Non-OPEC supplies are peaking a lot sooner than you think. I am dead serious. I will present a no bullshit analysis to you in this article. It will be concise and straight to the point.

For non-OPEC supplies, IEA believes there are 4 growth engines:

US shale

Canada

Brazil

Guyana

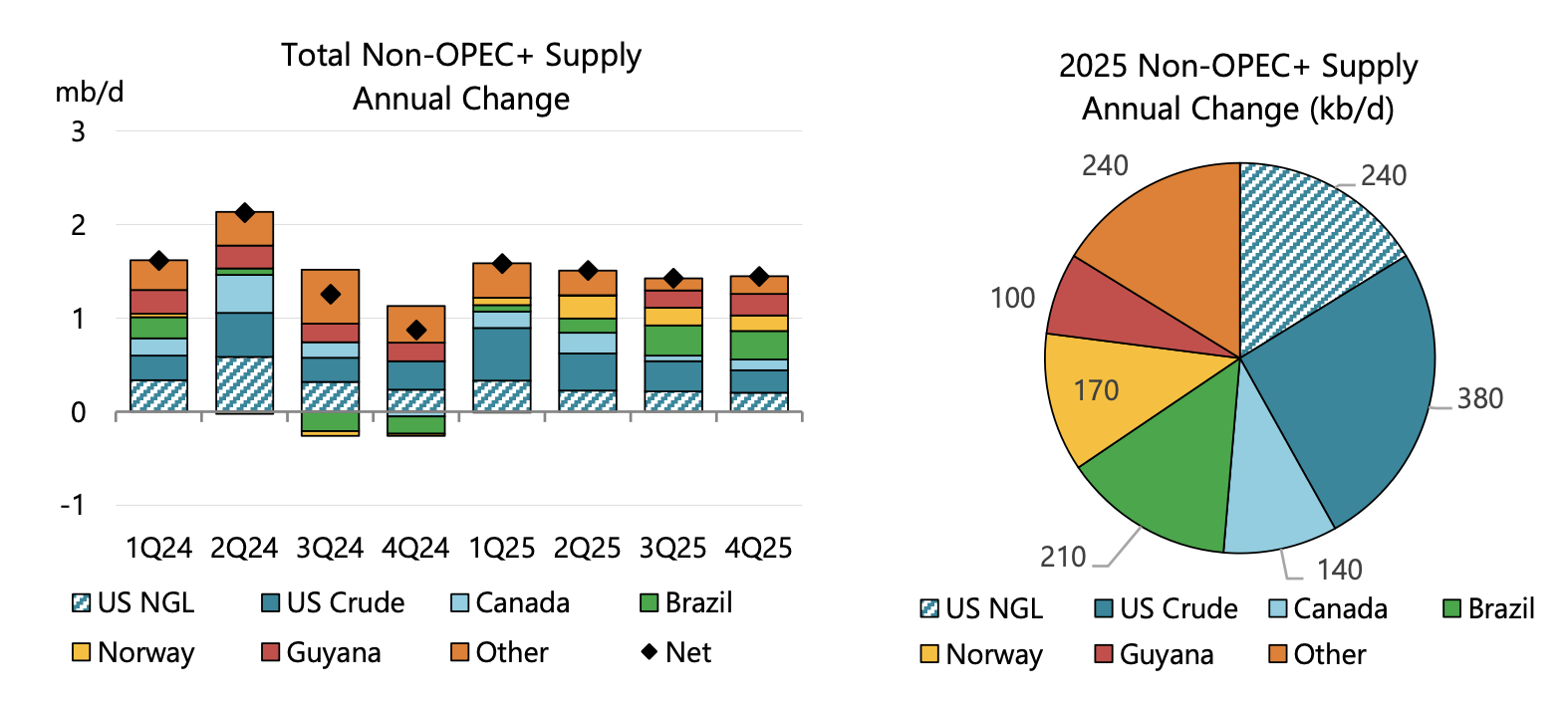

For 2025 oil market balances, these four countries are expected to add 930k b/d. In particular, the US is expected to add 620k b/d of liquids growth. Aside from these four countries, others are supposed to add 410k b/d.

In this article, our focus will be centered around Brazil and the US. I will show you why not only are the growth projections unrealistic, but the data so far has invalidated most analysts' estimates.

The Cold Hard Truth In US Oil Production

On Nov 9, we published an article titled, "The Peak In US Oil Production Is Here And Why You Need To Own Energy Stocks." This was an extremely important article because it highlights a lot of the things that will be discussed today. In particular, the biggest takeaway from the article was that Chevron announced it would stop growing the Permian production base.

We noted that the falling crude reserves relative to the rising natural gas reserves were one of the reasons why operators need to start planning for the long term. Growing production is an easy fix if the producers can grow reserves at the same pace. But if crude reserves are declining while production is growing, you are only shortening the lifespan of the assets. This is why you are seeing Permian operators pivot towards longer laterals and lower well counts. By managing the long-term decline of the assets, it can maximize the net present value and create more value for shareholders.

But none of this has made it into the sell-side community or the IEA. Instead, most analysts are still fixated on the idea that US oil production will grow despite the facts pointing to the other direction.

Let's look at some of the data points for clarity.