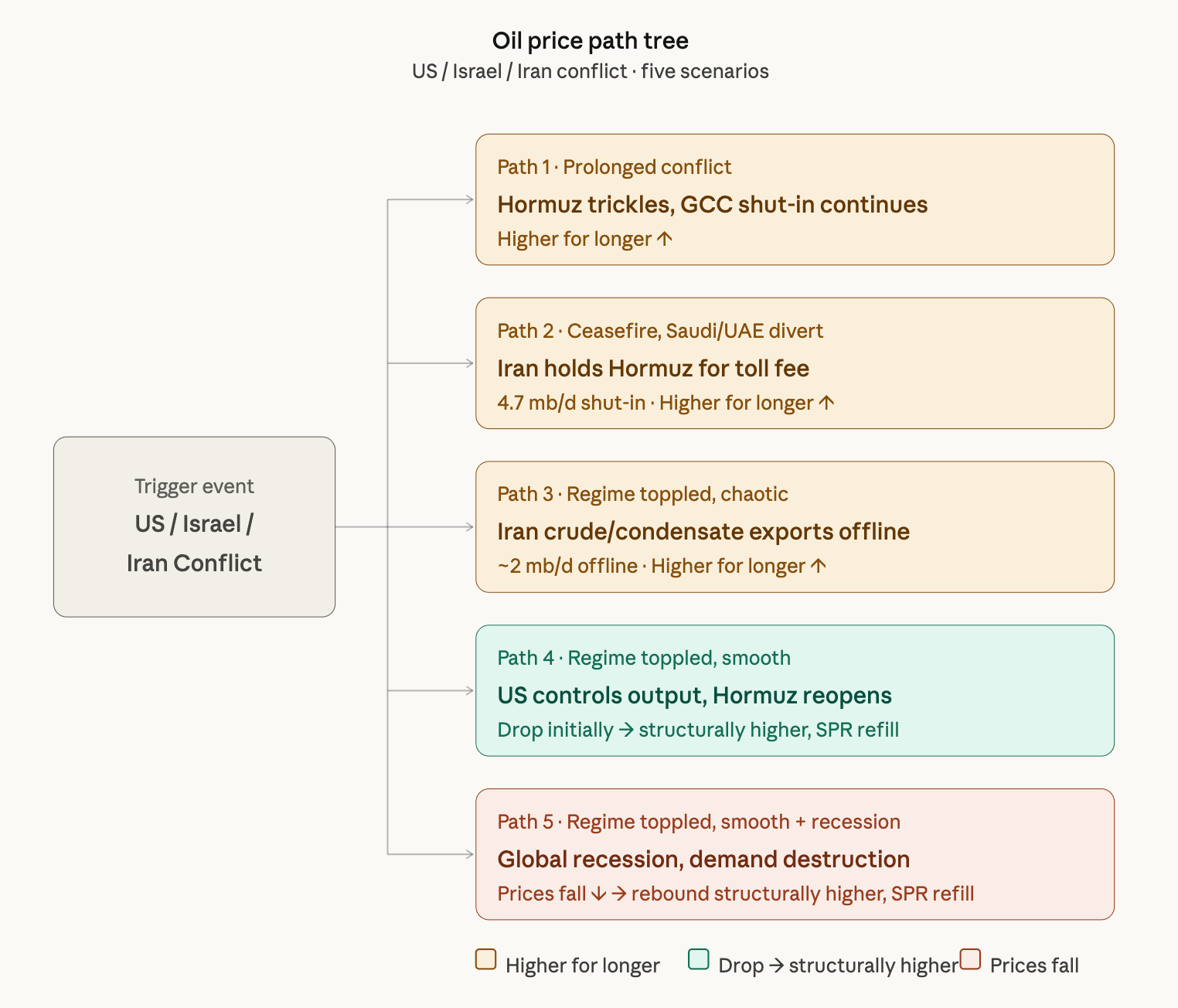

In our last week’s WCTW, we discussed how the oil market will never be the same again. Here are 5 of the paths we are looking at when confronted with the “long-term” direction of the oil market:

What does structurally higher for longer look like?

It is dependent on the resolution of the current conflict. With each passing day, the world is losing 11 million bbls of crude oil. The math of the supply outage is straightforward:

April 30 ceasefire: 1.2 billion bbls of crude + product lost

May 31 ceasefire: 1.5 billion bbls

June 30 ceasefire: 1.8 billion bbls

This is a rough estimate, as the oil price in the near term will have to reach a level that triggers demand destruction before we get to the May or June scenario. Available commercial crude oil inventories are much lower than people think.

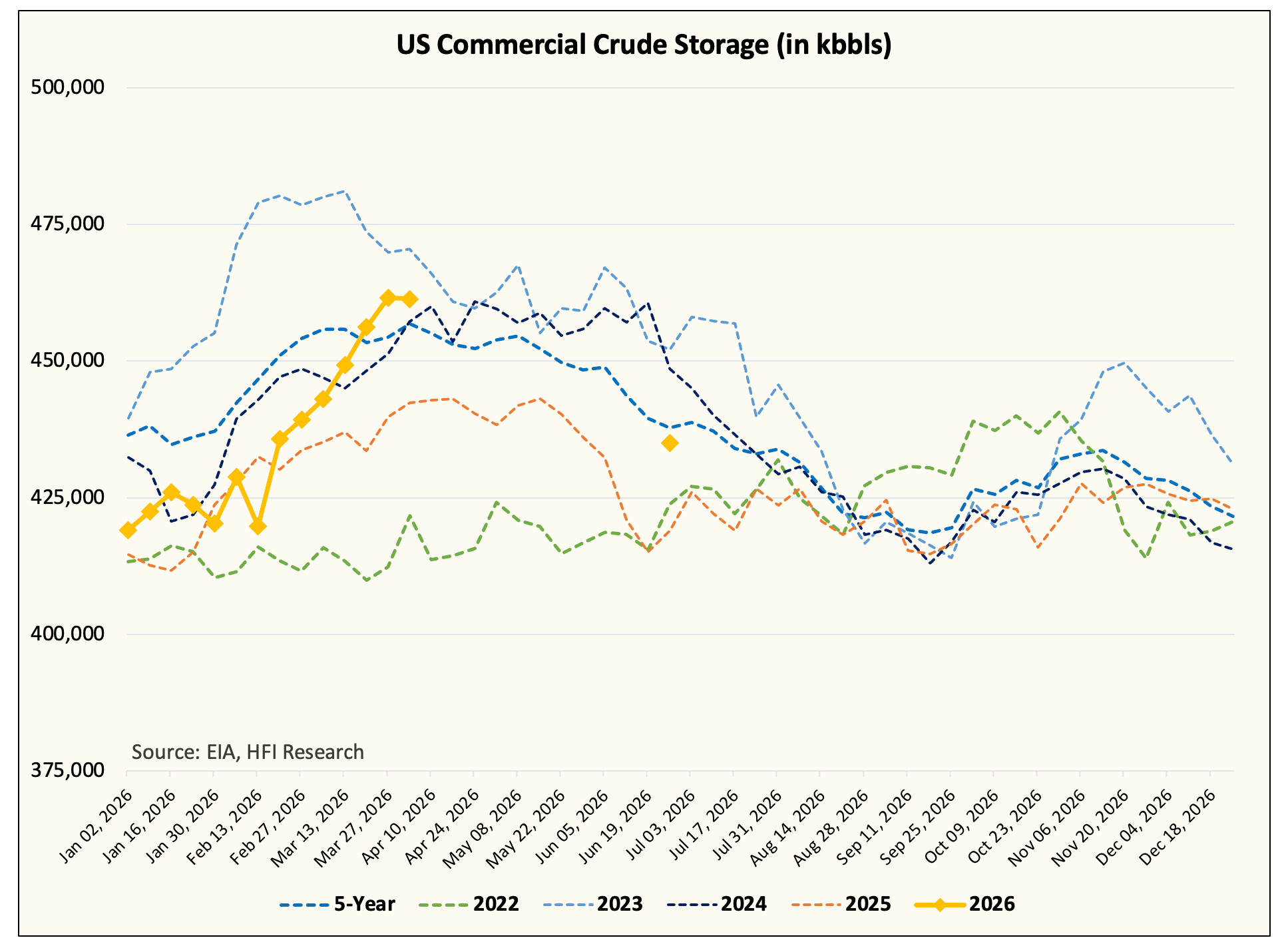

Commercial Storage Math

Here’s a good illustration of this:

US commercial crude oil storage is expected to reach ~435 million bbls by the end of June, regardless of whether the Strait of Hormuz is open or closed. The US does not import a meaningful amount of crude from the Middle East, so the impact is second-order in nature. Instead, US oil inventories would look like this: crude and product imports will decline as they are diverted to other regions, and US crude and product exports will spike.

In essence, the US will be the last place to draw down inventories.

For US commercial crude storage, we can not go below ~400 million bbls. Linefill, volumes required to operate pipelines, and operational minimums require that US commercial crude storage hold at least ~380 million bbls. From June onward, that leaves us with a cushion of ~55 million bbls. The good news is that the US is releasing SPR, so most of it will be exported, and that will dampen the impact of the decline in commercial crude storage.

JP Morgan estimated the operational minimum for OECD commercial crude oil inventories at ~842 million bbls. As of March 2026, we had ~1.02 billion bbls. This puts the effective capacity at 178 million bbls.

Now here’s the math:

IEA announced a ~400 million bbl SPR release.

Daily release volume: 2.5 million b/d.

April, May, and June volumes total 227.5 million bbls.

Effective capacity 178 million bbls + 227.5 million bbls = 405.5 million bbls

Outage from the Strait of Hormuz is 11 million b/d.

April outage is 330 million bbls. SPR release is only 75 million bbls. Net outage is 255 million bbls. We will have already eaten through the effective capacity of 178 million bbls.

This is why the oil market’s breaking point is this month, not in May or June as some analysts expect.