This Is Going To Be A Headwind For The Oil Market For The Rest Of The Year

For those of you that think oil prices will spike, you need to discard that assumption and come to reality. Barring an exogenous event where something happens to supply in a very meaningful way, the odds of a price spike are very, very, very low. The reason being is that the US implied oil demand is clearly, obviously, and unmistakeably weak.

Following last week's crazy US total implied oil demand drop, EIA showed a massive jump in implied demand of 2.305 million b/d. The issue with this jump, however, is that gasoline only contributed 0.459 million b/d. Relative to 2021, we are now 720k b/d below last year's demand figures.

At some point, we can't keep saying, let's wait and see how demand holds up. The reality is that high prices are impacting consumers and we are now seeing it in the data. As a result, it is clear and obvious to us that with where demand is at now, US oil inventories are no longer drawing as much as before.

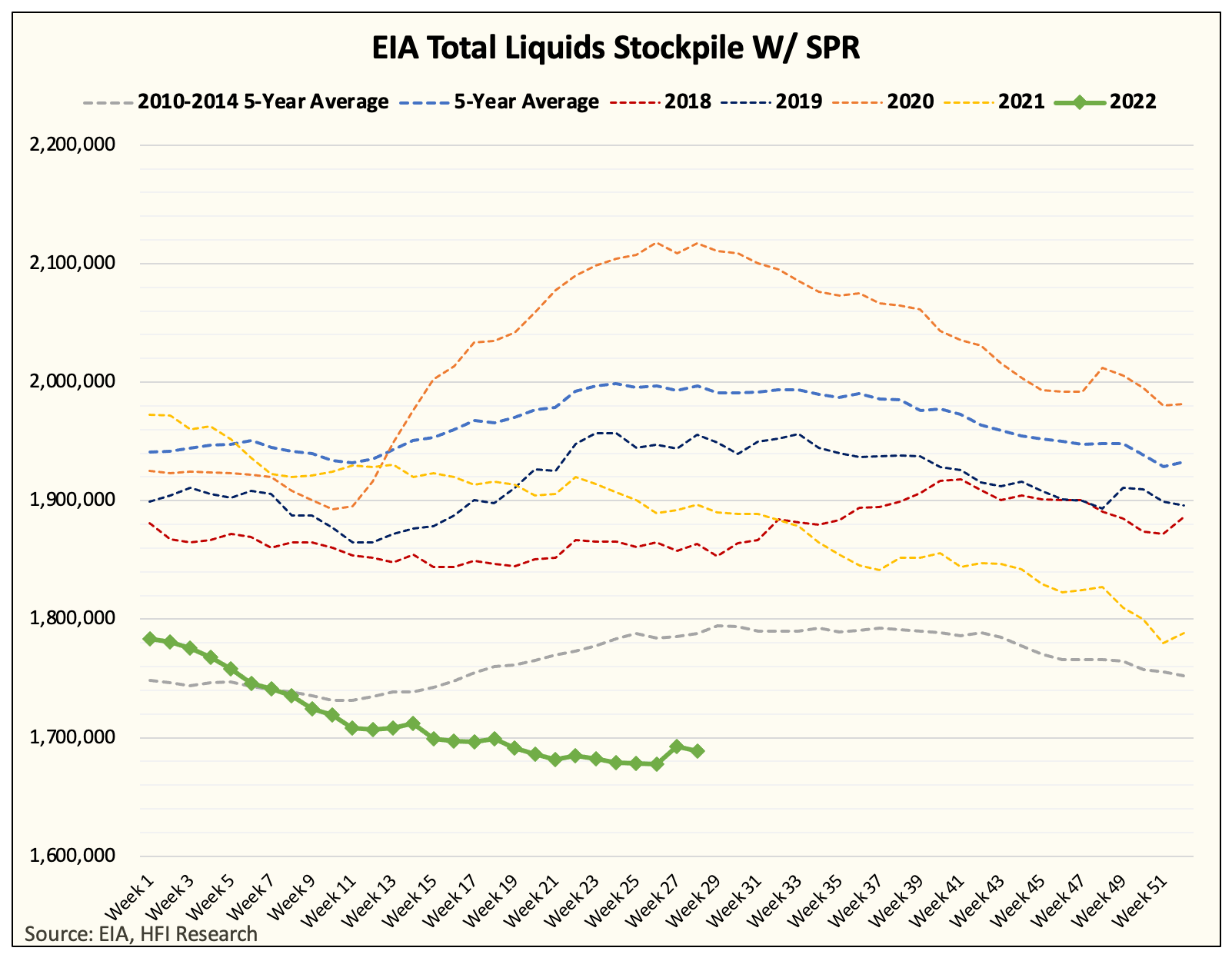

You can see this in the latest EIA total liquids stockpile chart where inventories have flatlined since April.

While it was expected that Q2 global oil market balances will show a small deficit, we expected Q3 to be at least -1 million b/d. As a result, if total liquids stop drawing, then we have an issue on our hands. And the culprit is the weak demand figures.