By: Jon Costello

Last week, I made the case that fee-based midstream master limited partnerships (MLPs) are the income trade for an oil supply shock. Their cash distributions follow their throughput volumes, not commodity prices, so they will continue to pay even when crude or natural gas prices decline, eliminating cash flow for exploration-and-production companies.

Staying on the topic of MLPs, I want to reiterate our interest in Mach Natural Resources (MNR). Mach is an exception in the MLP world as an upstream E&P, the kind of business that is exposed to commodity price volatility. We expect it to benefit from sustained higher oil prices we expect over the second half of this year, and likely beyond. Its units, trading at $13.35, reflect none of the potential upside.

Mach is dedicated to paying out essentially all its cash flow after reinvesting 50% or less into the business. At the same time, it maintains a hedging program that locks in cash flow. The result is that the yield on its units provides downside protection, while its commodity price exposure offers significant upside amid sustained high oil and/or natural gas prices. Mach is therefore attractive as a long-term E&P income holding. For our part, we can reinvest the distributions into other high-return opportunities, which suits our situation particularly well.

We added 11,950 units to our HFIR Energy Income Portfolio at $12.69 per unit in April. The purchase added to our existing position of 7,050 units acquired on January 8 at $10.83 per unit, bringing the total to 19,000 units at an average cost of $12.00 per unit. As things stand today, the second-half setup makes Mach’s income and appreciation case stronger than it was then.

Mach Captures the Oil Upside While Maintaining Downside Protection

Mach is built differently from the shale operators it gets lumped with. It distributes its cash through a variable quarterly distribution that represents nearly all of its residual cash available for distribution. Consequently, the payout moves directly with the cash the business throws off. When an oil supply shock raises crude prices, the quarterly payout rises accordingly. The distribution structure makes Mach a long-oil instrument that happens to carry a coupon, the mirror image of a fixed-dividend producer that buys back stock and pursues other capital allocation policies that are questionable in terms of the value they add for shareholders.

Mach’s dividend also makes it far better protected on the downside relative to its E&P peers. The company’s cash operating cost runs near $11 per barrel of oil equivalent, and its corporate decline rate is roughly 17%. By contrast, Permian shale peers run $15 to $20 per barrel of oil equivalent and decline at 30% to 40%. I covered the figures at greater length in previous articles. The same commodity price slump that can wreck a high-cost, high-decline operator barely dents Mach because its low costs and slow decline keep the distribution flowing when crude falls.

The Hedges That Capped the Upside Are Rolling Off

The obvious objection to Mach’s second-half cash flow story is its hedges, which cap the extent to which it can capture higher oil prices. Look closer, however, the cap is smaller than it appears.

As of the first-quarter report, Mach held fixed-price swaps on roughly 2.5 million barrels of oil at $65.87 per barrel through the end of 2026. It also held a costless collar on another 459,000 barrels, with a $ 78.24-per-barrel ceiling. Those are real caps. But these positions run through the end of 2026, and the share of second-half barrels they cap shrinks with every month that settles. By the second half, roughly 60% of Mach’s oil is either unhedged or newly collared around current prices. Those barrels will likely realize a crude price in the $90s, not the $66 per barrel that the legacy swaps locked in.

So while the cap is not gone, it’s loosening, quarter by quarter. And how much stays unhedged is management’s call, not the market’s. The existing book covers about 38% of second-half oil, roughly their historical pace, so most barrels will realize the higher price. Holding the percent of hedged production flat, the upside will flow through. On the other hand, if management opts to hedge up defensively toward 80%, the quarterly distribution will be reduced by $0.05 to $0.06 per unit. The point for unitholders is that the hedge book plays a large role in the extent of Mach’s income increase, not in whether it increases.

Management Is Already Drilling for $95 per Barrel Oil

Mach is not waiting for higher prices to help. On the first-quarter call, management laid out a real-time pivot toward oil. Effective May 1, it moved a rig into the oil-bearing Agogo formation in Kingfisher County, where it has drilled more than 250 Oswego locations, and paused the deep Anadarko dry-gas program. The shift adds three oil-weighted rigs, with a possible fourth in the Permian Clearfork. Drilling economics are driving this decision. Oswego wells return 90% at $75 per barrel WTI and 145% at $85 per barrel, and management pegs the Clearfork at a 100% rate of return at today’s prices. Mach’s chief financial officer, Kevin White, added that the oil wells carry shorter cycle times than the deep gas program, so the shift should help this year’s cash generation rather than delay it. This is the rare pivot that costs nothing in additional capital, with management holding its reinvestment rate below 50% of operating cash flow while tilting the production mix toward the most profitable barrels.

Second-Half Cash Flow Rises Even Against the Hedge Cap

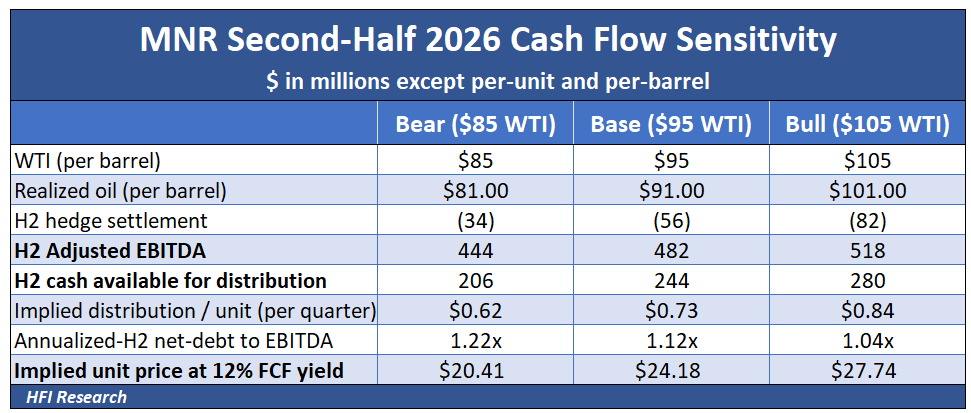

Looking at hedged and unhedged production, the surge in cash flow is significant. The table below shows the results of my model for Mach’s second-half distributable cash flow across three oil price scenarios. It maintains the oil-weighted production mix and the current hedge book, and adds the costless collars as prices rise.

In the base case at $95 per barrel WTI, roughly the level currently implied by observed global inventories, second-half cash available for distribution runs about $244 million, versus $107 million in the first quarter. That would lift the quarterly distribution from the $0.64 declared for the first quarter toward $0.73 per unit, a gain of nearly 14%, even after the model concedes about $56 million of hedge-settlement losses and a heavily gas-weighted volume base. The unhedged marginal barrel drives the variable distribution, and at $95 oil, more of those barrels arrive every quarter.

At the bear case of $85 per barrel WTI, the distribution roughly holds at the first-quarter level.

A meaningful cash flow ramp requires WTI to trade at or above $95 per barrel. While the drag from hedges upon cash flow is genuine, the bulk of the drag is attributable to the company’s legacy swaps at $65.87, which will roll off. This is therefore not a permanent ceiling, demonstrating that the cap mutes the increase in cash flow but does not erase it.

The cash flow generated in these scenarios also implies a value for the units. Annualize each scenario’s second-half distributable cash flow to a full-year run rate, about $412 million, $488 million, and $560 million, and capitalize it at a 12% free cash flow yield, which is in the ballpark of what the market tends to demand for a variable-payout E&P. On the 168.2 million units outstanding as of the first-quarter report, the implied unit price stands at roughly $20.41 in the bear case, $24.18 in the base case, and $27.74 in the bull case, 53%, 81%, and 108%, respectively, above the current unit price of $13.35.

Even the bear outcome puts the units well above our $12.69 April purchase price, while the base case represents nearly a double. These are sensitivities, not price targets, but they show what the second-half cash flow is worth once the market values it on yield rather than on a multiple of reported earnings.

Leverage Falls Without Touching the Distribution

Because Mach distributes nearly all of its residual cash, its leverage improvement will come less from debt retirement and more from EBITDA growth. My model shows annualized second-half net debt-to-EBITDA falling from about 1.22x at $85 per barrel WTI to about 1.04x at $105 per barrel. That brings the company close to management’s roughly 1.0x target, with no retained distribution.

So while net debt barely moves, EBITDA in the denominator of the leverage ratio increases with oil prices, causing the ratio to fall even as cash is distributed to unitholders rather than allocated to debt repayment. This is why management can credibly promise both a rising distribution and a falling leverage ratio. Management has been explicit that it will achieve its leverage target through EBITDA growth, not by cutting the payout. In fact, CEO Tom Ward likened the quarterly distribution to getting Christmas four times a year, implicitly rejecting the idea of trimming the payout to fund debt paydown.

What Would Break the Thesis

This analysis views Mach as a long oil position, so the primary risk relates to oil prices. A sustained move in West Texas Intermediate back below roughly $70 per barrel would reduce the cash flow benefit from unhedged barrels and push the distribution back toward first-quarter levels.

The second risk is execution. Pausing deep Anadarko gas while the oil rigs ramp could cut gas volumes faster than oil replaces them. If total output slips meaningfully below Mach’s roughly 158 Mboe/d production base, the cash-flow math could weaken.

Finally, management could allocate more residual cash to debt than to distributions, which would still be a win for the units but not for income. Unitholders should keep in mind that a variable distribution that ramps up also ramps down. None of these risks is hidden, and each is worth watching.

Conclusion

Mach offers one of the best risk/reward propositions among oil and gas E&Ps. Its variable distribution turns a rising crude price directly into rising income, and its cost structure defends against downside risk. Loosening hedges, an oil-weighted drilling pivot, and quick organic deleveraging all point to a higher payout and a lower leverage ratio from the same cash flow.

However, the call lives and dies with oil prices. If WTI reverses hard, the company’s distribution will give back much of the gain, and the hedge book will cap the top of any spike. I think that is the right risk to take here: a low-cost, long-life asset base bought below the value of its proved reserves, run by a team that treats the distribution as sacred.

We continue to own Mach in the HFIR Energy Income Portfolio and would add it at current prices. The April purchase at $12.69 looked like a deep value call on a misread secondary offering. Three months later, with WTI in the $90s, rigs already heading toward oil, and the stock trading only 5% higher, it is an undervalued current income call with capital appreciation, too.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of MNR either through stock ownership, options, or other derivatives.