On April 25, we published a piece titled, “B.A.C.D Is Coming To An Oil Storage Hub Near You.” In it, we said:

From now to the end of July, visible US crude inventories will decline by ~213 million bbls, the largest and fastest decline in history.

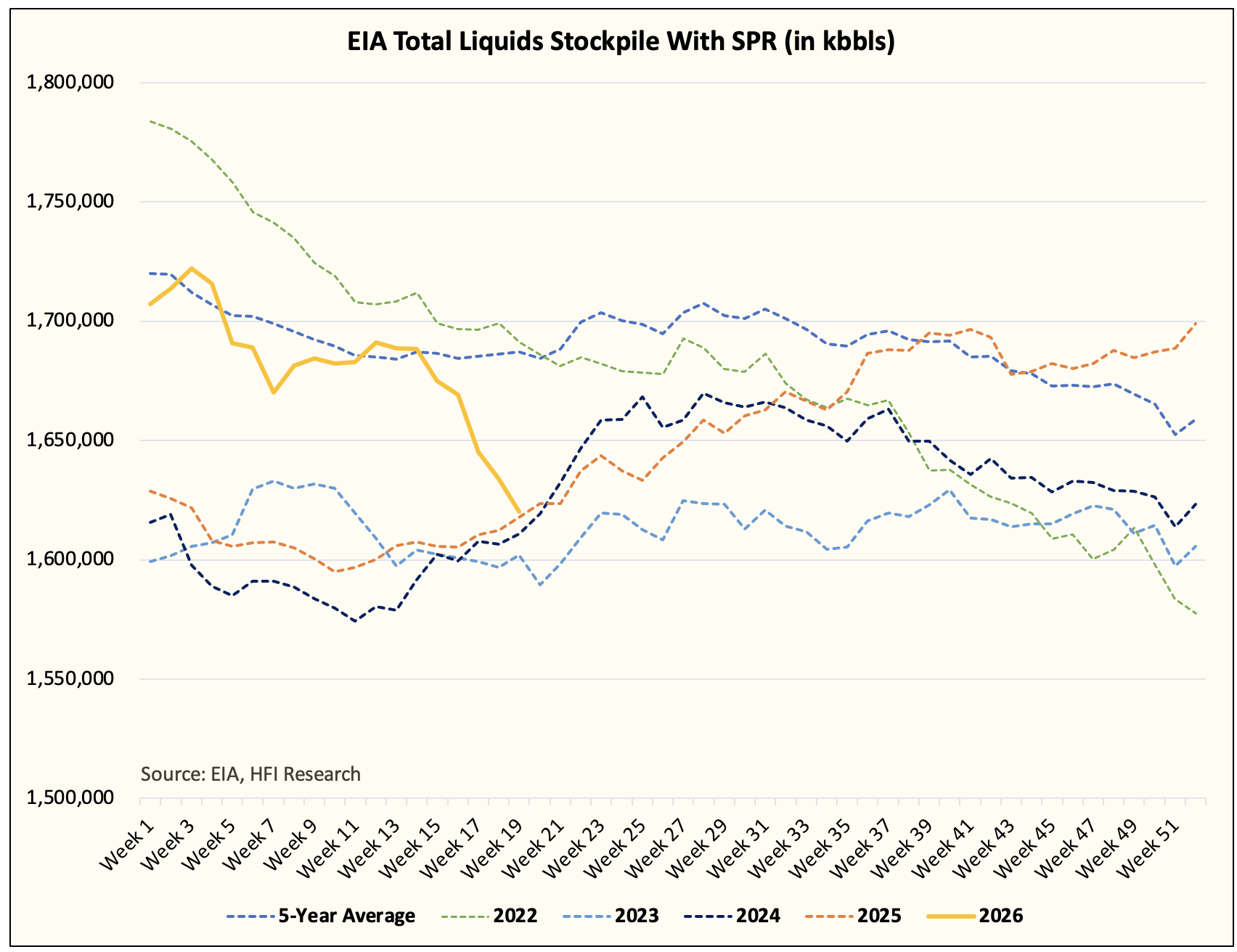

US total liquids with SPR will fall to an all-time low.

Yes, an all-time low.

Since EIA started publishing the data in Jan, 5, 1990, US total liquids have never breached 1.4 billion bbls.

This is happening regardless of what happens to the Strait of Hormuz. It’s too late already.

Fast forwarding to today, we are on pace:

US Total Liquids With SPR

In our April 25 report, we wrote:

Starting in next week’s EIA oil storage report, the US will average over 18 million bbls in total liquid draws.

Since then, US total liquids with SPR dropped 48.846 million bbls. We have averaged a draw of 16.282 million bbls per week.

Looking at current projections, US commercial crude storage is expected to decline steadily through the end of July. Refinery throughput has picked up, which will dampen some of the product draws we’ve seen, but crude draws will remain very heavy.

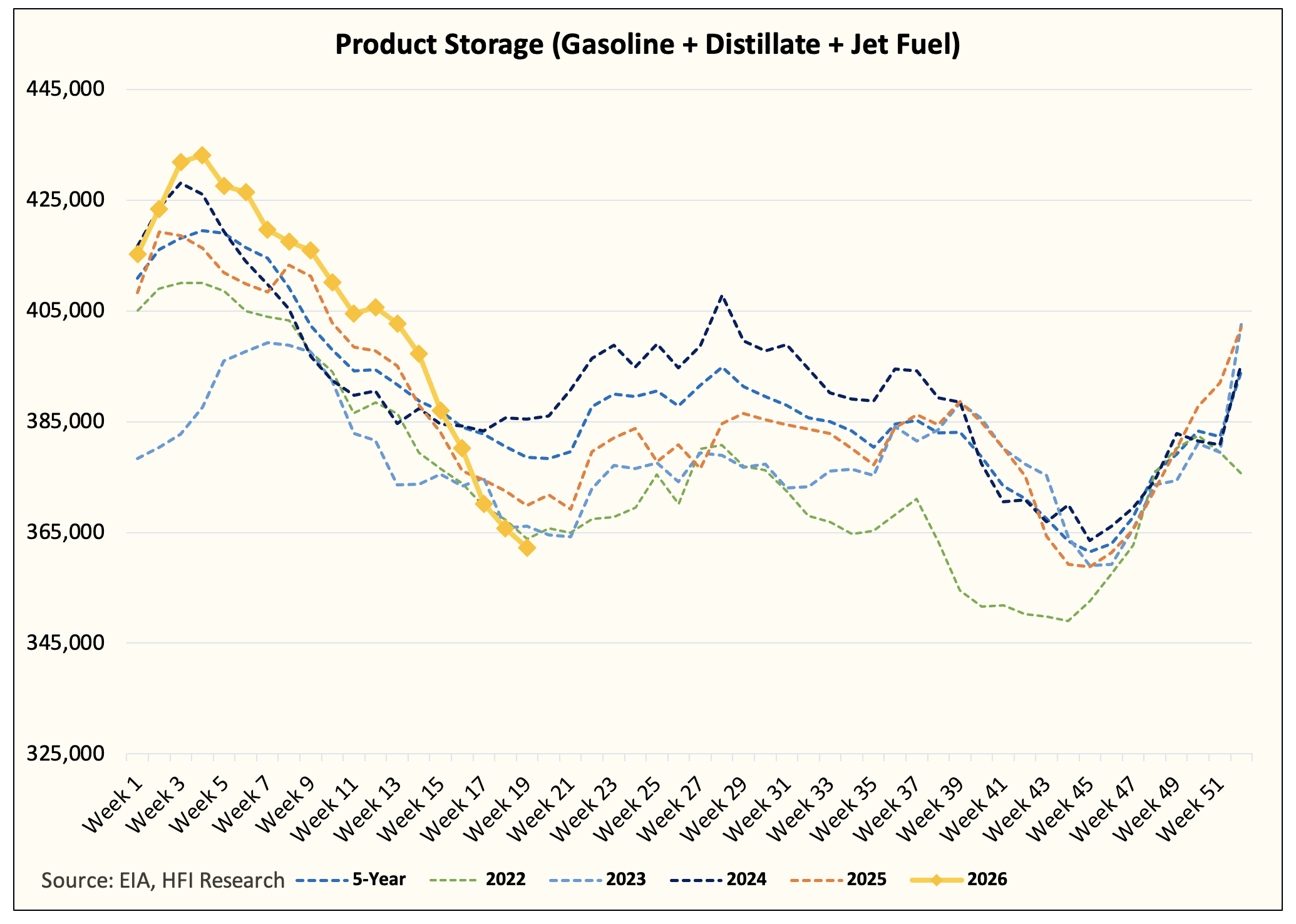

As you can see from the current product storage chart in the US, we are already running low on available products for domestic consumption.

In 2022, we had a global refinery capacity shortage, which saw refining margins rise disproportionately relative to crude. US refineries were incentivized to run at full capacity all year. You can see in the green dotted line above how low product storage stayed throughout 2022.

This time around, we have a crude shortage, but the lack of crude elsewhere has incentivized US refineries to run at max capacity going into the peak driving season. Product storage is now ~13 million bbls from the lows we saw in Q3 2022. We are about 3 weeks away from US petroleum product exports falling. Once the buffer is gone in the US, the elevated petroleum product exports that the world is enjoying will disappear.

Time is running out.