By: Jon Costello

Mach Natural Resources LP (MNR) reported first-quarter 2026 results on May 7, the first clean look at the company’s performance since its IKAV and Sabinal acquisitions closed last September. I added units at $12.69 in early April after the non-dilutive secondary offering triggered a 10% selloff, and came into earnings seeking confirmation that the combined business is integrating on plan. The integration is on plan, and the value case I laid out in April still holds at the current $14 unit price.

Operations Pivoting To Oil

The most consequential development of the quarter wasn’t in the numbers. Rather, it was CEO Tom Ward’s decision to pivot the rig program back toward oil. Starting May 1, Mach moved its first rig into the Oswego in Kingfisher County, where the company has drilled more than 250 wells since 2021, and the 2025 program sported a 39% IRR at $57 WTI, rising to 87% with WTI at $75 and 145% with WTI at $85.

Mach also paused its Deep Anadarko dry gas program and is planning to add up to two more oil-weighted rigs. The company is weighing adding a Clearfork rig in the Permian in place of the San Juan Mancos completion program. Returns from Clearfork are around 100% at current oil prices.

With WTI in the $90s and Henry Hub hovering just under $3, the shift toward oil is the same oil vs. gas “toggle” that Ward described on Mach’s fourth-quarter earnings conference call, just running in reverse. The company can flip back to gas the moment gas prices offer better returns.

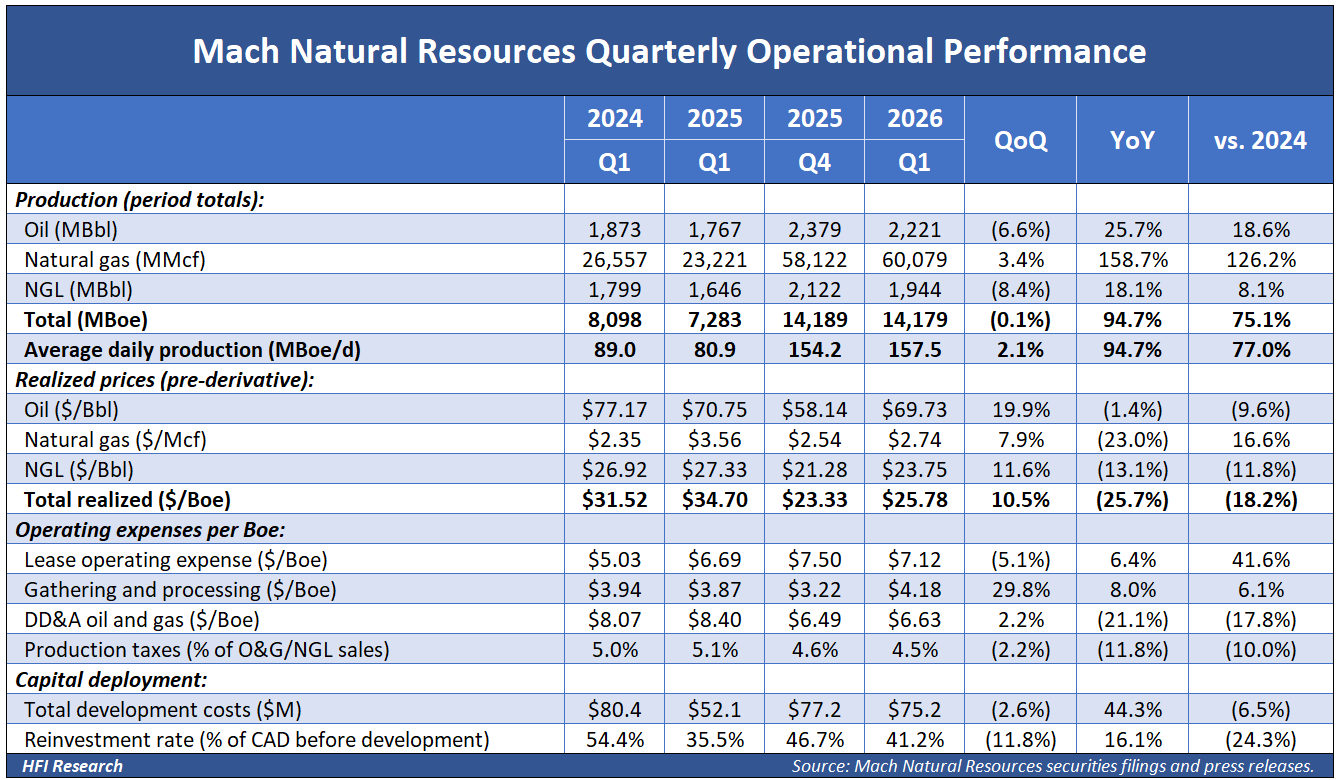

Production during the quarter averaged 157.5 MBoe/d, up 95% year-over-year. Essentially all of that gain came from the IKAV and Sabinal acquisitions, as organic production from the legacy Anadarko base was essentially flat. The company’s production mix is now 16% oil, 70% natural gas, and 14% NGLs. Importantly, unit costs are moving in the right direction: LOE per Boe came in at $7.12, down from $7.50 in the fourth quarter of 2025, a 5% sequential improvement that indicates the acquired assets are integrating on plan. The 2026 capex range of $315 to $360 million remains intact.

Meanwhile, the San Juan story is unchanged. Mach holds 570,000 net acres in the basin, the Mancos shale continues to perform at the high end of expectations, and 65% of basin volumes are committed under the BP take contract at $1.72 per Mcf through 2030. This contract is one of Mach’s most underappreciated assets, given where the uncontracted San Juan basis is currently transacting.

Robust Cash Generation

The first quarter was noisy in terms of GAAP but clean at the cash level. Revenue of $285.9 million was up 26% year-over-year but down 26% sequentially, and Mach reported a $35.0 million net loss versus $15.9 million of net income a year ago. The cause was a $96.9 million derivative loss, almost entirely an unrealized mark-to-market loss resulting from rebounding oil prices relative to the company’s hedges.

Strip out the derivative noise and the underlying business actually delivered. Adjusted EBITDA of $194.6 million was up 22% year-over-year and 4% sequentially. Cash available for distribution of $107.4 million was up 22% sequentially and 14% year-over-year. Mach declared a $0.64-per-unit distribution, up from $0.53 in the fourth quarter of 2025, consistent with the framework of paying out essentially all distributable cash after a sub-50% reinvestment rate. The first quarter’s reinvestment rate came in at 41%. The blended realized price was $25.78 per Boe pre-derivatives, down 26% year-over-year, dragged down by gas at $2.74 per Mcf.

On the balance sheet front, net debt was $1.082 billion at quarter-end, putting trailing leverage at roughly 1.3x Adjusted EBITDA against Ward’s 1.0x target. That gap is a binding constraint on capital allocation. Ward called the leverage “a pebble in my shoe” on the call and made clear that M&A will be on hold absent an all-equity deal that is accretive to distributable cash. He also confirmed he won’t cut the distribution to pay down debt. Rather, leverage will normalize as commodity prices recover, driven by EBITDA growth. With $358 million of liquidity, Mach has the room to keep paying out at current prices and wait for gas to firm.

Value in Excess of the Unit Price

At Mach’s current unit price of $14, the value on offer to equity investors is ample. The company’s enterprise value stands at approximately $3.4 billion, comprised of roughly $2.3 billion in market cap and $1.1 billion in net debt. At year-end 2025, Mach reported total proved reserves of 705 million barrels of oil equivalent, representing a 109% year-over-year increase, with a PV-10 value of $3.1 billion under an average WTI price of $65.34 per barrel and an average natural gas price of $3.39 per MMBtu.

Today, WTI trades at $98 per barrel and Henry Hub natural gas at $2.90 per MMBtu. The reported PV-10 was calculated using SEC pricing of $65.34 WTI and $3.39 per MMBtu Henry Hub — well below today’s $98 WTI and $2.90 Henry Hub. Even under those conservative price assumptions, PV-10 covers more than 90% of the enterprise value. Recalculated at current commodity prices, the reserve value comfortably exceeds the entire enterprise value, implying the market assigns essentially zero value to owned midstream infrastructure, future development upside, and continued growth through future accretive acquisitions.

Using Mach’s first-quarter 2026 realized price strip of roughly $72 per barrel WTI, the company generates approximately $0.60 per unit per quarter, or $2.40 annually in distributions, resulting in a 17.1% distribution yield at the current $14 unit price. First-quarter 2026’s actual declared distribution of $0.64 sits modestly above that model output, with the gap attributable to NGL realization and minor mix effects. The following table illustrates my estimates for the company’s cash flow sensitivity at different commodity prices.

The company’s earning power is more robust if commodity prices remain elevated and it locks in higher prices through its programmatic hedging. Without hedges, it could generate approximately $2.85 per unit, representing a 20.4% distribution yield.

These estimates assume a first-quarter WTI price of $72 per barrel, a production mix of 55% Mid-Continent, 38% San Juan, and 7% Permian Central Platform, and that NGLs are priced at 35% of WTI.

Mach’s investors will fare very well from an income perspective, and as the company pivots toward oil—and if the structurally higher oil prices we expect become consensus—then it is only a matter of time before the unit price increases to compress the distribution yield to between 8% and 12%.

Risks to the Investment Thesis

Downside risk to unitholders stems from lower commodity prices, higher capex, and higher cash interest on the company’s credit facility. Additionally, Mach’s edge has always been buying assets at or below the value of their currently producing reserves, but that supply of distressed deals tightens as commodity prices rise.

Another potentially material downside risk stems from San Juan’s uncontracted prices. The 35% of Mach’s San Juan gas production that isn’t locked into its contract with BP sells at whatever price the local market will pay, and that local price is currently around $1.00 per Mcf, well below the national Henry Hub benchmark, because there isn’t enough pipeline capacity to move San Juan gas to higher-priced markets in the Pacific Northwest, Phoenix, or Mexico. Mach’s outlook assumes new pipelines and LNG terminals open up over the next few years to absorb that gas. If those projects get delayed, then the local San Juan price could fall even further below $1.00, dragging down Mach’s blended gas realization regardless of what Henry Hub prices do.

On the financial side, leverage above target constrains the company’s capital allocation. Its borrowing base is reset twice a year based on commodity-price assumptions. Its revolver carries variable interest rates, and the open hedges will remain a drag on cash flow until the swaps roll off.

Conclusion

The first quarter didn’t change our investment thesis for Mach. The company’s PV-10 still covers nearly the entire enterprise value at SEC pricing, and would more than cover it at current commodity prices. The 25% multiple discount to C-corp peers remains, and the variable distribution still delivers oil-price strength directly to unitholders. At a mid-teens yield backed by sub-$40 WTI breakeven economics, I’m holding and plan to add to the position if the units dip back toward my $12.69 cost basis.

Link to HFIR Energy Income Portfolio on RunPlutus.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of MNR either through stock ownership, options, or other derivatives.