EIA reported an overall bullish storage report today, but as for the price action, I think we are witnessing WTI/Brent topping out for a bit here. Looking at our oil market signal chart, some of the indicators have turned bearish.

Source: HFIR

HFI Research is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

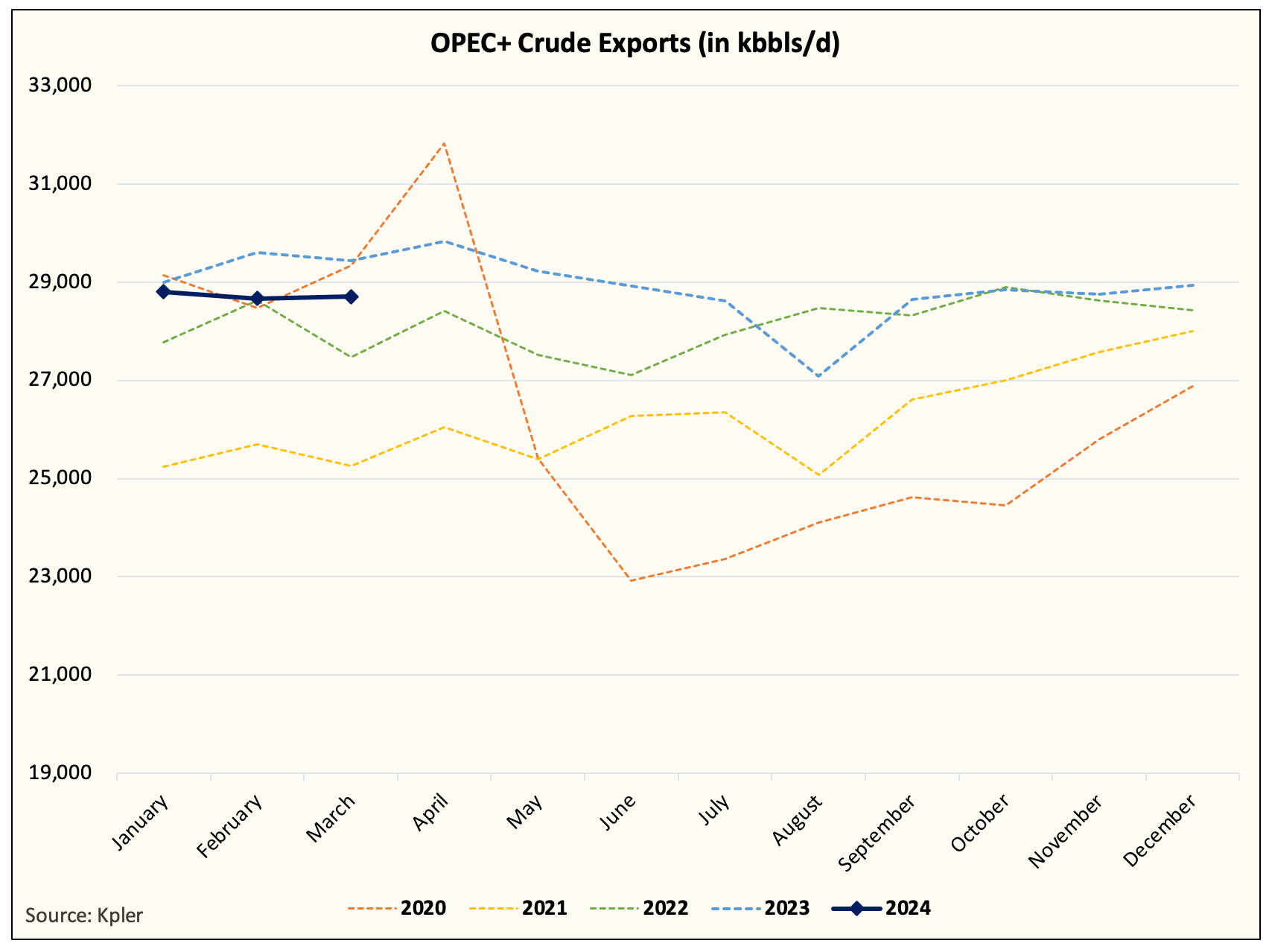

On the supply & demand front, OPEC+ crude exports are basically unchanged from a month ago at ~28.6 million b/d.

And as we head into peak global refinery maintenance season, the physical side is starting to soften a bit.

Brent 1-2 Timespread

Source: Barchart.com

Keep in mind, however, that this does not mean WTI will fall back to the low $70s. No, the conclusion should be that WTI is likely to be rangebound going forward until another catalyst (demand, probably) pushes prices higher. One key supporting factor for structurally elevated crude prices is elevated refining margins.

Source: Barchart.com

With the 3-2-1 crack spread trading over $32.50/bbl, refineries are heavily incentivized to come back as soon as possible to take advantage of the elevated margins.

This has and will continue to be our key leading indicator for the oil market this year. So long as refining margins remain elevated while crude prices grind higher, we believe the price move will be sustainable. If it doesn't rally in tandem, then we know a pullback is coming.

On the sentiment side, the market is not longer anywhere as bearish as we would like it to be. Sell-side is starting to come around the fact that global oil market balances are much tighter than expected. In turn, Morgan Stanley increased their Brent price target to $90/bbl this summer. Although they continue to incorrectly interpret the OPEC+ production cut, sentiment is changing, and bulls should be keenly aware.

Because of the recent price hikes we've seen, we've changed our sentiment indicator to bearish to reflect the optimism.

In essence, we see oil prices peaking for now with a much higher range. We could see WTI trade between $77 to $85 for the next few months.

Housekeeping Items

This week's weaker-than-expected crude draw from EIA stems from the very large modified adjustment figure. Due to the large crude export we saw in tanker activities last week, EIA likely has a lag on the data since it uses customs data versus physical movements.

As a result, EIA now owes us about ~8.344 million bbls, which will be returned in the following weeks.

Our preliminary figure this week shows a large crude build of ~7 million bbls. But thanks to the large discrepancy we saw this week, it's likely that EIA reports a small build instead.

Either way, the jump in modified adjustment is not sustainable, and EIA's reports over the next few weeks will correct this.

Energy Stocks to Benefit

Similar to the theme we discussed in this week's WCTW, "Energy Stocks Set To Materially Outperform Their Tech Counterparts." We believe a rangebound oil pricing environment will be materially beneficial to energy stocks.

For our WTI price forecast, we used $82.50 for this year's average. With WTI trading right around this price, our E&P valuation sheet universe shows an average free cash flow yield of ~12%.

Amongst the names we own, we get an average FCF yield close to ~15%.

We think a stable period of high prices will attract more investors as the potential of a price spike always opens the possibility of demand destruction down the road. With a period of stable but high prices, E&Ps can generate well above average return on capital, and in turn, shareholders would benefit from higher dividends or higher share buybacks.

One of our favorite names right now is Strathcona Resources. See the section below on its cash flow sensitivity and valuation (from our part 2 report):

Like other Canadian oil sands operators, Strathcona has tremendous cash flow torque to higher oil prices. It will be a prime beneficiary as the WTI-WCS differential compresses over the next few months as the Trans Mountain Pipeline expansion project enters service.

Assuming 190,000 boe/d of production growth, $1.3 billion of total capex, US$80 per barrel WTI, $2.50 per mcf AECO, and a $14.50 WTI-WCS differential, Strathcona will generate the following free cash flow yield on its current share price of $25 at different commodity prices:

If the shares were to trade at a 12% free cash flow yield, their return prospects at different commodity prices from their current price would look like the following:

Clearly, the shares have tremendous cash flow torque to oil prices. If WTI is sustained above US$90 per barrel, they offer more than 100% returns from their current price.

Our discounted cash flow value uses the same assumptions as above and values the shares at $34.02, which implies 36% upside.

Of course, production growth, commodity price increases, effective capital allocation, and sustainable cost reductions could all create further upside for shareholders.

Given the discount to value, we would prefer management allocate free cash flow to repurchases. However, large share repurchases would exacerbate the negatives listed above. While they wouldn’t reduce intrinsic value per share—quite the contrary, in fact—they would frustrate management’s intent to provide liquidity for Waterous Energy Fund investors, at least in the near term.

We therefore expect free cash flow to be distributed to shareholders via dividends. Strathcona is likely to establish a base dividend and pay variable dividends once it hits its debt target, which we expect in the second half.

Conclusion

Oil prices are going to be rangebound for a while. As sentiment has shifted to the bull side and the physical market weakening, we need refining margins to remain strong to keep crude structurally higher. Once global refinery maintenance season is over and global demand increases (seasonality), that will be the time for the next leg higher in crude.

Meanwhile, energy stocks should continue to benefit from the rangebound price action. As oil slowly grinds higher throughout the rest of the year, we see energy stocks materially outperforming their tech counterparts. This should be a very good year for energy investors.

Analyst's Disclosure: I/we have a beneficial long position in the shares of SCR.TO either through stock ownership, options, or other derivatives.

HFI Research is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.