higher meaningfully.

Running Out of Time?

At the start of the summer injection season, we argued that there's a case to be made for natural gas prices to surge to $5/MMBtu. With the +3 Bcf/d structural LNG demand coming by year-end, the market will start to fret over sufficient storage estimates if injections surprise to the downside.

Well, the surprise has been to the upside.

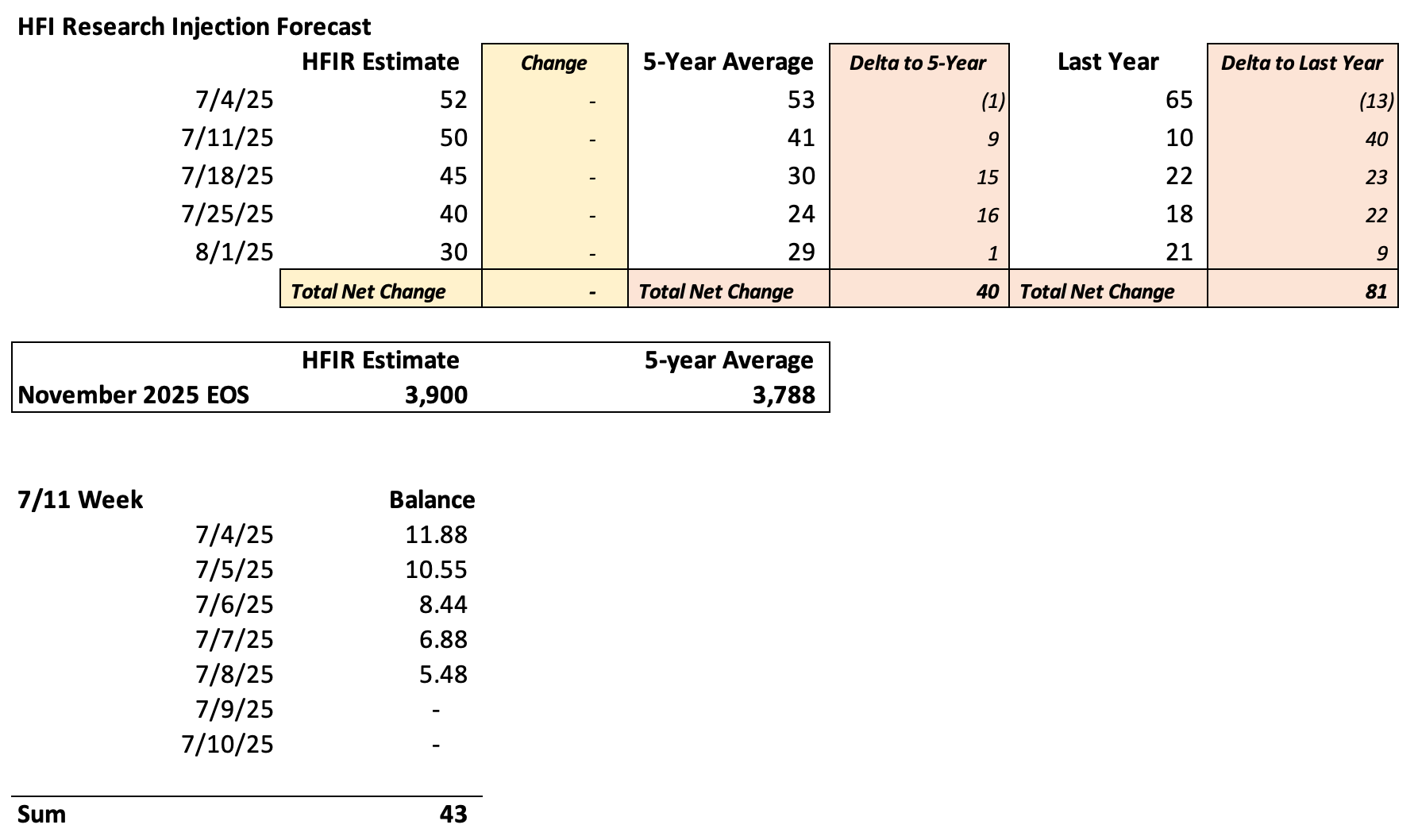

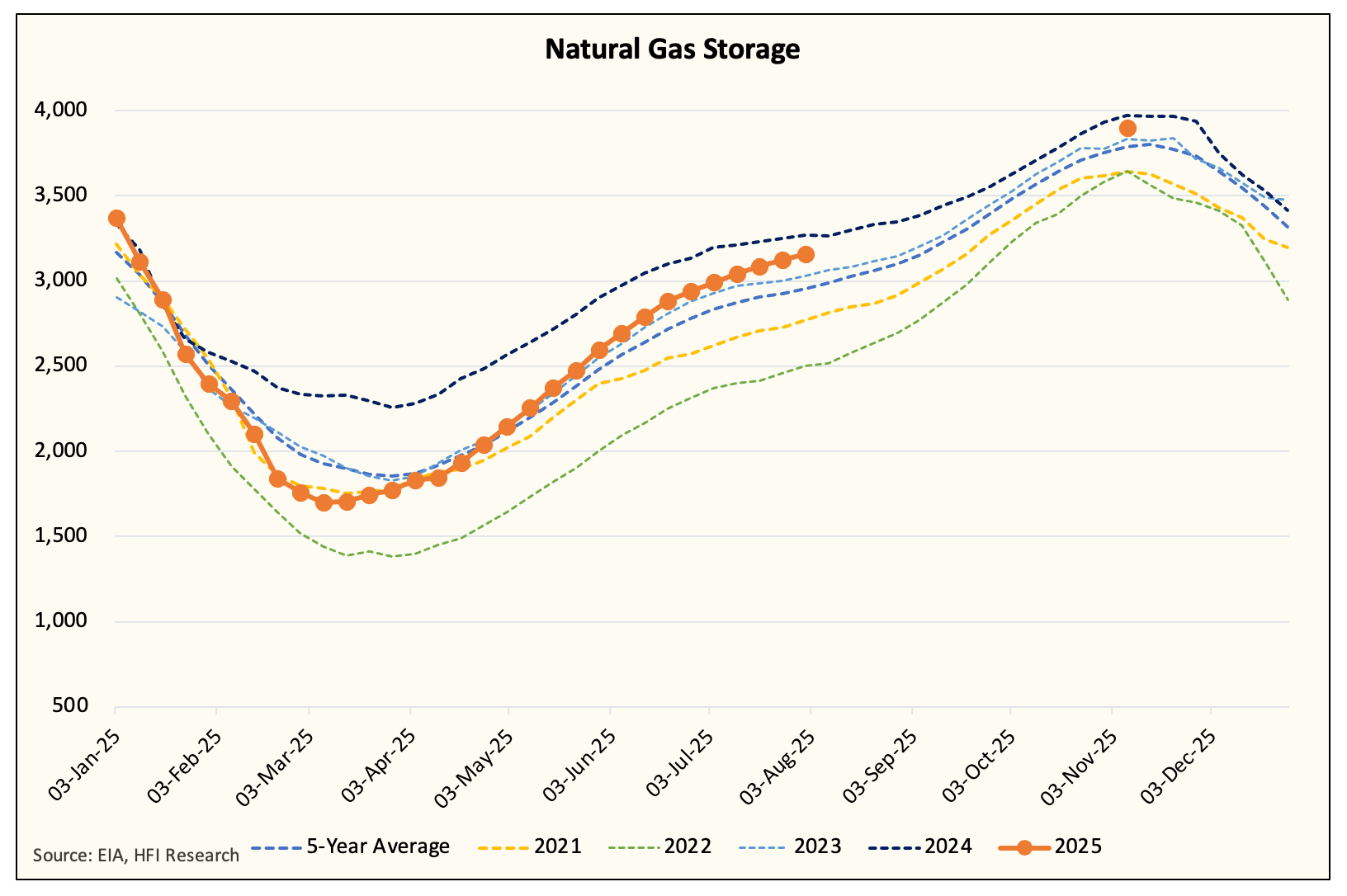

Injections are going to come in well above the 5-year average for the next 5 reports, and natural gas storage for November is projected to be between 3.9 to 3.95 Tcf, or 150 to 200 Bcf above the 5-year average.

Storage Projection

Storage

While overall storage will be below 2024 levels, that's not something to be proud of considering that at the start of the injection season, natural gas storage started 453 Bcf lower y-o-y.

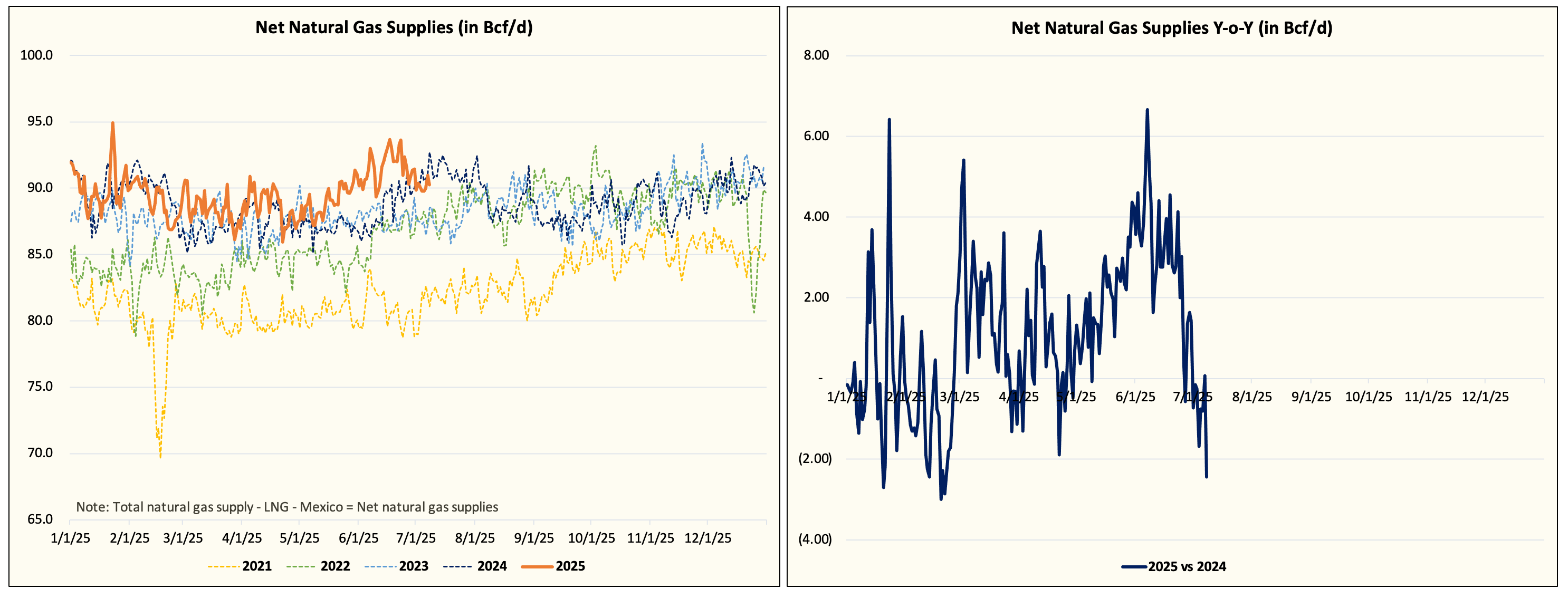

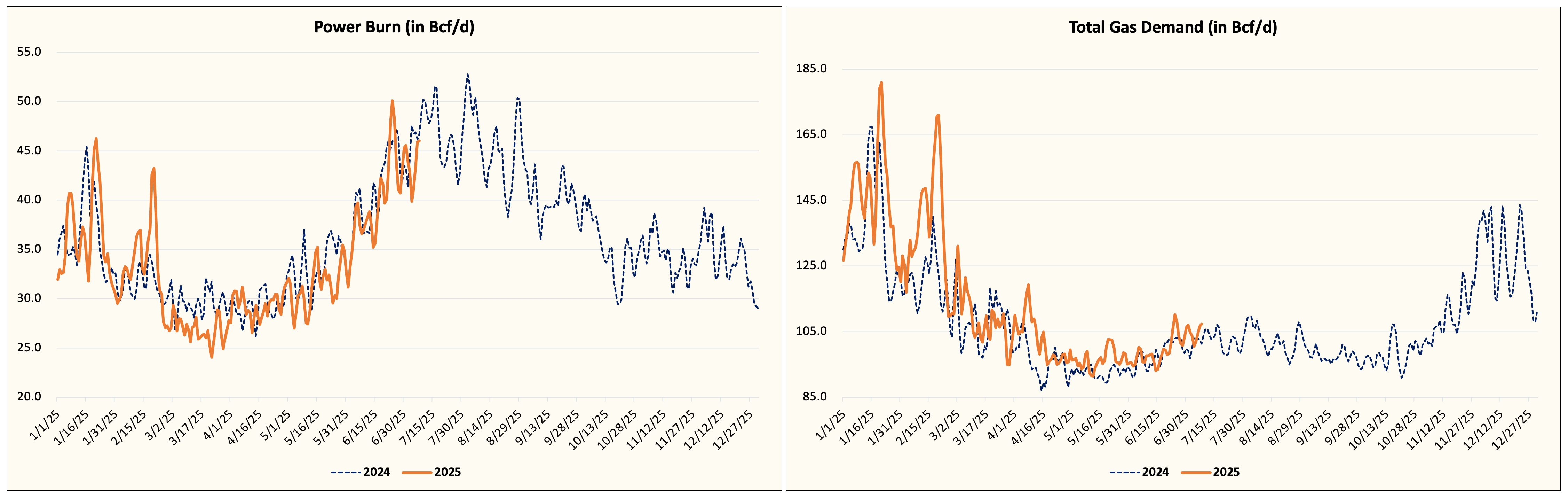

Looking at both the physical market and implied balance, it is obvious that the recent cooling demand is still insufficient to create a very tight market. The higher production y-o-y is only being partially absorbed by higher LNG and Mexico gas exports. Net gas supplies are finally down y-o-y, but power burn demand is lower y-o-y.

Net Gas Supplies

Power Burn and Total Demand

In essence, more heat is needed if we are to push total injections lower.

Downside vs Upside

Power burn demand is currently around ~46 Bcf/d, which is below where we were last year. The current cooling demand projections continue to escape the Southeast (as shown in the weather map below), which is creating a lot of anxiety in the physical market.

At $3.2/MMBtu average today, Henry Hub cash continues to keep a lid on the prompt month, while simultaneously providing a floor. Without much higher cash prices, it will be difficult for August contracts to meaningfully rally.

Does this mean the upside is gone for this summer? No, but with each passing day that the cooling demand gets revised down, the eventual upside is reduced.