(Public) My Latest Thoughts On The Oil Market Amidst The Incredible Jawboning On The Iran Conflict

They threw everything at the oil market in the past week.

SPR release (hedging by the companies that received allocation).

Bank of Japan intervention through the FX market.

Axios fake headlines.

Pakistani sources saying a framework is close.

I understand the frustration many of you are facing. I get it. The P&L swings have been extreme, but the math is what it is. Some people in the oil community have started to question their own sanity with questions like:

Why aren’t physical premiums for crude higher?

Why is China’s onshore satellite crude storage data showing a build?

Is 5 million b/d of demand destruction already here?

It’s easy to get myopic right now. The math is hard to fathom so it’s easy to start thinking about all the things that can screw with your trade (long oil, I’m assuming here).

I hope I can provide you with some clarity. Here are the topics I want to discuss today:

Difficulties in conviction.

The differences between what the US wants and what Iran wants.

Oil market math.

Difficulties In Conviction

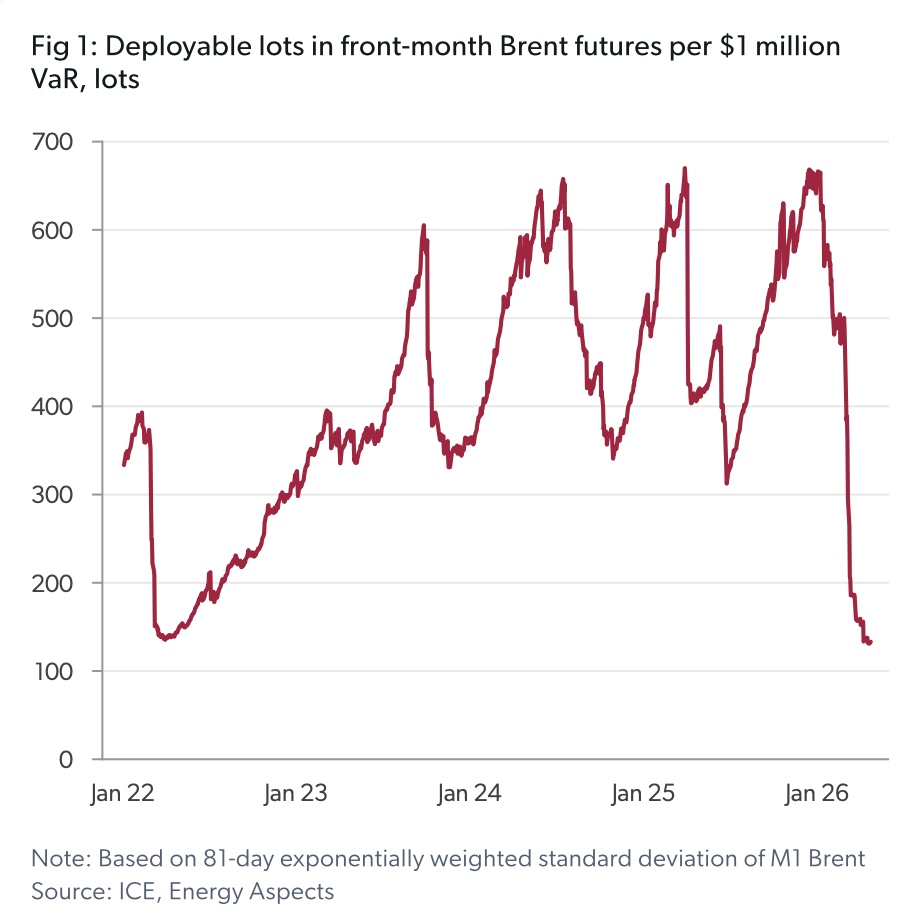

Fog of war and the Trump Administration have used mainstream media outlets to deploy this weapon. The constant headline risk is preventing oil traders from taking any conviction bets. Energy Aspects recently wrote a piece noting that value-at-risk (VAR) constraints have made it very difficult to take on positions.

I have seen sell-side analysts attribute the current refinery outage of ~5 to ~6 million b/d to demand loss without acknowledging that, even during the Great Financial Crisis of 2008-2009, global oil demand fell only ~3%.

Even energy specialists are trying to be “conservative” because the models that they are running show us running out of commercially available oil inventories by this summer. I mean, it can’t be that bad, right?

The issue, again, is that we’ve never had a supply outage of ~12 million b/d.

Never.

There’s no supply & demand model that even remotely gets close to the level of inventory draws that we are going to see ahead. Oil traders themselves continue to hope for a swift resolution so all of the floating storage in the Persian Gulf is unlocked. Everyone is spending most of their time figuring out what the oil market would look like if the Strait of Hormuz were reopened, without analyzing what it would look like if it weren’t.

That’s the situation we are in now. Even the guys who live and breathe this stuff are having a hard time wrapping their heads around the magnitude, so I can’t imagine what generalists are thinking with both the S&P 500 and Nasdaq ripping right in front of our faces with every fake Axios headline.

It is what it is.

It is difficult to take on a conviction position today. The market is making it hard, but this is precisely when you need to be clearheaded.

The Differences

It is clear to me that Iran either wants uranium enrichment or control of the Strait of Hormuz. It is willing to part with 1, but not both.

The US wants Iran to part with both in exchange for relief from economic sanctions and compensation payments.

Money is not the issue here. Deterrent is. Iran needs guarantees that there will be no more attacks from Israel, and the only way to guarantee that is if it has either 1 or both of those things (Strait of Hormuz control/enriched uranium).

And here lies the big issue, from an oil market standpoint, Iran cannot control the Strait of Hormuz. If it controls it through a toll mechanism, then it will have an effective say in oil production in Saudi, UAE, Iraq, Bahrain, Kuwait, and Qatar. It will control 11% of global oil supplies (including all bypasses, Saudi’s East-to-West, and the UAE’s Abu Dhabi pipeline) and 20% of LNG flows. The GCC would never agree to any supply restrictions, so continued conflicts are a guaranteed scenario.

On the other hand, if Iran gives up control of the Strait, then it will want to pursue a nuclear bomb. Again, this is a nonstarter for the Trump administration.

No matter how you slice and dice this, the outcome is inevitable. Either we escalate further or Iran gets exactly what they want through the economic pain they are inflicting.

As my friend PauloMacro said before, follow the North Star. Clarity of thought is hard to come by when you have so much crap thrown at you on a daily basis. But the logic is what it is.

Oil Market Math

One of the most interesting arguments I have seen from very smart oil traders is 1) they are confused by the weak physical premiums, and 2) the data out of China.

Let’s talk about China first.

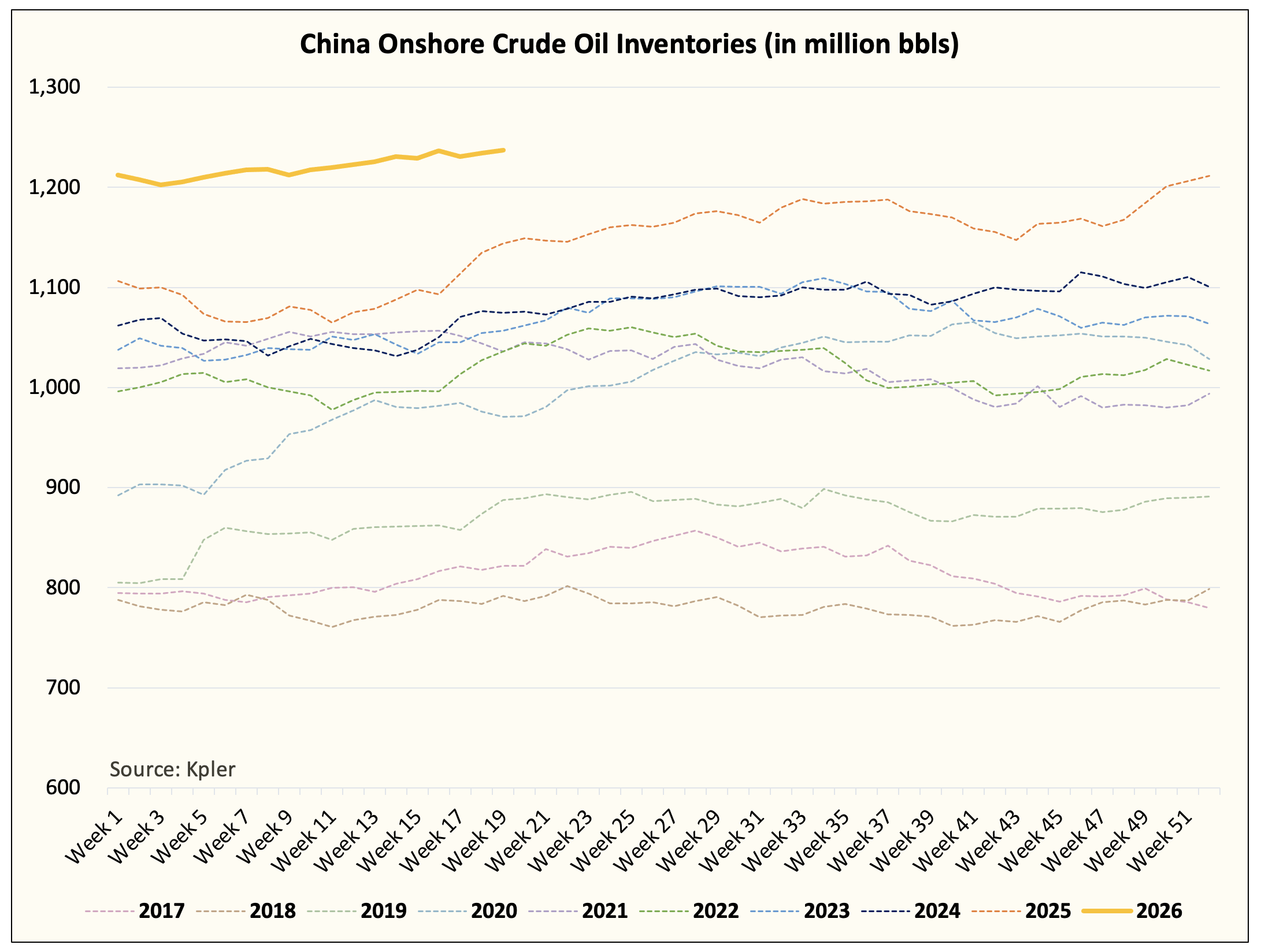

Here are China’s onshore crude oil inventories. And before we go any further, you need to understand how the sausage is made.

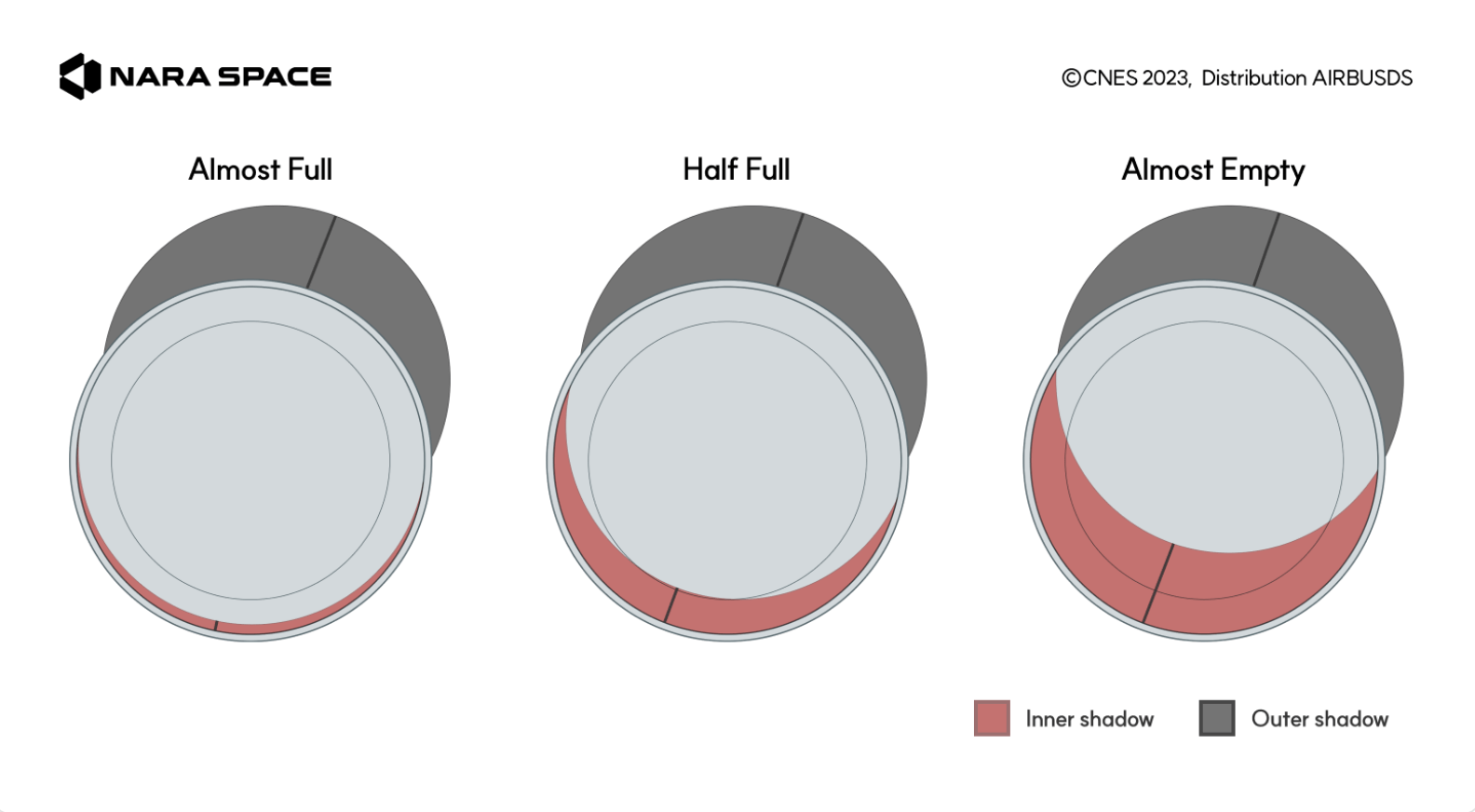

China does not disclose its oil inventories. It’s a black box. Smart service providers like Kayrros and Kpler figured out about 10 years ago that using satellite imagery to observe the shadow of a floating roof storage tank could help determine how much oil is left in inventories.

Source: Naraspace

This is how China’s onshore crude oil inventories are derived. The satellites revisit the location, snap an image, and a computer program deciphers how much the storage tanks have moved. It’s imperfect, as the images could be blurry, but it gives a rough approximation of where storage is at.

One question many physical oil traders have had over the past week is: “Why aren’t China’s onshore crude oil inventories declining?”

Well...

We know that China has underground crude oil inventories.

We know China had a lot of sanctioned crude flooding in (Russia and Iran).

We know China banned petroleum product exports (recently restarted, but it’s a rounding error, 116k b/d).

We know China saw a ~2.9 million b/d year-over-year decrease in seaborne crude imports in April.

Based on China’s economic data, there’s no scenario where oil demand fell by more than 2.9 million b/d. Anecdotal data from my discussions with people on the ground points to the same conclusion. As a result, there are only two reasonable conclusions we can arrive at:

China is releasing crude oil inventories in underground storage, knowing full well that the rest of the world is watching its onshore inventories.

Refineries in China have throttled back throughput, but product inventories are drawing (unobservable).

My assumption here is that a bit of both. At the end of the day, the 12 million b/d of production shut-in is a known fact. China’s oil inventory data is not. Given that we know one of them with certainty, then it’s the uncertain variable we have to question, not the known one.

But during times of chaos, we can lose our minds, so I get it; traders are starting to question their own sanity.

I’m here to tell you that you are not. The math is what it is.

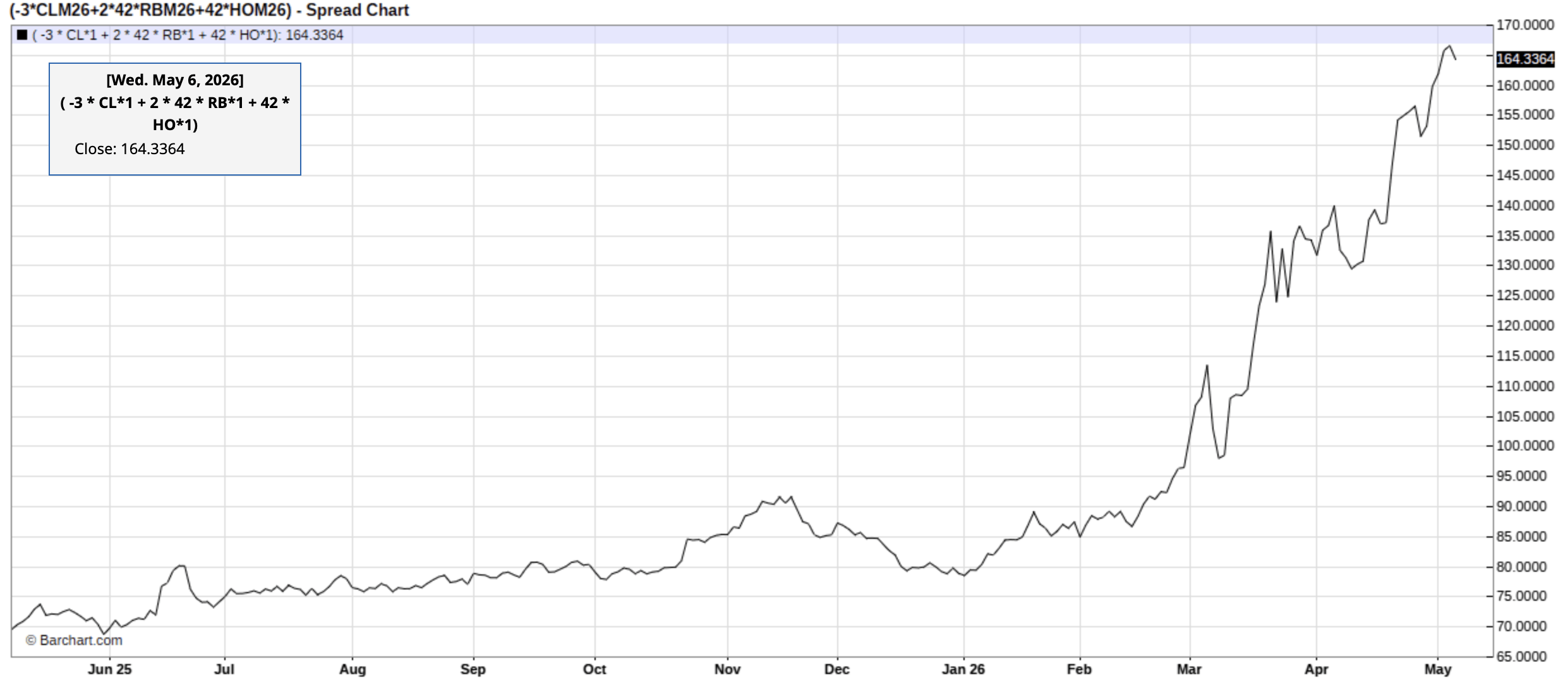

Now, if we look at the current physical oil market landscape, one thing is for certain: refineries are getting the most benefit if they have access to crude.

Despite crude’s sell-off today, the 3-2-1 crack spread remains near all-time highs.

Note: Divide it by 3.

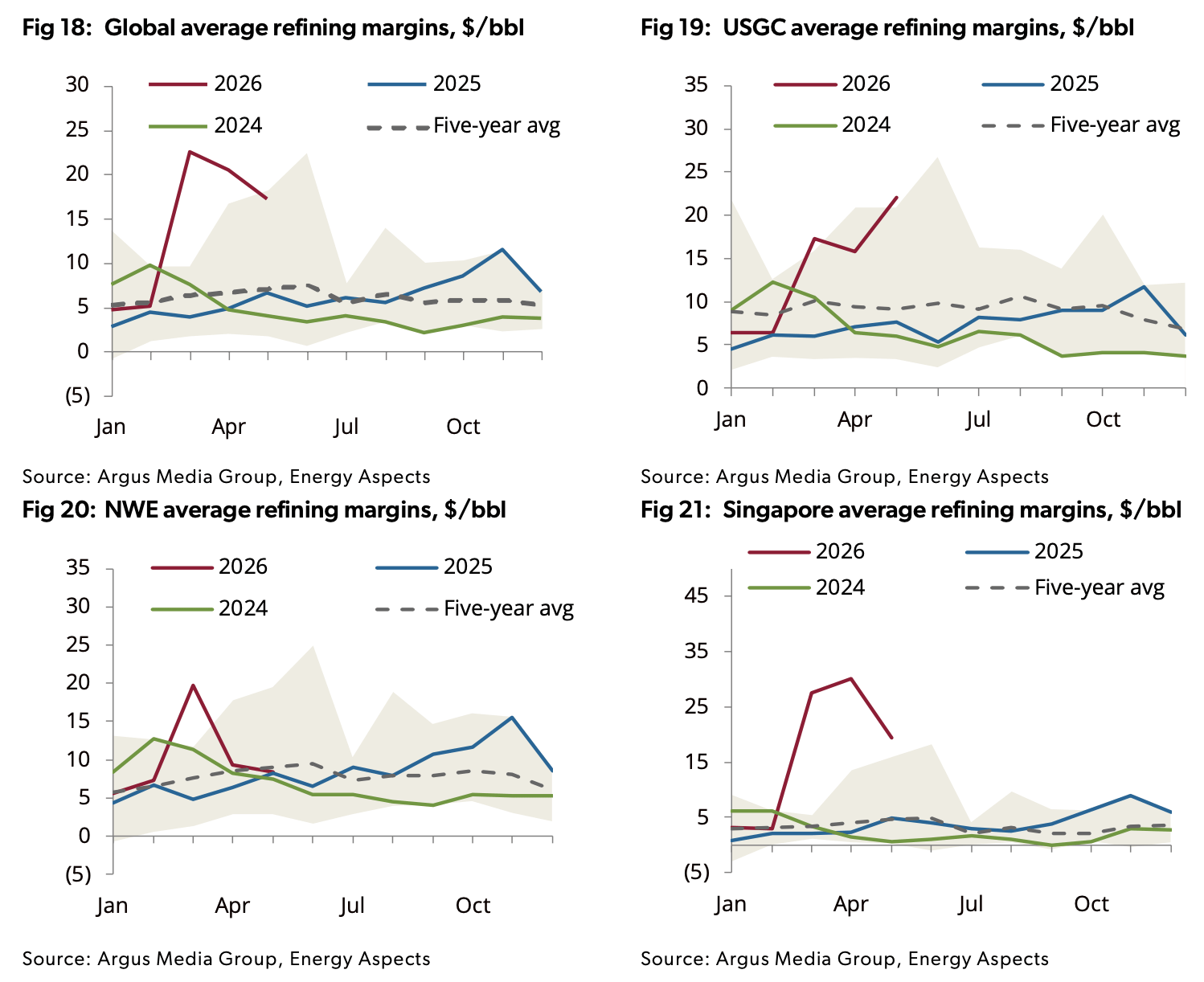

Energy Aspect’s refining margin proxy shows margins above seasonal norms globally, except in Europe.

So yes, refineries are disproportionately benefiting today, but the Strait of Hormuz outage is predominantly crude. It is only a matter of time before product storage runs low, refinery throughput ramps up, and crude storage plummets. The sequencing is what it is; it’s an inevitable outcome.

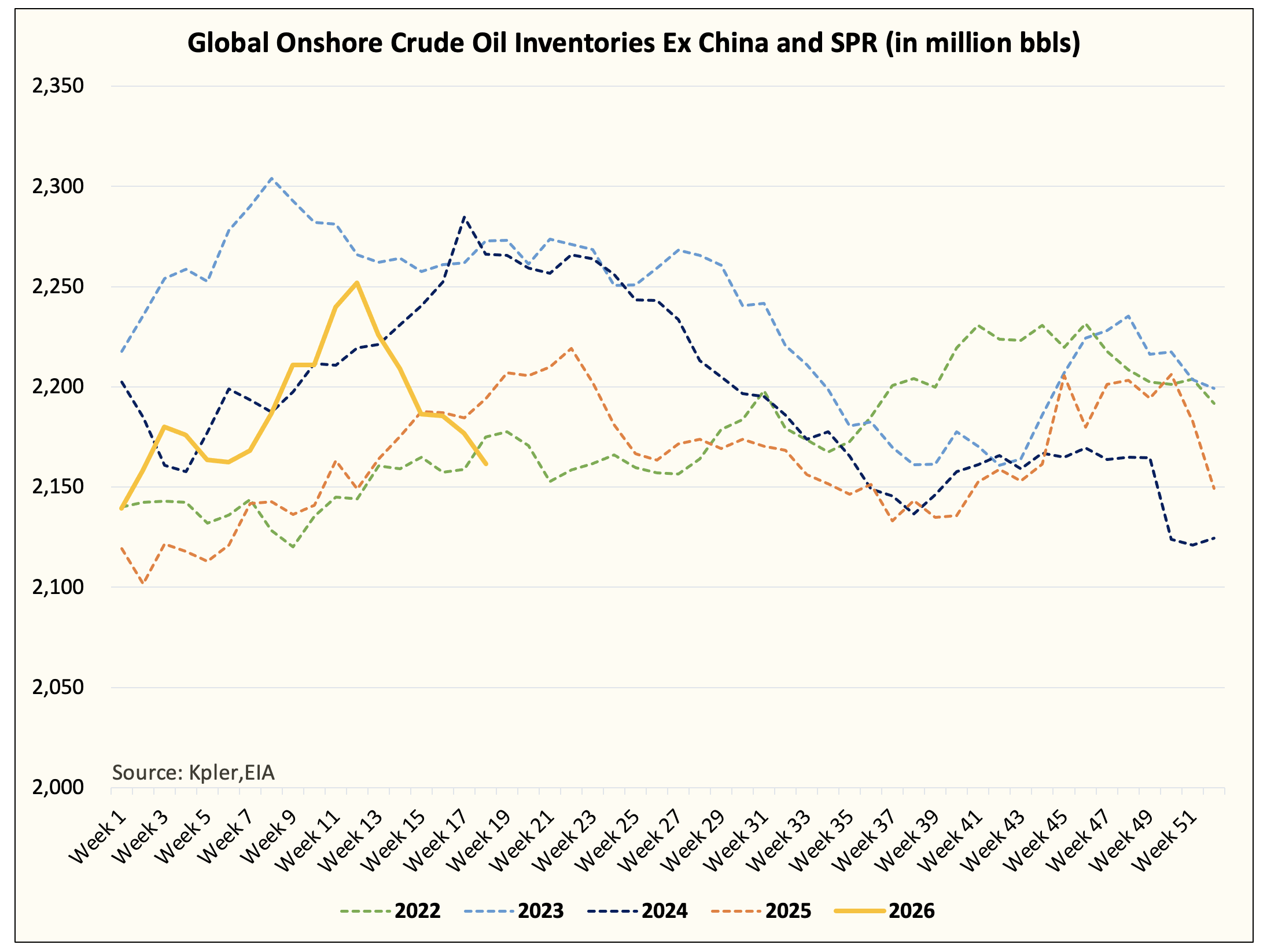

Visible Oil Inventories

Global onshore oil inventories, excluding China and the SPR, are headed straight down. The only scenario that would prevent oil inventories from plummeting is if all the governments around the world implement a global lockdown right now and kill oil demand by ~20 million b/d.

Outside of that, there’s not one scenario that will prevent this cliff in visible onshore oil inventories.

Not one.

The math is what it is. Visible onshore oil inventories are about to plummet so fast that oil analysts won’t even know how to reconcile the numbers. I’ve done the math, and I can’t believe the draws we are about to see.

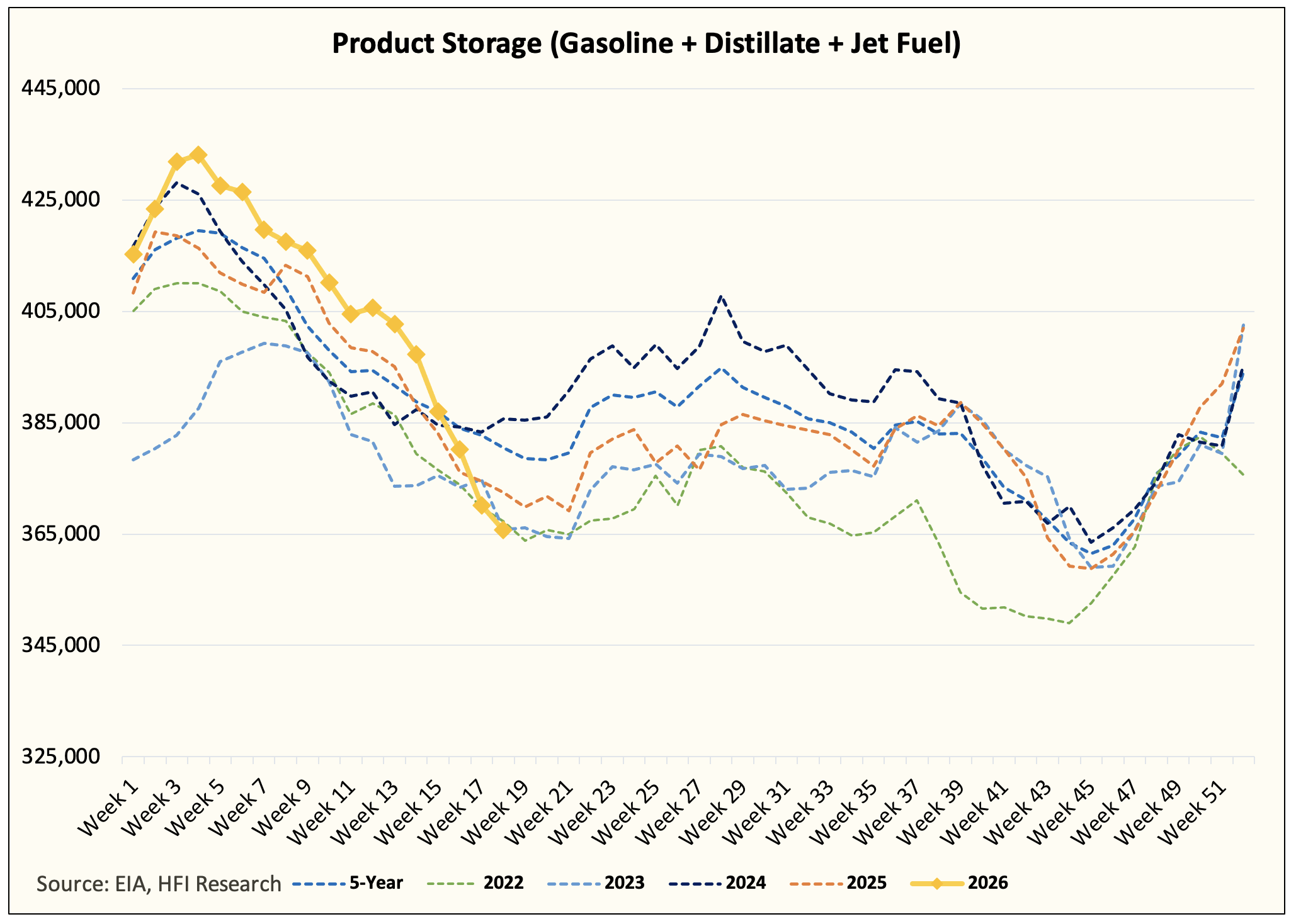

The big 3 product storage in the US, gasoline, distillate, and jet fuel, are already on pace to fall to the lowest level for this time of the year.

Record petroleum product exports are going to continue, and crude storage is now the only place with any buffers left.

Again, even if the Strait of Hormuz opens this very second, those visible draws are coming. No headline from Axios will change this outcome.

Conclusion

The math is correct. The outage is real. I am putting my money where my mouth is, and today’s headline changed nothing.

There’s really nothing more to say about this other than the conviction I’ve displayed in my writing over the past month.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of USO, UCO, BNO Calls, USO Calls either through stock ownership, options, or other derivatives.

Thanks for the article and the resolute consistency. Could you elaborate on why the physical premium is so muted given market participants must also see what's coming?

🙏