US Oil Demand Starting To Recover But More Is Needed

With every passing week, the longer it takes for US oil demand to "recover", the more obvious the demand destruction from the recent surge in oil price. Our OMF yesterday noted that comparing crude to the 2008 level to gauge demand destruction is inadequate. Consumers use petroleum products, so consumers are already paying close to $180/bbl on refined product prices.

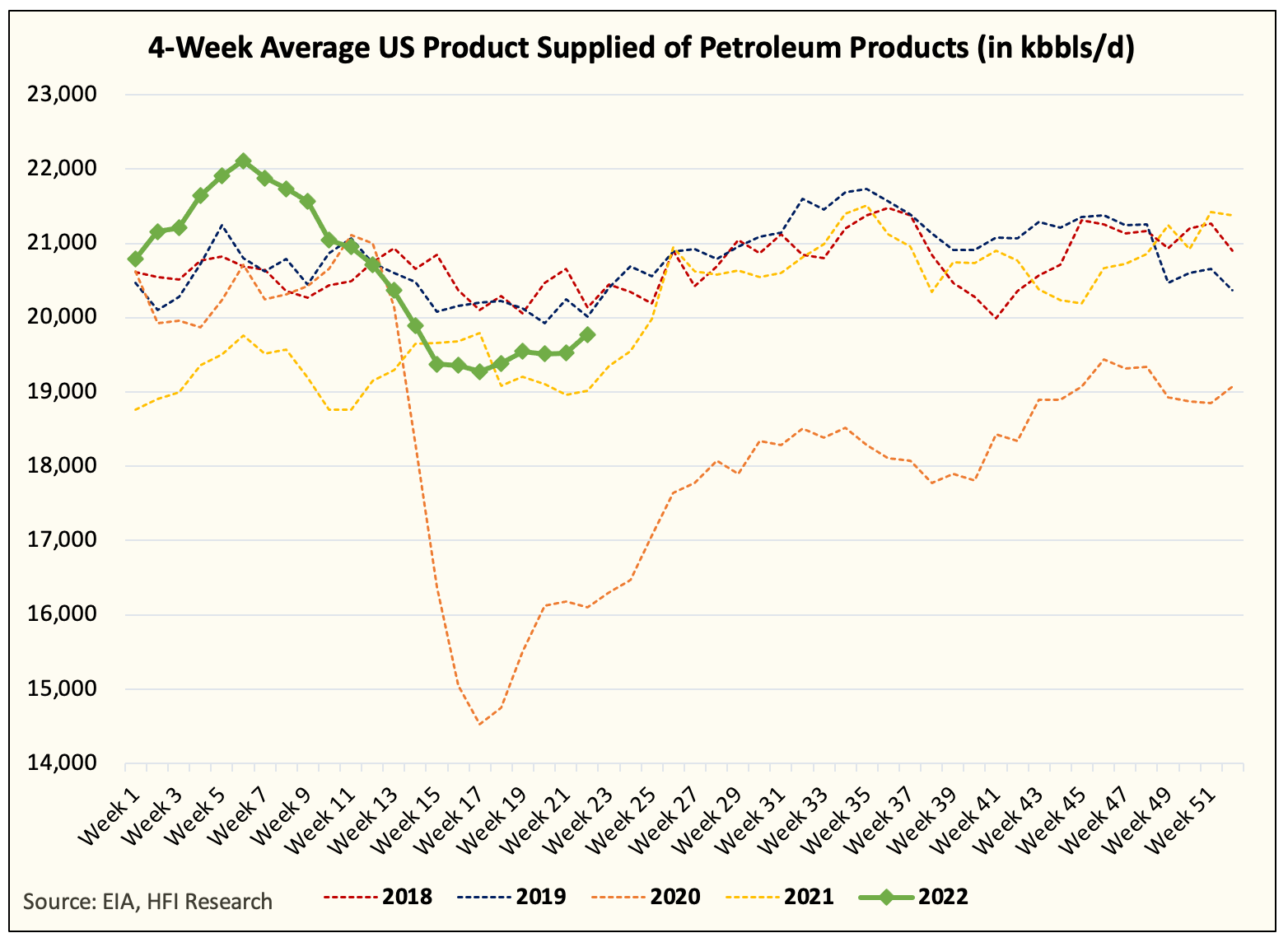

This is why it's important to gauge the implied US oil demand figure the EIA publishes every week. While it's not a perfect measurement of demand, it's the best we have, and it's proving to be a good approximate gauge for demand.

Now if you look at the total implied US oil demand in the chart above, you can see that we have recovered quite well from the trough. We are still ~350k b/d below that of 2019, but with the peak demand months ahead of us, we could be well on our way to the 2019 level.

But if we break the demand components down, gasoline, distillate, and jet fuel are still lagging a bit.

You can see that we are just matching the 2021 levels for now.

And if you break it down to all of the components, the recent rise in jet fuel is encouraging but remains below that of 2018/2019. Residual fuel oil has helped push total demand higher, but gasoline needs to move materially higher for total US oil demand to surpass 2019 levels.

Now here's the reason why we believe demand needs to recover further. At the current implied demand and the current refinery throughput, the total US liquids saw a small build of ~3 million bbls. Gasoline, distillate, and jet fuel saw a build this week suggesting ~16.3 to ~16.4 million b/d is sufficient to prevent us from further draining inventory.

Seasonally speaking, product storage usually builds/move sideways from here into the fall maintenance season. But this year is different given the recent rise in oil and the rise in refining margins. If US oil demand fails to recover from here (low probability of happening, but entertain us), then refining margins will fall, product storage will build, and crude will lose the tailwind for moving higher.

The market will also perceive the lack of a demand recovery to the recent rally in oil suggesting demand destruction is firmly taking hold. This will result in bears having the firepower to push prices lower.

While we think this is a low probability scenario, it is something to ponder over.

Now, what happens if US oil demand eclipses 2019 levels by the end of June? Well... given refinery throughput will get maxed out around ~16.6 to ~16.8 million b/d, we would see a scenario of elevated refinery throughput, product storage draw, and crude storage draw. Total liquids will decline and oil prices along with refining margins will have to move even higher to "prompt" demand destruction.

We think the most likely scenario is that 2022 US implied oil demand will lag 2019 just by a touch prompting refining margins to drop a bit from here while crude rallies. Product storage will remain flattish going forward while refinery throughput peaks around ~16.7 million b/d.

The net effect is that crude should remain in a reasonable range between $115 to $130 (for the summer) and energy stocks should enjoy a period of stable/high prices. So unless demand recovers materially higher from here, or drops materially lower from here, we don't see that price band changing much.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours.