(WCTW) Powder Keg

Positioning and sentiment have priced oil as if the Iran conflict is over. This is a market that's sitting on a powder keg with someone holding a lit match.

Oil markets always move to extremes, but this is the first time in history that the market may be getting way too extreme.

Let me explain.

Global oil inventory buffers are running out. US SPR release is set to fall to zero after August.

US commercial crude oil storage will fall below ~400 million bbls by the second week of July.

Iran has demonstrated, again, that it can close the Strait of Hormuz this weekend. This time, it’s about the conflict in Lebanon. Last time? It was the Naval Blockade. Even with the US announcing that there will be a 60 day sanction relief on Iranian petroleum exports, Iran is increasing its leverage, not the other way around.

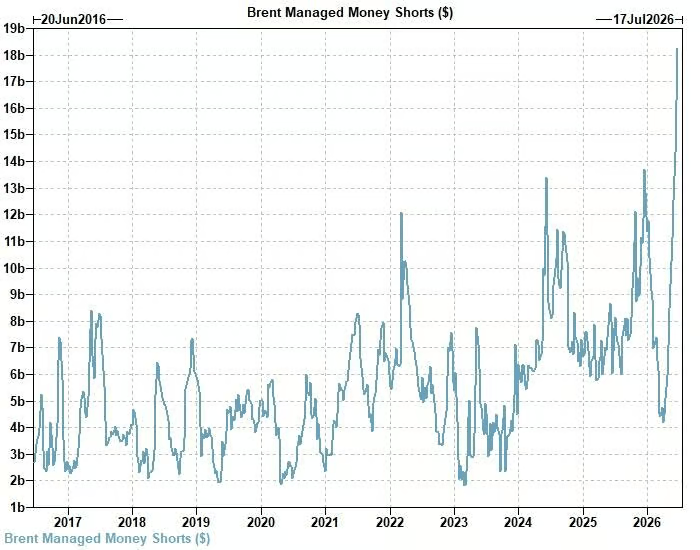

Meanwhile, Brent short positioning is at an all-time high. All the while, global onshore oil inventories continue to draw, refining margins remain elevated (signaling no demand destruction), and the market has priced in a complete recovery and more.

Production shut-in excluding Iran and Qatar remains around 7.8 million b/d. Note: More on the math below.

My bullish stance on the oil market has not changed. This is a market that got extreme on the other side. It’s a guy with a lit match sitting on a powder keg. It will inevitably swing to the extreme on the other side.

Powder Keg

Extreme positioning has been a key reason why oil prices have disconnected from reality.

This is now the largest Brent managed money short position in history. As I explained in my memo, the financialization of the oil market since 2014 has made it very difficult for real price discovery in the physical oil market. Andy Hall, nicknamed the oil trading god, retired in 2017 because he could no longer handle how disconnected the market could get from time to time.

In this case, it is important to understand the oil math to see why so many commentators are saying that “crude is in surplus.”