The Start Of The 3rd Inning - It's Time To Go Back On Offense

Note: This article was first published to subscribers on Jan 3, 2023.

Please read, "Bottom Of The 2nd Inning - What Signs To Look For On Oil."

As 2023 begins, the score is now 4-2. While energy investors managed to play good defense to close out 2022 with solid gains, the 2nd half of 2022 wasn't without its perils. Not only were energy investors blindsided by the China zero COVID policies that materially dampened oil market balances, but the recession in Europe coupled with the strengthening USD pushed investors away from oil. Energy stocks, however, did manage to outperform despite the lackluster oil price performance, but that's something we shouldn't celebrate for long. A high tide will lift all boats, and this is no different for energy investors.

In our view, the themes of 2023 will be one that's centered around offense. The opposition has thrown pretty much everything it had left at energy investors.

Global SPR release with the US contributing the most.

China's zero COVID policy.

The Fed raising rates to fight off inflation.

Even amidst all of this headwind, the structural supply shortage balance managed to hold prices above $70 to $80. It's safe to say now that this wasn't a repeat of 2018, but we can't let our guards down just yet.

If I was to characterize 2023, I would ask you to imagine the following scenario. As we enter the new year, our star hitters are not at bat just yet. We have our 3 weakest hitters coming up (the 1st quarter of 2023). Oil market balances won't be tight in Q1, so it will be a matter of how little we draw or how much we build in Q1 that defines us for the rest of the year. During this time period, China is in the process of reopening and its COVID case counts are spiking. Headline concerns will continue to shake investor sentiment, but for those of us that are rational and calm, we know that the COVID reopening case spike was an eventuality. As a result, the faster COVID spreads in China, the faster the full reopening will take place.

While I am not trying to be unemotional about this, it is important to understand that for the sake of investing, the outcome is all that matters. So as case counts spike, and the spread widens at a rapid pace, the oil demand spike that will take place in a few weeks will be telling just how fast China recovers. And if the western countries are any guide, the jump will be meaningful enough to send a ripple effect across financial markets.

Once we get over the hump of Q1, we will be on offense, and in a very meaningful way. For starters, China's oil demand will be a key driver of global oil demand this year. According to the IEA, China and India are expected to propel global oil demand to ~104 million b/d by year-end.

Relative to 2019, this will be ~3 million b/d higher.

In addition, following the conclusion of Q1, investors will be able to see just how much Russian oil production is lost. In the latest update, Russia has guided to a production loss of ~500k b/d to ~700k b/d. We will see just how true that is soon enough. (FYI, Russia lost ~450k b/d of crude exports in Dec vs Nov).

As for US oil production, we estimate that 2023 will show +650k b/d to +700k b/d. US oil production will exit 2022 at ~12.4 million b/d, a growth of ~700k b/d y-o-y. We expect the 2023 US oil production exit rate to be around ~13 million b/d, or an all-time high, but the pace of the growth will fall off dramatically by year-end. By Q4, it will be evident to most investors (also expressed in US shale earnings calls) that they should no longer expect 3-5% growth. Servicing cost inflation coupled with tier 2 and 3 wells will result in a spike in capital efficiency ratios (the cost to replace oil production, the higher the figure, the more expensive it is). This will prompt most US shale drillers to pursue a mature declining production profile as opposed to one fixated on growth. While most producers are already starting to do that today, most are still guiding toward some type of growth. We think this will end and it will become very evident by year-end.

So as 2023 progresses and the world sees visible production loss from Russia and the inevitable slowdown in US shale, they will start to wonder, "where are the future oil supplies going to come from?" And just as they start to ask these obvious questions, the answers are already laid out in front of them.

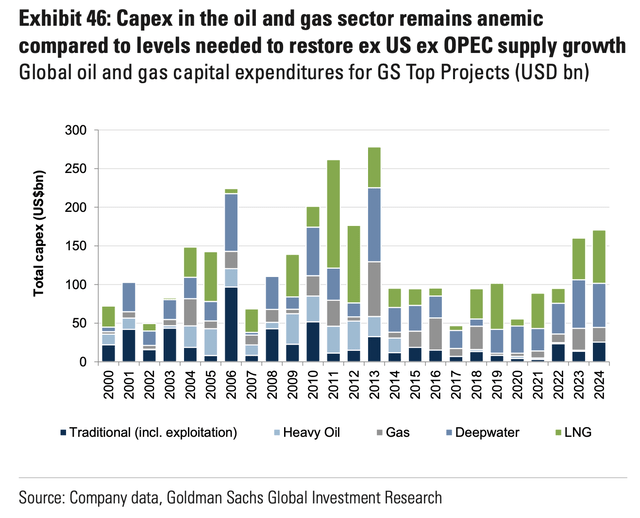

Here is a chart compiled by Goldman on global oil production ex-OPEC+, US, and Guyana. What you will notice is that starting in 2023, these countries will peak and production will decline through 2026. This is an inevitable outcome because there's been a lack of upstream capex spending since 2014.

It's already far too late to change this fact, so the world is just a slow trainwreck in motion to the inevitable outcome of a global oil supply crisis.

Now, what's the caveat to what we just wrote? Well, we need oil demand to materialize to the upside. We need China's oil demand to rebound and we need to see a further recovery in other regions including Europe. And while we are very confident that demand will rebound in a meaningful way, but just like baseball, the opposing team may just get lucky, and we should always be prepared for the worst just in case.

Conclusion

The structural oil deficit will start to show its teeth later this year. But for energy investors, we need to get through the first quarter. We don't have our best hitters up first, so it doesn't mean you go out and borrow "conservative margin" for your portfolio. It means you keep playing defense until the signals change.

Once we get confirmation that China's demand is indeed rebounding and the world isn't falling apart, we play offense, and we play some aggressive offense. As we wrote in this article, the world isn't prepared just yet for the question of, "where are the future oil supplies going to come from?" People are still too oblivious, but who can blame them? ESG this, climate change that, they don't have time to ask the simple question of, "do we have enough oil supplies for the next 1, 2, 3, or 5 years?" Well, they are running out of time, but we did, and we are prepared.

Let's get through Q1, then let's play some aggressive offense.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours.