(WCTW) The Incoming OPEC+ Production Agreement Will Be Nothing But Paper Barrels

Why production increases are an illusion and the oil market remains firmly in Saudi Arabia's grasp.

Oil prices have already factored in the potential supply increase coming from OPEC+. On March 1, the eight OPEC+ producers are expected to meet to discuss the further unwinding of the production cuts. At the moment, the group is contemplating increasing production by ~137k b/d. This is expected to continue for the rest of 2026.

From a fundamental standpoint, further production increases won’t impact the physical oil market one bit. Psychologically, it might appear that OPEC+ is trying to pressure non-OPEC supplies lower, but realistically speaking, OPEC+ is already producing near max capacity.

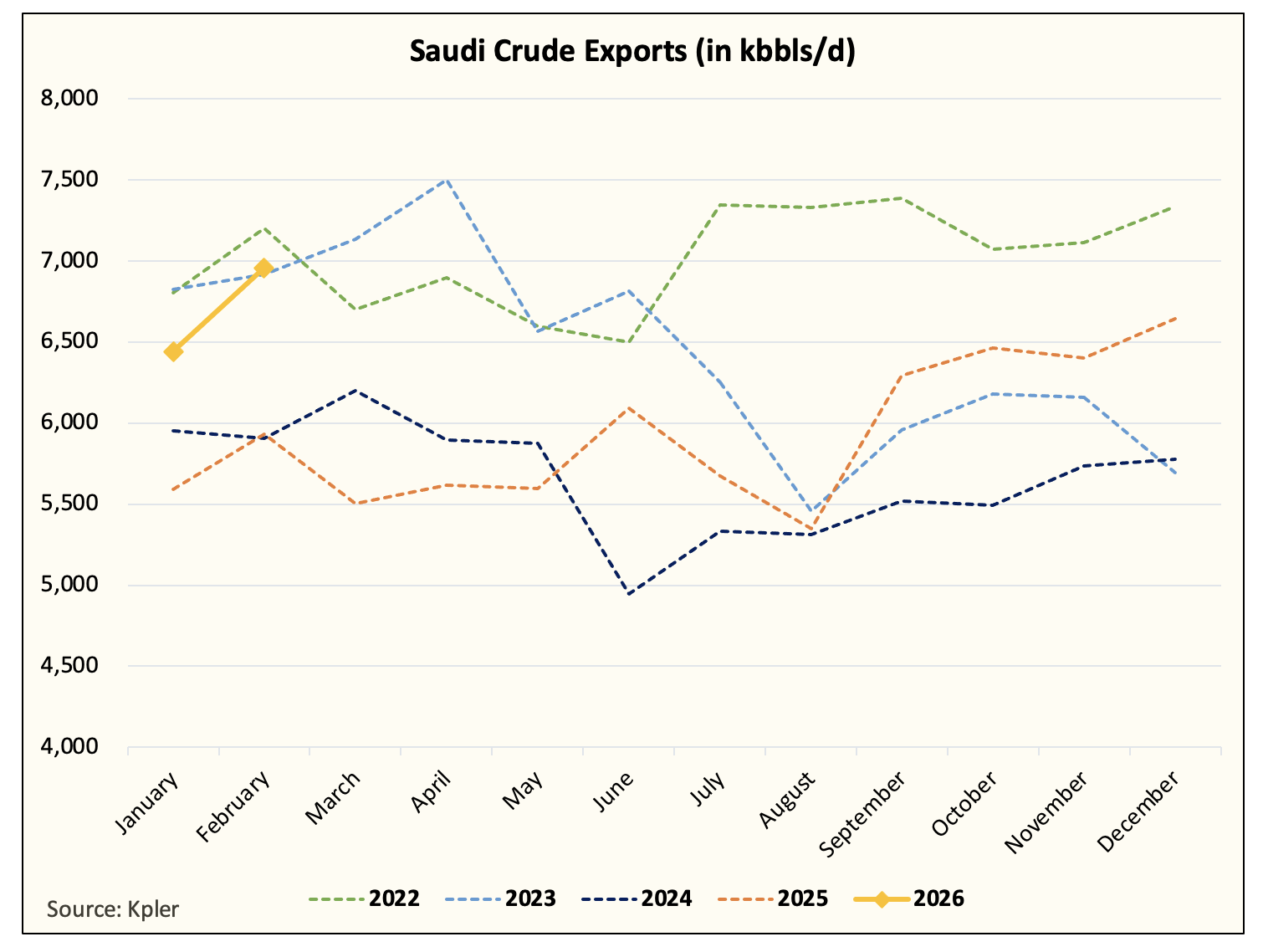

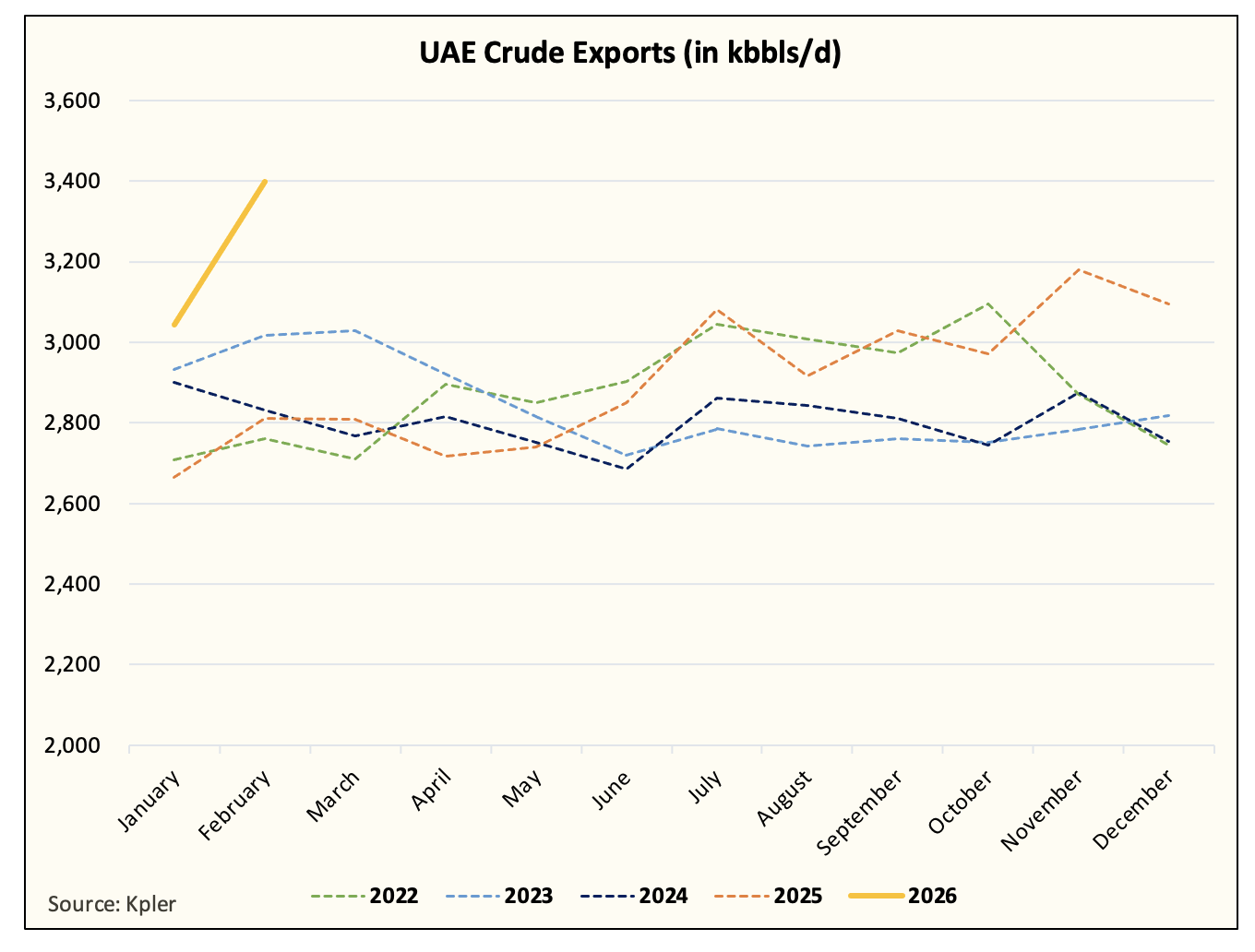

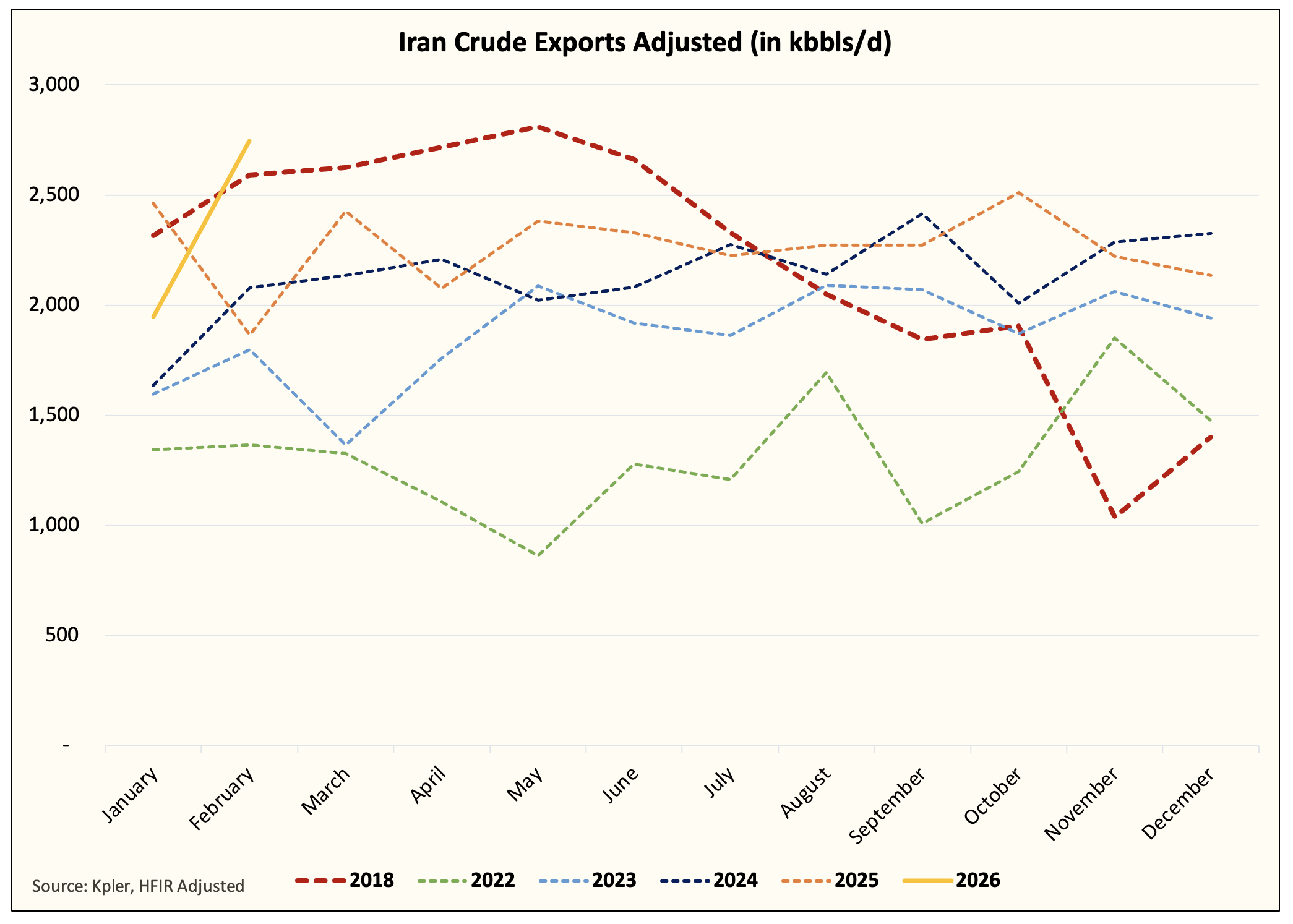

As frequent readers of our reports will know, we use crude exports to gauge a country’s real supply capacity. While some oil analysts argue that exports do not equate to production, we disagree, as the exported barrels are what the market perceives as supply.

In this sense, February tanker tracking data provided by Kpler is showing an obvious peaking signal. Saudi, UAE, and Iran are exporting near max capacity. Saudis can export an additional ~500k b/d to average ~7.5 million b/d, but for both UAE and Iran, we are at the max.

Saudi

UAE

Iran

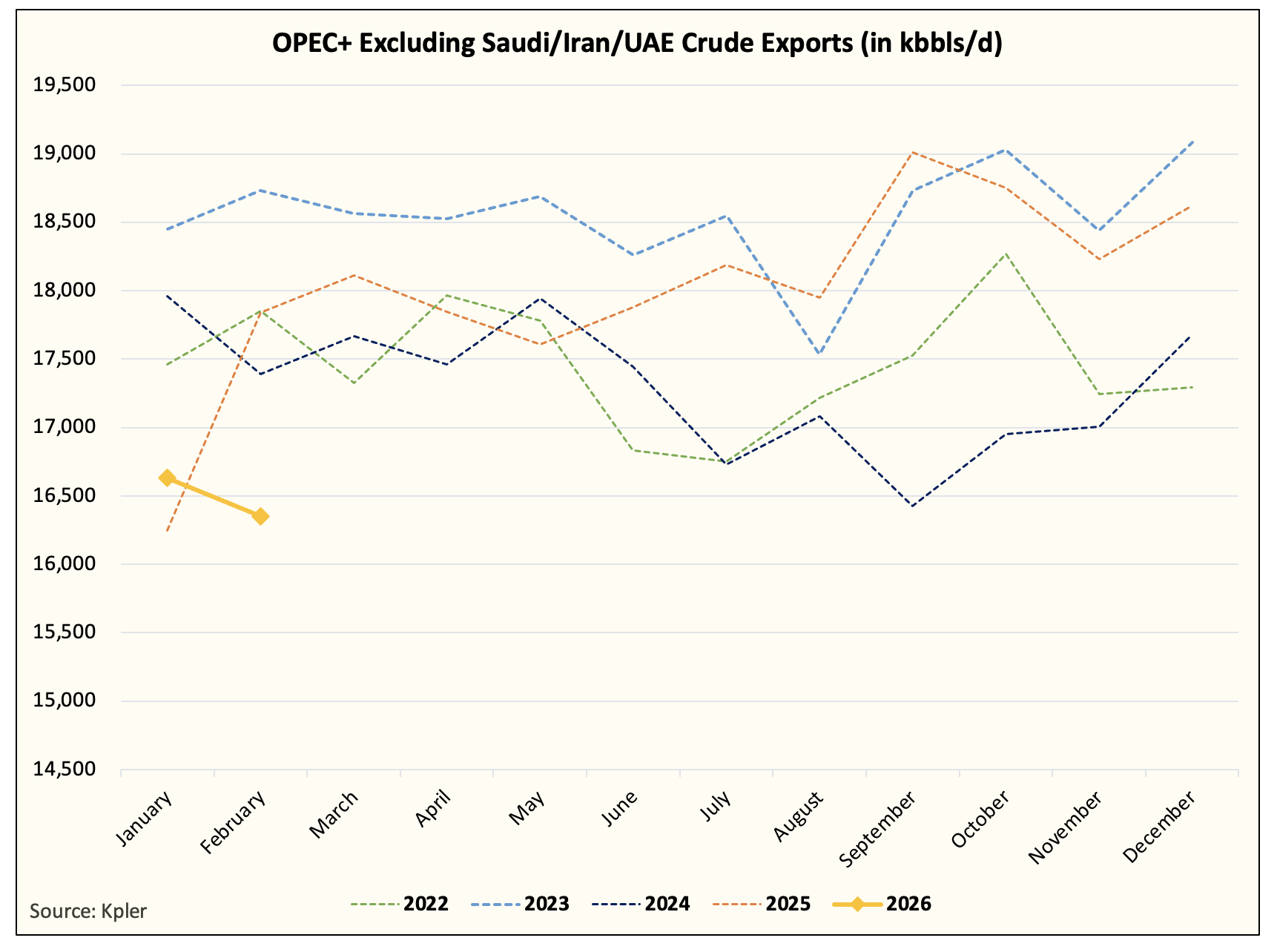

As for the other producers, exports have already maxed out in Q4 2025.

Excluding the UAE and Saudi, we won’t see any production increases from others. This is especially the case as we go into the summer power burn demand season where crude exports seasonally drift lower due to domestic consumption.