Editor’s Note: Jon Costello is the head of Ideas from HFI Research, a separate subscription service to HFI Research. If you have not signed up as a free subscriber yet, I highly recommend you do so!

By: Jon Costello

Incoming data continue to indicate that U.S. shale oil production is maturing. Fourth-quarter production results for U.S. independent E&Ps show shale production growing gassier. This phenomenon is becoming more pronounced over time and is occurring in most shale basins.

The large independent Permian operators—all of which prioritize crude oil over natural gas in their production mix—all saw their crude production decrease relative to their natural gas and NGL production on a year-over-year basis. These E&Ps may have expanded their production through acquisitions between the fourth quarters of 2023 and 2024, but despite their larger size, all saw their production grow gassier.

Diamondback Energy (FANG) is considered to be one of the best-managed U.S. independent E&Ps, with some of the best acreage in the Permian. Diamondback’s fourth-quarter oil production fell from 59.0% of the company’s total production to 53.9% on a year-over-year barrel of oil equivalent basis. The company’s natural gas production increased from 19.8% to 22.0% of total production, and its NGLs increased from 21.2% to 24.1% over the same timeframe. Fourth quarter results are shown below.

Diamondback’s notably gassier production was in large part attributable to its acquisition of Double Eagle last year. In early 2024, Double Eagle’s production was reported to be comprised of 69% liquids versus Diamondback’s 80% at the time. It remains to be seen if the legacy Double Eagle acreage—which was substantially undeveloped—can become more oily over time, but results to date aren’t encouraging.

Diamondback’s higher gas-to-oil ratio had a negative impact on its financial results, albeit a small one. In August of last year, the company decided to curtail some of its Permian oil production in order to limit its natural gas output amid a natural gas supply glut and local takeaway constraints. While the move made sense, it speaks to the risks to shareholders when basin-wide gasification occurs.

Permian Resources (PR) also experienced a higher gas-to-oil ratio in the fourth quarter. Year over year, its crude oil production fell from 47.9% to 46.5%.

Permian Resources’ acquisition of Delaware Basin acreage from Occidental Petroleum (OXY) didn’t prevent its oil weighting from falling.

Turning to the Bakken—historically the most oil-weighted of the U.S. basins—large producers in the basin also saw their oil weighting fall. Hess Corp.’s (HES) oil weighting fell from 45.9% to 44.8% year-over-year during the quarter. Its natural gas weighting increased, and its NGL weighting remained flat, as shown below.

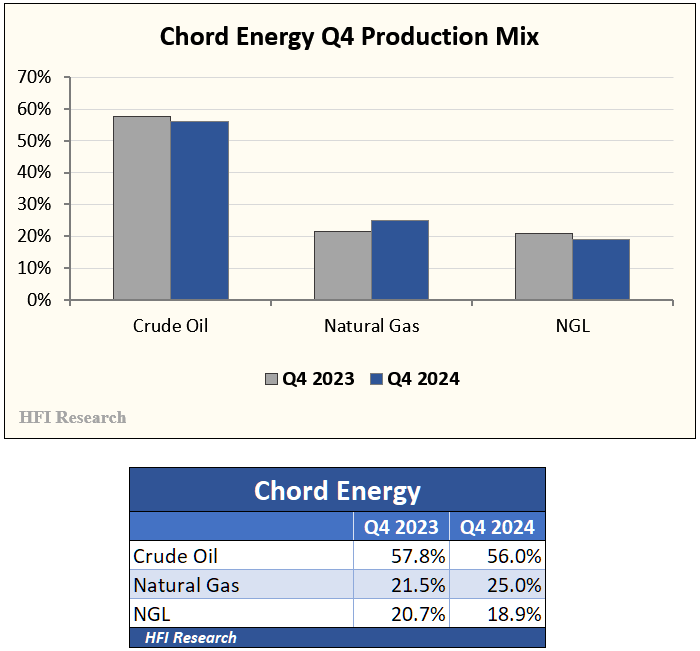

The same is true for Chord Energy (CHRD), which experienced a steeper falloff in its oil weighting than Hess. Chord’s 2024 acquisition of Enerplus failed to bolster its oil weighting—another example where increasing size came at the expense of oil weighting.

Civitas Resources (CIVI), which has 356,800 net acres in the DJ Basin and 120,400 acres in the Permian, also saw its oil weighting decline. However, Civitas managed to buck the trend toward gassier production. It was the only large independent E&P to see its natural gas production remain flat instead of increasing. Its NGL weighting did increase, however.

Civitas’ results in the fourth quarter of 2023 include only a partial contribution from its Permian assets, which it acquired in an acquisition that closed in November of that year. Nevertheless, its oil weighting declined year-over-year in the fourth quarter despite the additional volumes.

Interestingly, Civitas’ DJ Basin production became more oily year-over-year during the fourth quarter. Its oil weighting increased from 46.2% to 47.7%. However, the company’s newly-added Permian production more than offset these gains to make its total oil weighting decrease. Civitas’ Permian oil production declined from 48.9% oil to 45.5% over the same timeframe. Its DJ Basin natural gas volumes held steady, while its NGL volumes in the basin decreased. Increasingly gassy Permian production could make Civitas’ $2.1 billion acquisition of Permian-based Vencer Energy from Vitol look foolish in hindsight.

Consequences to Oil Macro and E&Ps

The consequences of the gasification of U.S. shale production are significant for the global oil market.

One important macro consequence is that U.S. crude oil production will be increasingly challenged to remain flat. Since 2010, U.S. shale production has accounted for nearly all production growth outside of OPEC+. An increasing gas cut in total U.S. production will put well productivity at risk of declining. Lower well productivity in the U.S. will ultimately cause the marginal cost of global supply to increase. Moreover, the marginal production required to satisfy growing global demand will have to come from somewhere else, but no other region is capable of producing the volumes necessary to meet the demand growth we expect over the next several years.

On an individual company level, the higher gas-to-oil ratio and lower well productivity will negatively impact E&P capital efficiency, free cash flow generation, and returns on capital. It also increases the risk that company reserves will be subject to write-downs if crude oil remains significantly more valuable on a barrel-of-oil equivalent basis than natural gas.

The impact on individual companies could be positive or negative depending on the course of commodity prices. If the ultra-bull natural gas scenario plays out and natural gas egress remains sufficient, the growing natural gas weighting would likely be a net benefit for E&Ps and their shareholders. Sustained higher natural gas prices in this scenario would be a boon to gassier E&Ps, in particular.

The gasification of U.S. shale and the risks it implies for E&Ps strengthens the case for investors who seek crude oil exposure to avoid U.S. E&Ps and favor Canadian producers. Many Canadian E&Ps have greater inventory depth and a lower gas-to-oil ratio than independent U.S. E&Ps. Investors looking to hold for several years are therefore less likely to encounter declining well productivity and more likely to benefit from oil-weighted production growth over their holding period.

An additional benefit is that Canadian E&Ps currently trade at lower multiples than U.S. E&Ps. The respective multiples can flip to penalize U.S. E&Ps and benefit Canadian E&Ps if investors grow more wary about declining oil weighting. Furthermore, Canadian E&Ps are on sale due to near-term concerns over the potential impact of U.S. tariffs on their cash flows. We don’t expect the U.S. to make the irrational move of subjecting Canadian oil and gas to tariffs. If it does, we would expect the move to be short-lived as it pushes U.S. gasoline prices higher. We reiterate our view that investors with a time horizon of more than one year should consider buying Canadian E&Ps now.

Conclusion

The data continue to show the maturation of U.S. shale oil production. An increasing gas-to-oil ratio will only hasten the resource’s maturity, strengthening the macro case for investing in oil-weighted E&P stocks. At the same time, investors must be attentive to the risks of holding U.S. E&Ps for the long term. Given the greater upside we see over the long term, buying Canadian E&Ps and holding them for two to five years strikes us as a no-brainer.

Analyst's Disclosure: Jon Costello has no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours.

Instead of just "maturing," this article could have emphasized that gassy bloat is a Peak Oil precursor, since Peak Permian is essentially a global peak, which could trigger a worldwide depression in connected nations.

Man has experimented with energy for thousands of years and never quite hit the wall of no viable replacements, e.g. whale oil with petroleum. It's always been assumed the next big thing would take over, but most people ignore the vast difference in scale between sprawling "renewables" and fossil fuels that build & back up the former.

Even nuclear fusion can't replace many fossil fuel functions, given that electricity is only about 1/5th of total energy use. I'd worry more about economic collapse than picking this or that investment!