For most oil analysts, getting lost in the weeds is extremely easy. US oil production may underperform or outperform by 150k b/d, but the reality is that if your oil bull thesis is contingent on US oil production underperforming by 150k b/d in 2025, then the margin of safety is far too slim.

I'm here to tell you that for the structural oil supply deficit thesis to take hold, it's more dependent on global oil demand growth going forward versus supplies underperforming.

The Numbers...

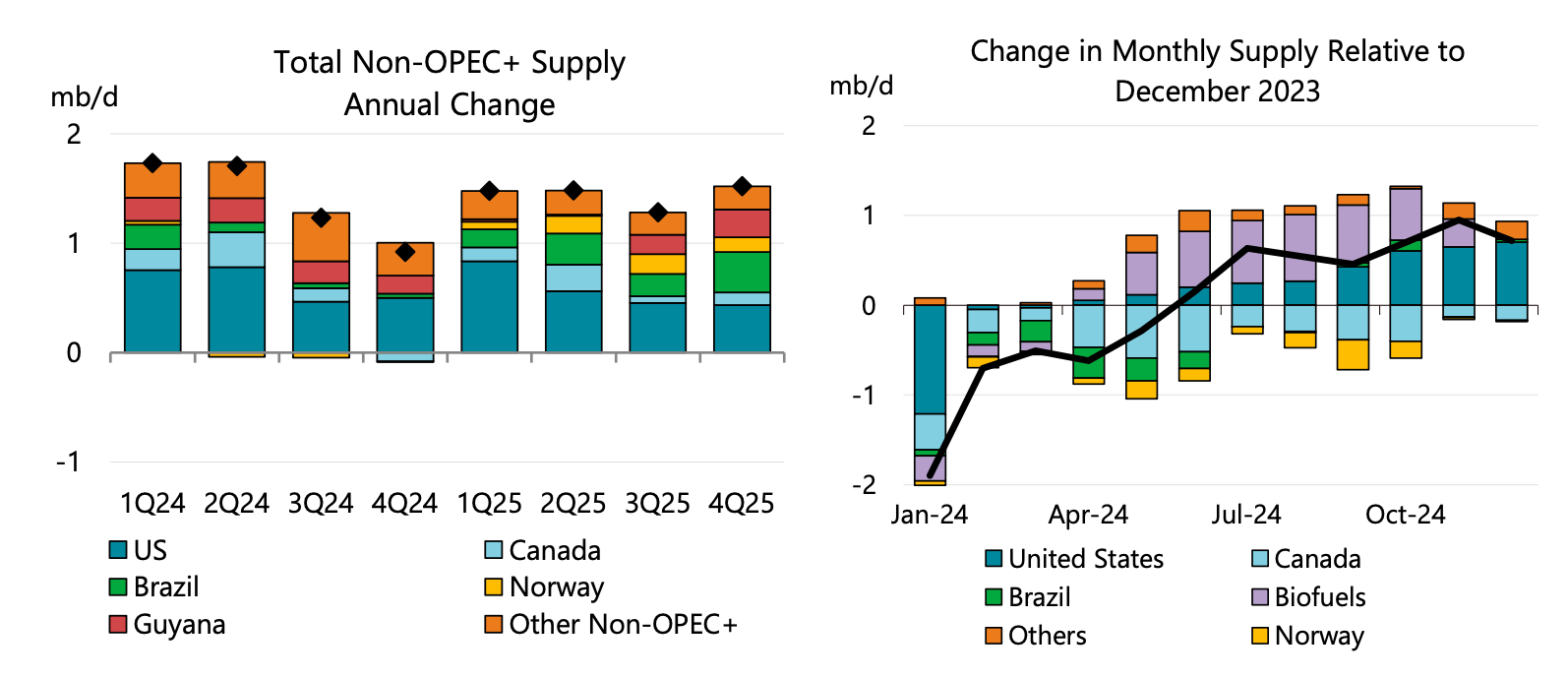

In IEA's latest oil market report, this is IEA's projection for non-OPEC supply growth.

Source: IEA

After going through each assumption the IEA made for the US, Canada, Brazil, and Norway, we were able to shave off roughly ~500k b/d for 2025. This is driven by the fact that IEA almost always assumes a perpetual bullish supply picture.

In IEA's future supply projections, it assumes almost no maintenance and no real seasonality in the Canadian, Brazil, and Norway production. And for the US, it is using ~13.35 million b/d for the baseline production in 2024, when the reality will be closer to ~13.2 million b/d.

Putting it all together, IEA is overestimating supplies by ~0.5 million b/d for 2025.

But the real kicker is on the demand side, which is the point of this article.