(Public) What To Make Of The Current Geopolitical Situation (Israel) And What It Means For Oil?

Note: This article was first published to subscribers on Sunday, October 8th.

First and foremost, the situation in both Israel and Gaza is horrible beyond our wildest imagination. This article is not about politics, and it will not focus on what's right or wrong. Instead, we will do our best to think through what this means for oil market supply and demand, and how readers can use it to manage their portfolio/trading positions.

Geopolitical Risk Premium

WTI and Brent, as of this writing, are up ~3% with WTI trading above $85 and Brent above $87. Initially, at the close of Friday, WSJ published a report noting that the US is close to finalizing a megadeal between Saudi and Israel. It even contained a quote stating that the Saudis may increase production by early 2024 if prices are too high. Soon after, Hamas militants launched a surprise attack on Israel. If you want to thoroughly review the events, please read this article.

Some of you may wonder, what does this have to do with oil? Historically speaking, geopolitical risk premiums are usually embedded into the price of oil in case of supply disruptions. In this case, Israel is not a major oil producer, so what's the catch? The catch, in our view, has to do with Iran's potential involvement in this whole ordeal. WSJ published a piece noting that Iran's senior officials helped plan this attack months ago.

While the US has not condemned Iran or associated Iran in any way with these attacks just yet, it does make you wonder what this means in terms of oil sanctions on Iran.

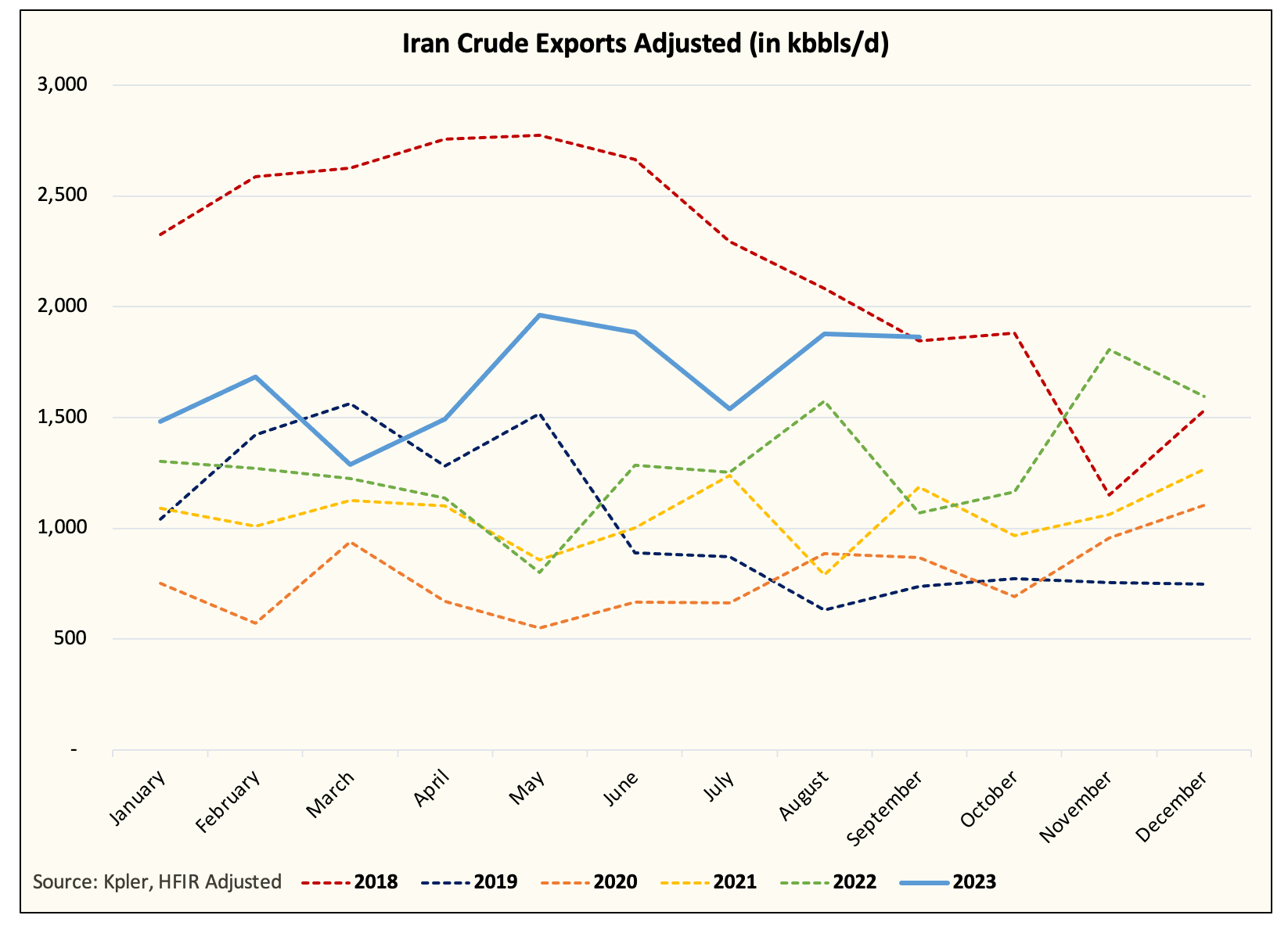

Source: IEA

For starters, we need context to what we are writing. In June, we published a report noting that Iran is already back in the oil market. Since then, IEA has confirmed via its figures that Iran's oil production is close to ~3.1 million b/d. Our supply & demand model assumes ~3.3 million b/d, and official Iranian figures support that production is around ~3.3 million b/d.

Putting all of this together, Iran is exporting close to ~2 million b/d. Visible tanker exports account for ~1.5 to ~1.6 million b/d, while shadow exports account for ~400k b/d.

Since H2 2022, the Biden administration has turned a blind eye to Iranian crude exports. As we wrote earlier in the year, this was most notable in the rapid decline in Iranian floating storage.

With floating storage gone and crude exports back to ~2 million b/d (~500 to ~800k b/d below the previous peak), what's the chance that Iranian crude exports drop going forward? Perhaps the US does nothing and leaves Iran as is, but what probability would we assign to that?

In my view, while the risk of a major loss is low, we think Iranian crude exports would move lower in the following months. We think the average would fall from ~2 million b/d to ~1.6 million b/d. In terms of visible tankers, this means Iran's crude exports would drop closer to ~1.2 million b/d.

While it won't be much of a decline, it will be compounded by the fact that Saudi and Russia will continue with their voluntary cuts into year-end and possibly well into H1 2024.

Supply & Demand Math

Looking at our latest supply & demand update, we made a few important assumption changes:

We have revised lower Iran's crude production from ~3.3 million b/d to ~3 million b/d.

We have made the assumption that Saudi/Russia will extend their voluntary production cut into Q1 2024 with a gradual pick-up in Q2 2024.

We have increased US oil production to ~13 million b/d up from ~12.75 million b/d for Q4.

We have made no demand changes. Reminder, we already have one of the lower demand assumptions out there.

In essence, global oil inventory draws should continue and accelerate once global refinery maintenance season finishes by month-end. And if the US starts to enforce some of the sanctions on Iranian crude exports, then our balance could surprise to the upside. But with a deficit of ~2.2 million b/d, the lack of production decline from Iran won't make that much of a difference either.

On the other hand, with no mega deal on the horizon (between Israel and Saudi), the possibility of a production increase from the Saudis also decreases. Pierre Andurand has also argued in his latest tweet that the Saudis won't be interested in increasing production until Brent is at least $110/bbl. With Brent trading at $87, we will have to wait a bit before that becomes a reality.

What does this mean for oil?

Israel and Saudi megadeal are off the table. The probability of Saudi increasing oil production in response to the deal decreases greatly.

The probability that the US will enforce sanctions on Iranian crude exports increases. This results in the potential for lower supplies from Iran.

With US crude storage remaining tight, US crude exports will fall into year-end.

Saudi and Russia voluntary cuts will continue and if Q1 2024 shows builds, then the cuts will be prolonged.

In conclusion, global oil inventories will accelerate downward. But the physical market will keep fighting the mainstream worries over an incoming recession. Fund flows will ebb and flow so oil prices won't skyrocket anytime soon. Only an extremely tight physical oil market could change perception. Until then, we see prices grinding higher with frequent retracements to solidify technical support levels.

For readers looking to add energy stocks, Q4 will provide ample opportunities. We see energy stocks lagging the broad move higher in oil. Consolidation and M&A are heating up, so you will see more and more mergers announced. But more importantly, always remember that with these oil prices, the energy companies you own are generating free cash flow hand over fist. Please be patient, fundamentals are on your side.