(WCTW) Short-Term Pain For Long-Term Gain? Yeah, But How Much Longer!

OPEC+ and US shale, yeah, oil fundamentals.

Editor’s Note: That’s not my face, but I am Asian. And it is a close resemblance to my reaction today.

Short-term pain for long-term gain.

Yeah, we've all heard that before.

Go on a diet today, and lose weight in the long run.

Spend less than you make, invest/save, and you will be rich in the long run.

But what if I don't want to wait for the long run? What if I've suffered enough from short-term pain?

When it comes to energy investing, I'm having those moments of flashbacks again. 2018, 2020, 2022, you name it. And the sad thing is that I can't count those instances on one hand anymore, I need 10 people's hands to count all the torment!

When is enough enough?

As I sat there in front of my desk this morning, I couldn't help but just start laughing at the tragicness energy investors are going through. First, Atlanta Fed GDP estimates tank deeply into the negative territory sending all the recession bears back in the fold.

Then OPEC+ announced that it would not delay its voluntary production cut for another quarter and instead, opted to start its scheduled production increase in Q2 2025.

Finally, when it rains, it pours, Trump announces that he's following through on the tariffs on Canada and Mexico.

As I aptly described my day to a friend today, it was as if I had gotten into a car accident, opened my door, got hit by another car, carried into the ambulance, and the ambulance fell off a cliff.

When will this end?

I don't know, but the increasingly frustrating nature of this market is that even for energy specialists such as myself, we are losing patience. A sign of the times, or perhaps this, in itself, is a contrarian indicator.

OPEC+

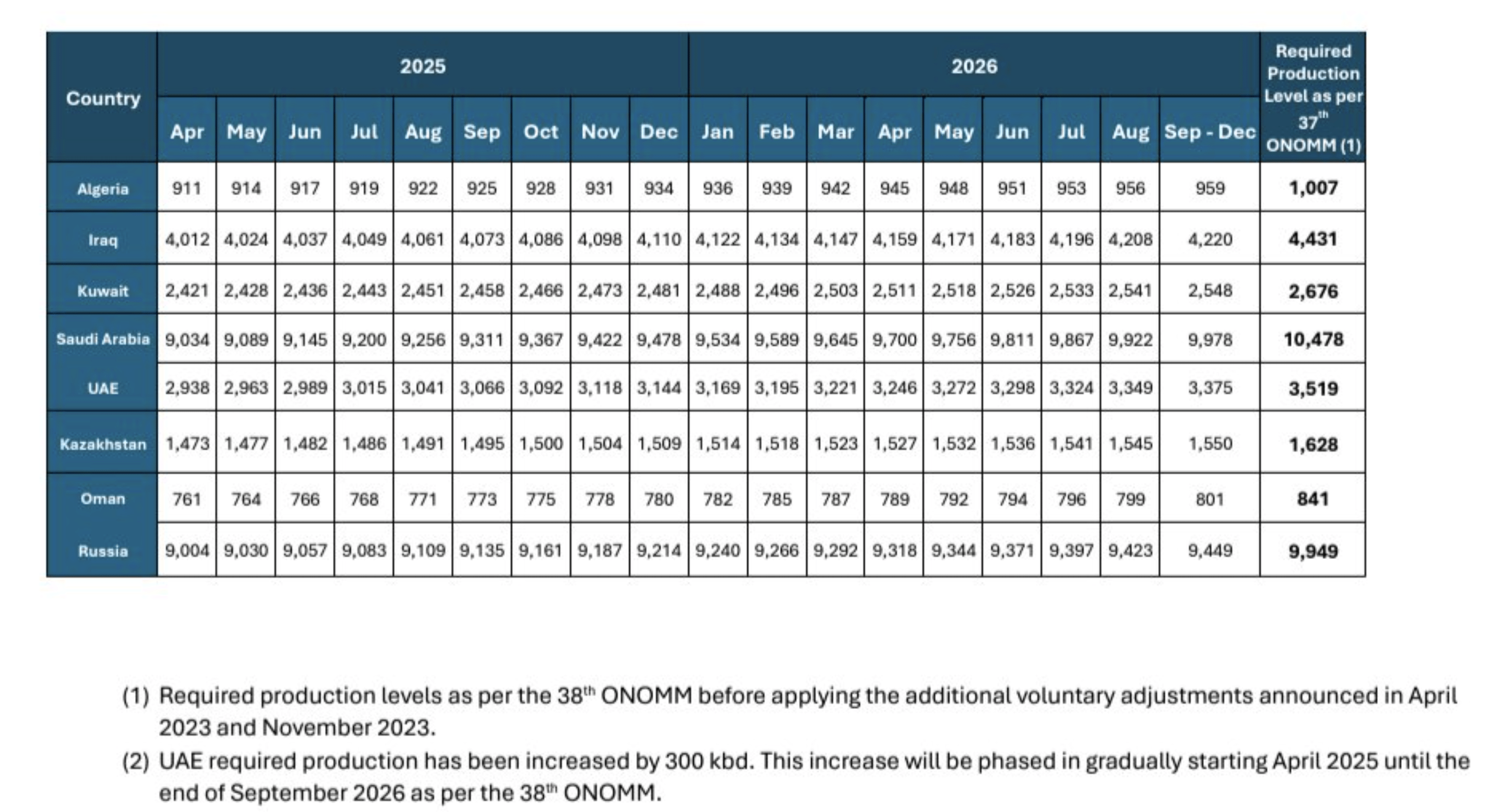

OPEC+ surprised the market consensus today with the announcement that it's unwinding its voluntary production cuts starting in April. This is in contrast to the prediction we had for another quarterly extension.

OPEC+ in Dec 2024 had extended the voluntary production cut to the end of Q1 2025 and extended the timeline of how fast it will increase production (Dec 2026). The delayed nature of the production increase makes it so that the monthly increase is very gradual: +135k b/d per month.

By year-end, OPEC+ will have increased production by ~1.215 million b/d and reduced its spare capacity by the same amount.

And unsurprisingly, immediately following the OPEC+ announcement, the oil market sold off. The sell-off wasn't obvious if you watched the physical market (timespreads & refining margins), but it was very obvious if you watched flat prices.

With WTI flirting around $68/bbl, oil speculators are once again slinging long positions back and forth like a pachinko ball.

Source: Giovanni Staunovo

As of the last CFTC positioning update, money manager positioning remains elevated, but we suspect the recent flush in price will likely correspond with materially lower positioning.

But for oil watchers who have tracked the OPEC+ meetings, you will remember the bear narrative that prolonged production cuts are not bullish because the availability of spare capacity is in itself a ceiling to prices.

However, with OPEC+ finally letting production increase just as non-OPEC supplies disappoint (namely the US & Brazil), and inventories are counter-seasonally declining, the market still views it as bearish, because... well, it's the oil market.

But don't let logic get in the way of the narrative, because for most analysts, OPEC+ production was always penciled in for the 2nd half of 2025. Whether it was an increase in Q2 or Q3, the difference in supply & demand is very negligible.

Supply & Demand