By: Wilson

Wow, this is incredible.

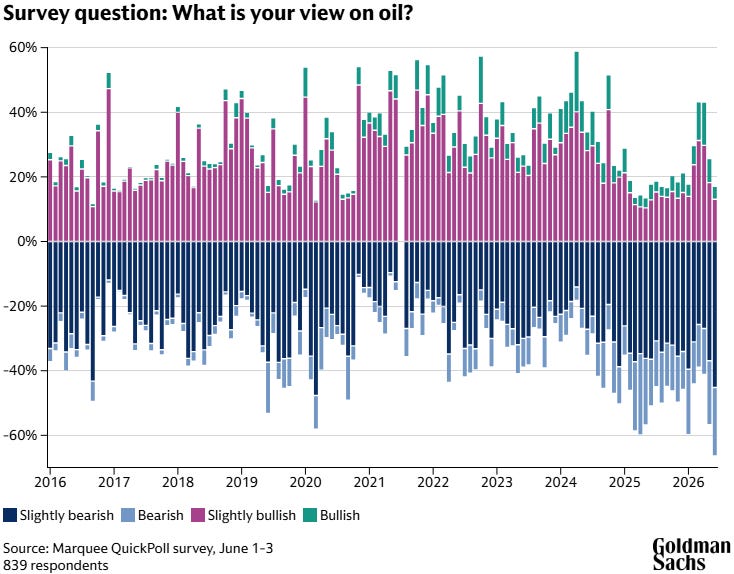

Goldman conducted a survey that showed 839 respondents were overwhelmingly bearish on oil.

That’s incredible. I have traded oil since 2019 and followed the oil market closely since 2015. So it’s ironic that I can tell you precisely at each major point in the oil market over the past decade how accurate this survey is.

Hint, these guys are contrarian indicators.

End of 2016: OPEC+’s first production cut since the start of the oil price war (late 2014).

The survey was very bullish on oil. The OPEC+ production cut wasn’t implemented to its full effect. OPEC+, as usual, kept producing the same barrels until Saudi Arabia’s energy minister (at the time), Khalid Al-Falih, threw down the gauntlet in mid-2017 and targeted US commercial crude oil inventories.

Middle of 2018: Iranian oil sanctions.

Of course, who can forget my favorite moment in my career so far: Iranian oil sanctions. In March 2018, the Saudis’ efforts to target US commercial crude oil inventories began to pay off. Couple that with Trump talking about leaving the JCPOA and sanctioning Iranian oil exports, and oil prices entered an uptrend.

Survey participants were more bullish in mid-2018 than they are today, despite Iranian oil sanctions impacting only ~1.5 million b/d, whereas we are losing ~11 million b/d today.

This is stupidity at its finest.

March 2020: COVID.

As the saying goes, price changes the narrative; market participants were overwhelmingly bearish on oil after the COVID lockdowns, when the opposite should’ve been true. I vividly remember that in March 2020, I was the only one who talked about how forced production shut-in would balance the global oil market. It wasn’t until a month later that the consensus came to that view. At the time, if you were brave enough, you could have bought companies like Suncor for below PDP value (proved developed producing, aka, equivalent to net-net of value investing).

2022: Ukraine/Russia.

Last but not least, who can forget Russia’s invasion of Ukraine. In March 2022, the IEA wrote that Russia would lose ~3 million b/d of crude oil production. Oops, Russia didn’t lose anything, and crude exports surged contrary to expectations.

Instead, the IEA convinced everyone that production losses were imminent and coordinated a global SPR release over ~260 million bbls.

OPEC+ also began unwinding its production cuts, and the Biden administration turned a blind eye to Iranian crude exports.

But, of course, these survey participants remained bullish on oil prices throughout this period despite no visible supply loss.

What’s the takeaway here?

Do the opposite.

Whoever Goldman is surveying is so clueless as to the point of blissful ignorance.

As Sun Tzu (or Don Tzu) said, “Never interrupt your enemy when he is making a mistake.”

For anyone bullish on oil, this survey is the greatest blessing. You should print this chart out, frame it, and your future generation should thank these 839 respondents for it.

If you are one of those respondents and you are reading this article, thank you. Thank you for being so oblivious. If you don’t understand the oil math, don’t; I don’t want you to.

In the meantime, let the fastest visible onshore oil inventory declines continue. If an outright shortage is what’s needed to wake market participants up, then so be it.

We are going full speed into the wall and there’s no reversing this now.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of SU, USO, UCO, BNO either through stock ownership, options, or other derivatives.

I posted this on a previous post. I feel like Casandra. You?

Anas Alhajji has the opposing view. He claims that demand decline is offsetting the supply decline and he is bearish on oil. Alhajji is generally respected, is my impression, at least. Can you comment on why you think he is mistaken in his analysis? I think that Alexander Stahel also attributes the demand decline to China?