Two weeks ago in our WCTW, we wrote about "following the process" and what it meant for the oil market. We wrote:

The combination of positioning + refining margin weakness indicates to us that the market has successfully figured out where the near-term top is. Like all things markets, it can still very well go against this fundamental backdrop and push higher, but informed readers should know that it won't last.

Since then, the oil market has been distracted by the Israel/Iran conflict which sucked in uninformed investors/traders expecting oil prices to move higher on the potential for more geopolitical conflicts. With the benefit of hindsight, the geopolitical events never turned into a material and sustainable increase in oil. Why? Because the underlying fundamentals are not currently supportive of higher prices, and while geopolitics always can obfuscate reality in the near term, fundamentals ultimately win out.

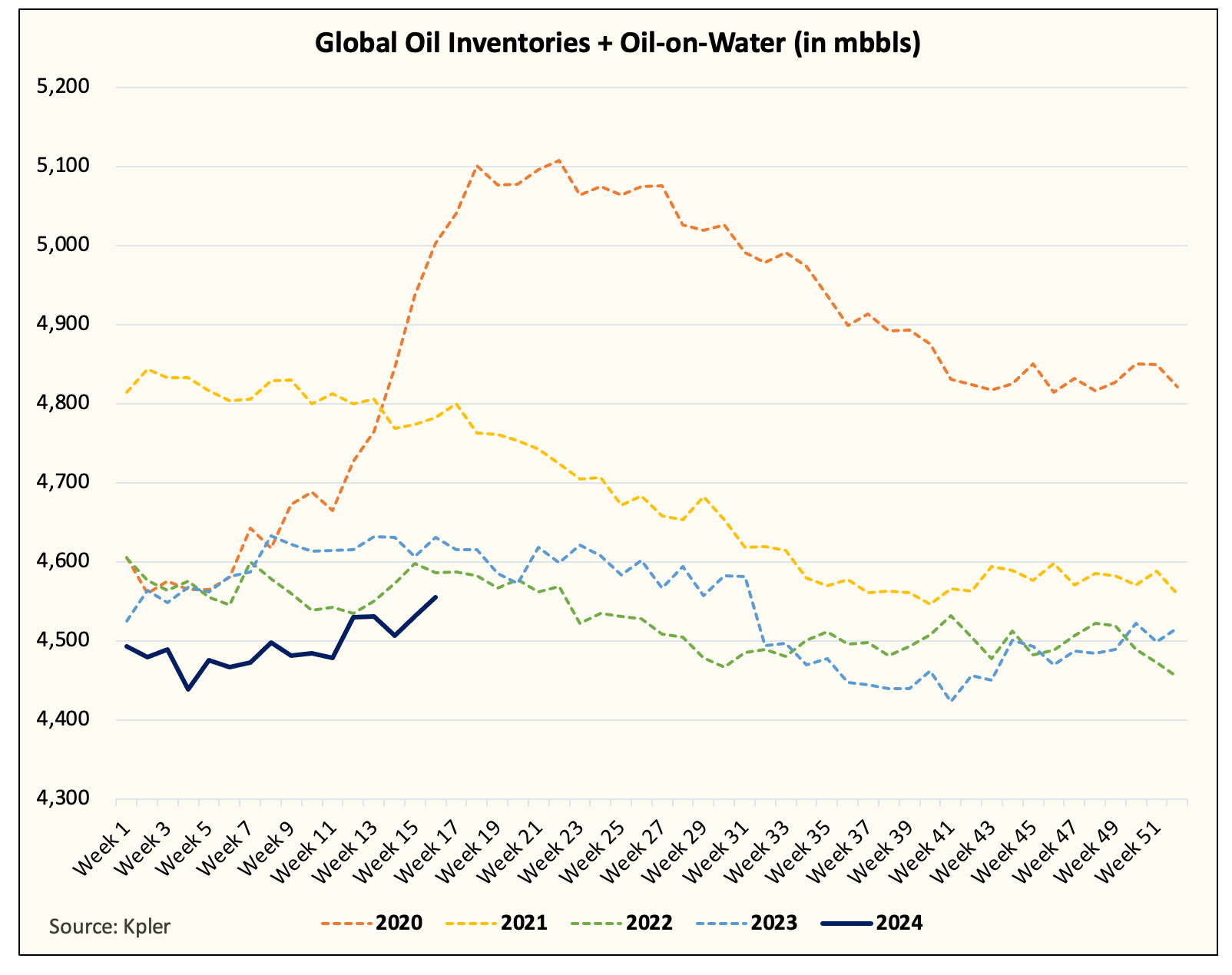

Fast forwarding to today and with WTI pulling back slightly, we see the near-term weakness in oil persisting. Global oil inventories are on pace in April to wipe out all of the draws we have seen since the start of the year. And while we are entering summer demand season with historically low oil inventories, we need to be mindful of the implied balance April is showing us.

The most troubling sign, however, is the recent price action we are seeing in the distillate complex. Historically, distillate has always been the product market that's in deficit. So with the recent weakness, it does make us question just how strong global oil demand is. As we've long said, demand is very hard to gauge, and the only way to figure out demand in real time is to look at refining margins. So despite the pullback we have seen in crude, refining margins are failing to keep pace, this is another sign that oil has more room to pullback.