Elevated OPEC+ spare capacity, peak Chinese oil demand, extreme supply surplus in 2025, OPEC+ disunity, and whatever else people are saying to themselves to believe oil prices will crash lower, I've heard it all this year.

In particular, one of the best arguments I've seen pertains to the material growth we are going to see in US oil production.

Spoiler alert: It's not happening.

On August 9, we published our report titled, "US Oil Production Slowdown Is Real." We said:

Why this matters...

One of our key variant perceptions coming into 2024 was that people overestimated the production growth we saw from shale in 2023. The main culprit for this is from EIA's production reporting change. Following the June 2023 introduction of "transfers to crude oil supply," EIA purposely increased US oil production in an attempt to eliminate the dreaded "adjustment" figure. The reality is that US oil production was meaningfully higher at the end of 2022 (please see our real-time graph for the spike into the end of 2022).

So while headline growth showed +1 million b/d, the reality was closer to +250k b/d to +300k b/d. This, in turn, resulted in overly optimistic US shale oil production growth assumptions into the end of 2024 and 2025.

As a result, most oil analysts are overstating non-OPEC supply figures in 2025, which is pushing them toward the bearish side.

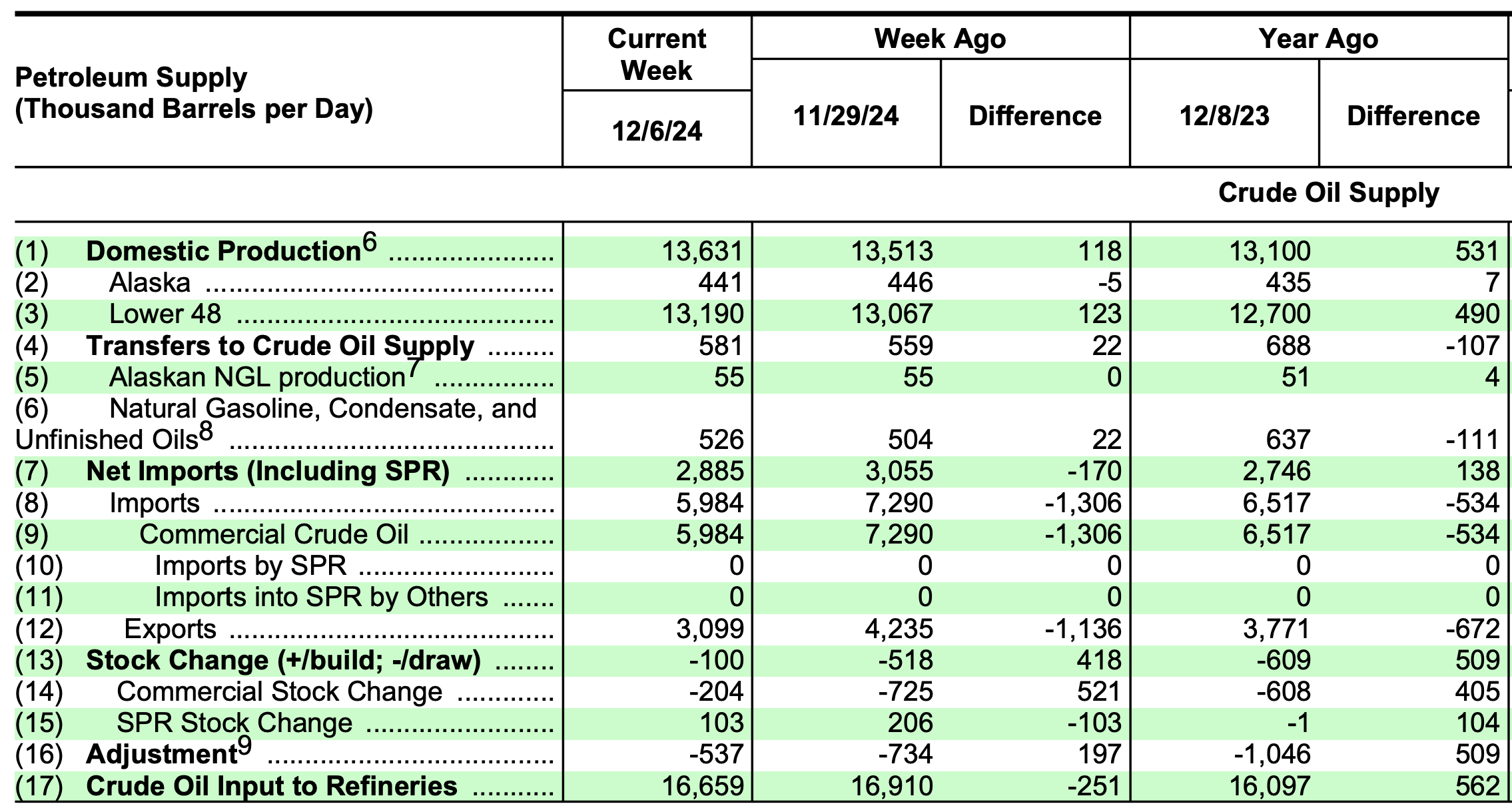

Fast forwarding to today, real-time data is showing US oil production disappointing to the downside, while headline EIA US oil production figures hit an all-time high of ~13.63 million b/d.

Once again, the people unaware of the data are being fooled into believing that US oil production is ramping higher.

While EIA does a great job of disclosing its methodology change and the associated variable changes, people do not pay attention to details, and this week's production increase is simply to match the change in EIA's short-term energy outlook or STEO.

Source: EIA

In fact, more often than not, I have to point out to people that the weekly US oil production figures published by the EIA are not "real" and instead a modeled figure from the STEO. The STEO is just EIA analyst assumptions and has no basis in reality.

Source: EIA

And even for those keenly aware of the data, they only go as far as using the "adjustment" figure to account for the implied difference in US crude balance. But even this method fails to account for the real underlying US oil production trend.

Why?

Because US crude exports are based on customs data. And the EIA explains that there will be differences in timing due to reported customs figures and real exports. This delta is the main reason why finalized crude export figures (from the EIA PSM) are different than what the EIA weekly reporting is.

Such trivial, yet important differences, are why the oil market has more questions than answers. But for people like me who've followed the data this closely for a decade, none of this is a surprise.

So when I say that this oil market is out of touch, it really is. And one of the biggest out-of-touch things with regards to the oil market is the idea that US oil production is ramping.

By my estimate, US crude production today is around ~13.25 million b/d to ~13.3 million b/d. This is flat y-o-y. In October and November, we saw an increase in US oil production, but December is expected to show a drop.

Even if we assume that this week's EIA data was an anomaly, the implied US oil production figure fell to ~12.2 million b/d, which will be hard to reverse back higher. I don't think this is where US oil production is, but the fact that it disappointed that much implies to me that there's no "exit production growth", which is important to understand if you are modeling into 2025.