(WCTW) Stuck Between A Rock And A Hard Place

The global markets are not prepared for what's coming.

I am baffled by the broader market’s reaction to the current Iran conflict. I have seen many smart people conclude that Trump can unilaterally end this conflict and that all will return to normal. This is so detached from reality that it’s hard to even comprehend.

During the past 2 months, we’ve seen the following, and they have all been proven incorrect:

The lack of insurance is the cause of the standstill in tanker traffic in the Strait of Hormuz.

The Strait of Hormuz will “gradually” reopen. Countries will ink country-specific deals in exchange for a toll fee.

Trump can unilaterally exit the conflict.

I’m not going to sit here and pretend like I know what’s happening in geopolitics. I don’t. But I’ve had enough humility to realize that when the facts change, I change my mind.

From the start, it was obvious to energy specialists that a toll fee arrangement in the Strait of Hormuz was a nonstarter. The Gulf countries would be held hostage by Iran’s ability to dictate traffic flow, which would make it the most powerful oil producer in the world. We detailed why in this piece titled, “The Unacceptable Status Quo And Why The Oil Market Will Never Be The Same Again.”

It is also clear now that this is not an insurance issue, far from it. On April 18, the IRGC demonstrated how it physically implemented the Strait of Hormuz closure by forcing tankers to turn around midway. I mean, these tankers literally tried leaving, and they were forced to turn around. Anyone who thinks this is still an insurance issue is depicting the scenes from the movie “Don’t Look Up.”

Finally, the idea that President Trump can unilaterally end this conflict and all will return to normal is just crazy. Now that Iran has demonstrated its ability to control the flow, it has one of the most powerful economic weapons. By restricting flows, it effectively replaces OPEC as the world’s most powerful oil producer.

Again, this context is important to understand.

Historically, global oil market balances are off by 1 to 2% at most. A 2% imbalance (~2 million b/d) is already considered either very tight or very loose. For people who have never built a global oil supply-and-demand model, this point is not well understood. Oil prices trade on the margin; the last barrel sets the price. There are people in the industry who still believe that contango in the futures curve signals higher oil prices, while backwardation signals lower prices. You really can’t make this stuff up.

Nonetheless, a global imbalance of 1 to 2% has historically translated into $ 25-per-barrel swings in either direction. We have a 12% imbalance today.

12%, 12 million b/d

That’s not a rounding error. That is literally a catastrophe in the making.

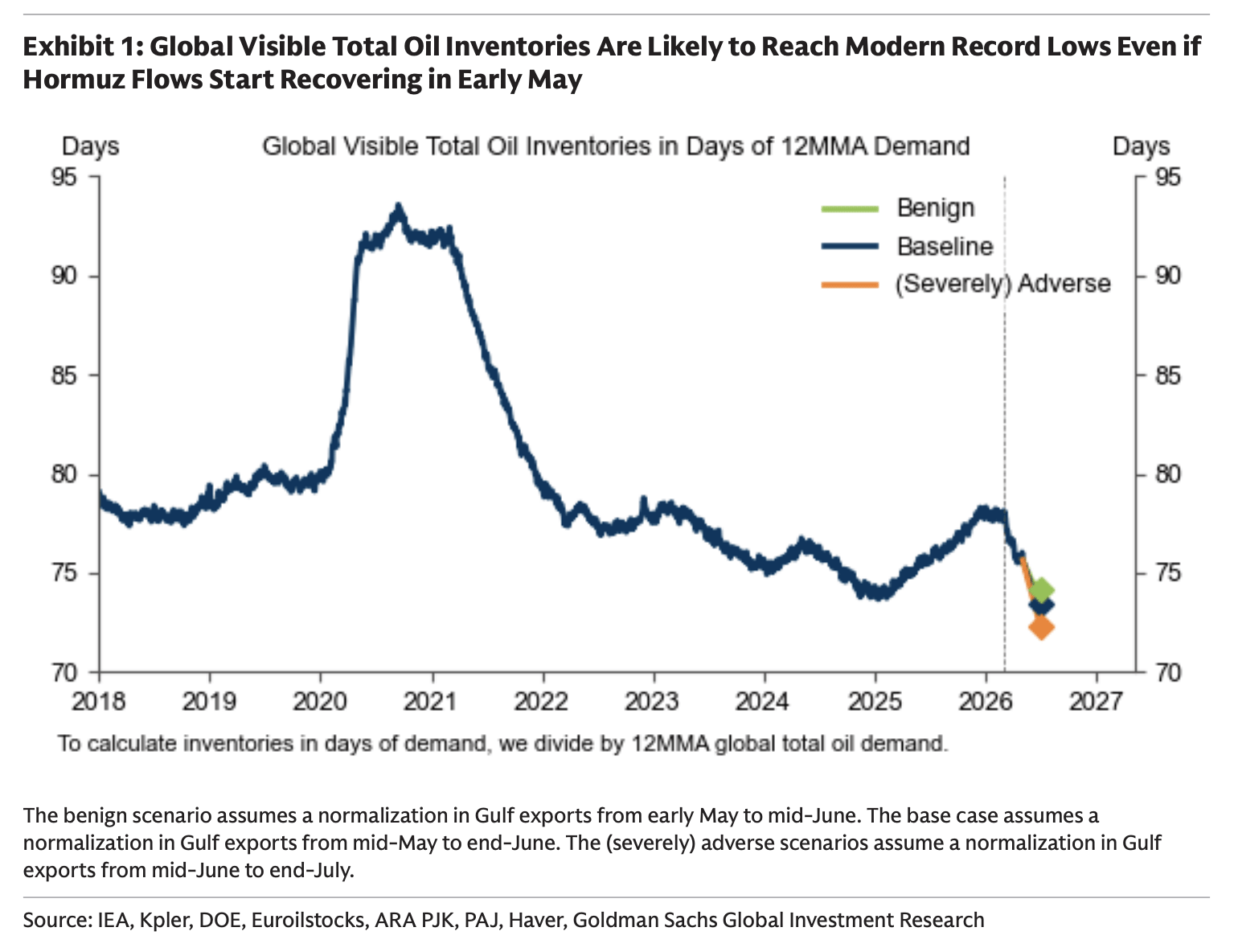

You don’t have every energy specialist looking at barrels and storage all coming to the exact same conclusion. Not one person right now who counts barrels for a living thinks we will somehow escape the situation that we are in unscathed. The oil market breaking point is already here. We are headed for record-low oil inventories, even if the Strait of Hormuz opens this very second.

So yes, we are stuck between a rock and a hard place.