What's happening in the natural gas market today is not normal.

Let me clarify.

The August weather setup is not normal. The weather this month is expected to be so bearish that it will be the lowest cooling demand since 2017.

Source: CommodityWxGroup

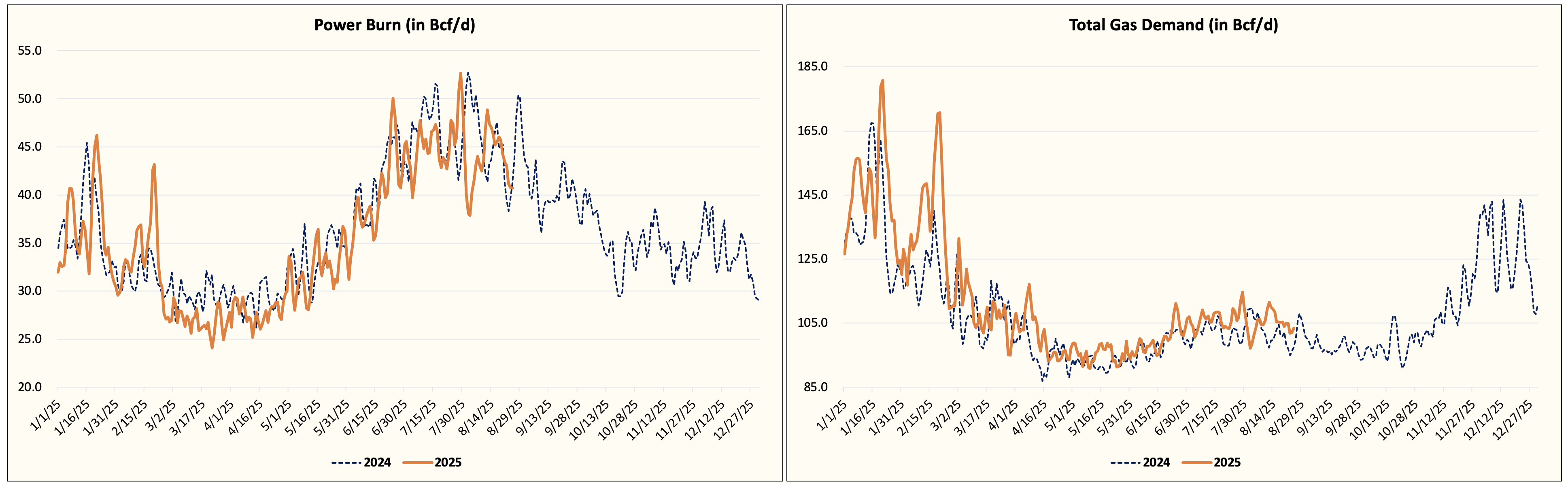

To put the power burn demand loss into perspective, from August 1 to 12, power burn demand was down ~7.3 Bcf/d y-o-y.

That's insane.

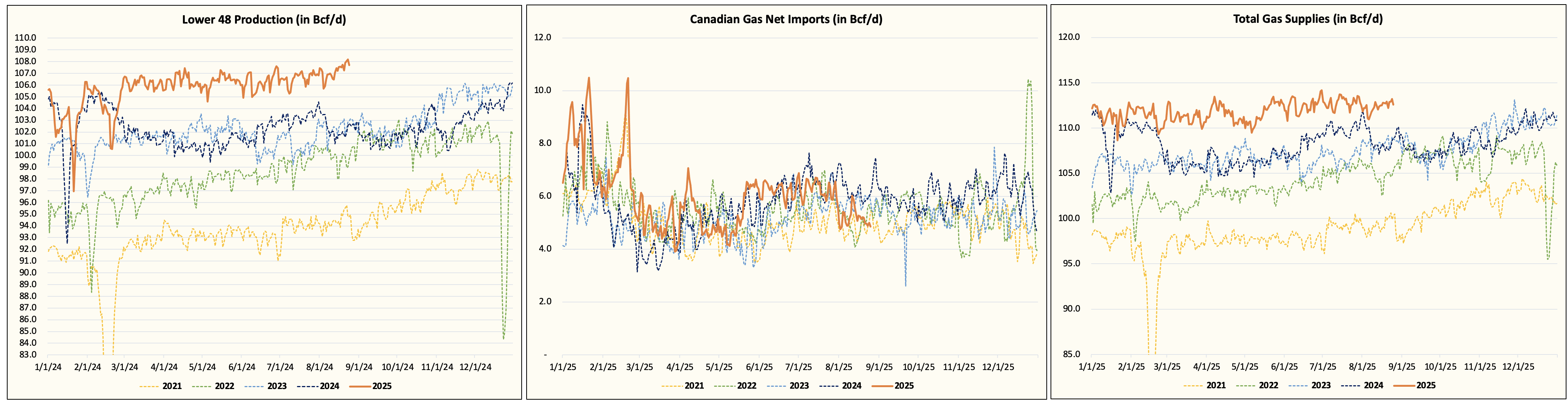

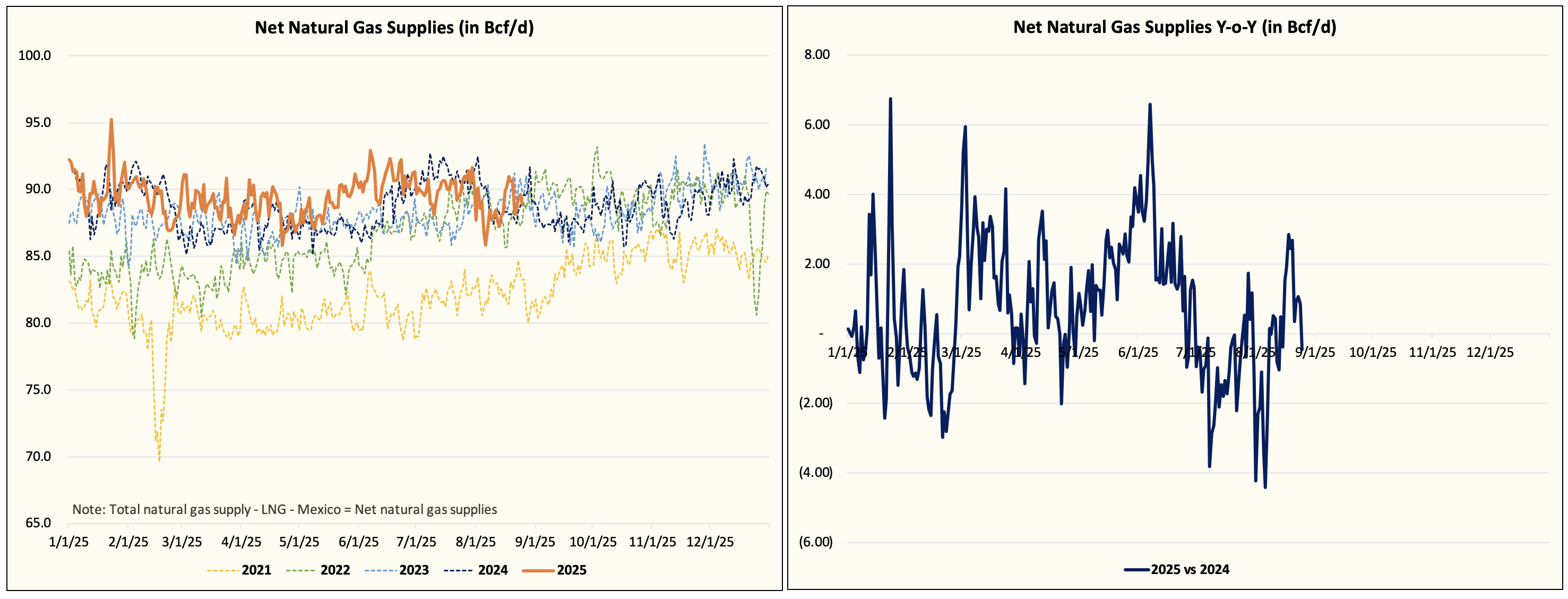

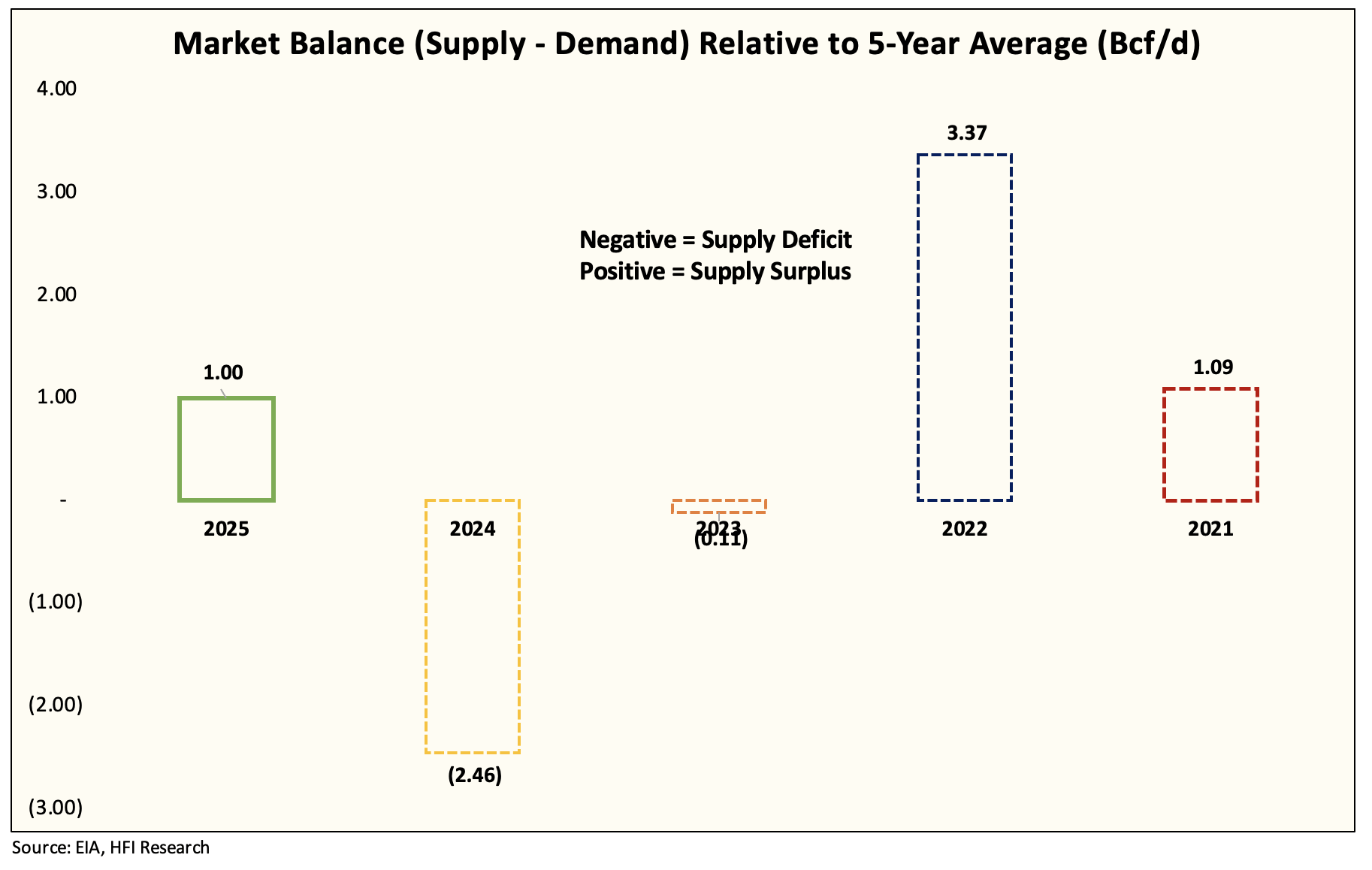

But what you will notice is that total demand remains above last year, thanks largely to the structural demand increases (LNG + Mexico). Total gas supplies are also higher year-over-year as production was impacted by low prices last year.

In aggregate, net gas supplies remain only slightly above last year (on average). As a result, the majority of the surplus we are seeing in gas storage is primarily due to lower power burn demand from the weather.

So what gives? Why are natural gas prices so low?

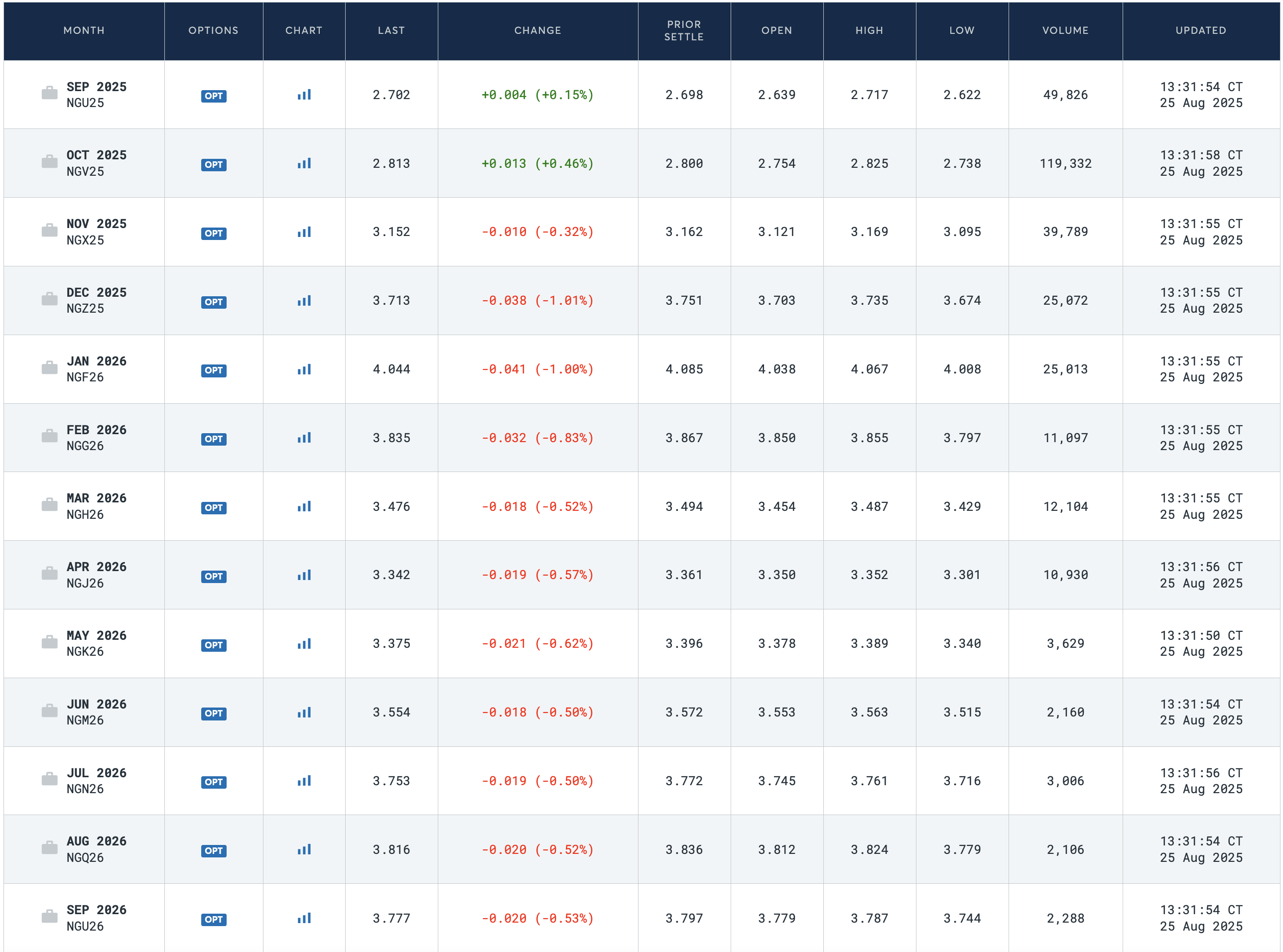

Source: CME

If you look at the futures curve, there's only 1 month above $4/MMBtu today (January 2026), and that's the heart of winter.

With +3 Bcf/d of gas demand coming online by year-end, I would think the market would be considerably more cautious than that.

As a result, is this one of those “obvious” moments where we invest more in natural gas names?

Yes, and I will explain why the market is being too apathetic about a price spike into 2026.

Price Spike

First, we need to understand why the market is so apathetic about potentially higher natural gas prices today.

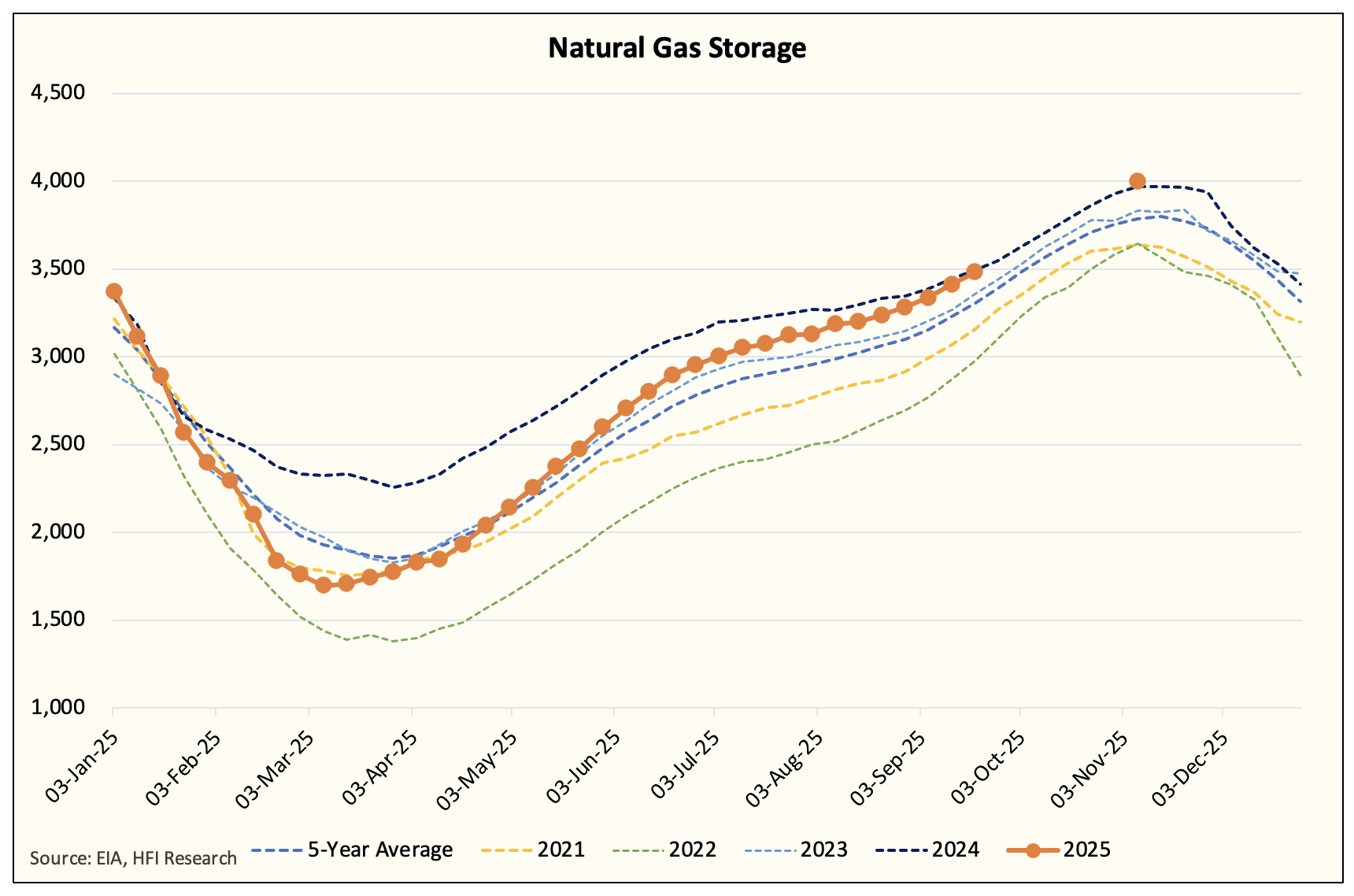

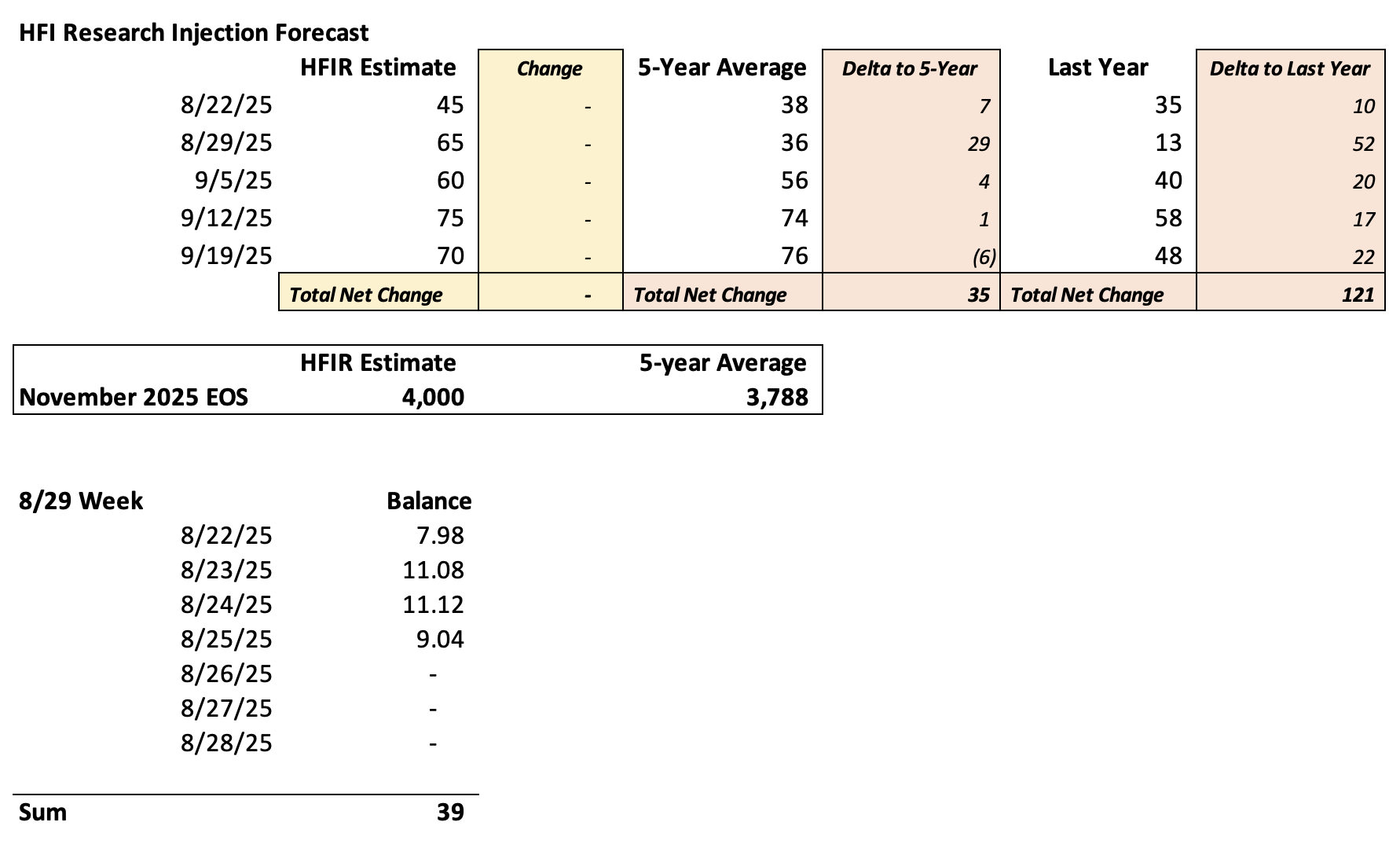

We can all thank the chart above for that. Natural gas storage is expected to surpass 4 Tcf by November, thanks to the incredibly bearish injections in August.

Over the next 5 reports, storage injections will be +121 Bcf higher than last year and +35 Bcf higher than the 5-year average.

This puts the oversupply at ~1 Bcf/d.

But as we've seen with winter heating demand months, the +212 Bcf of surplus in storage could easily be eliminated in the event of a bullish weather. All it takes is 1 cold blast, and the rest is history.

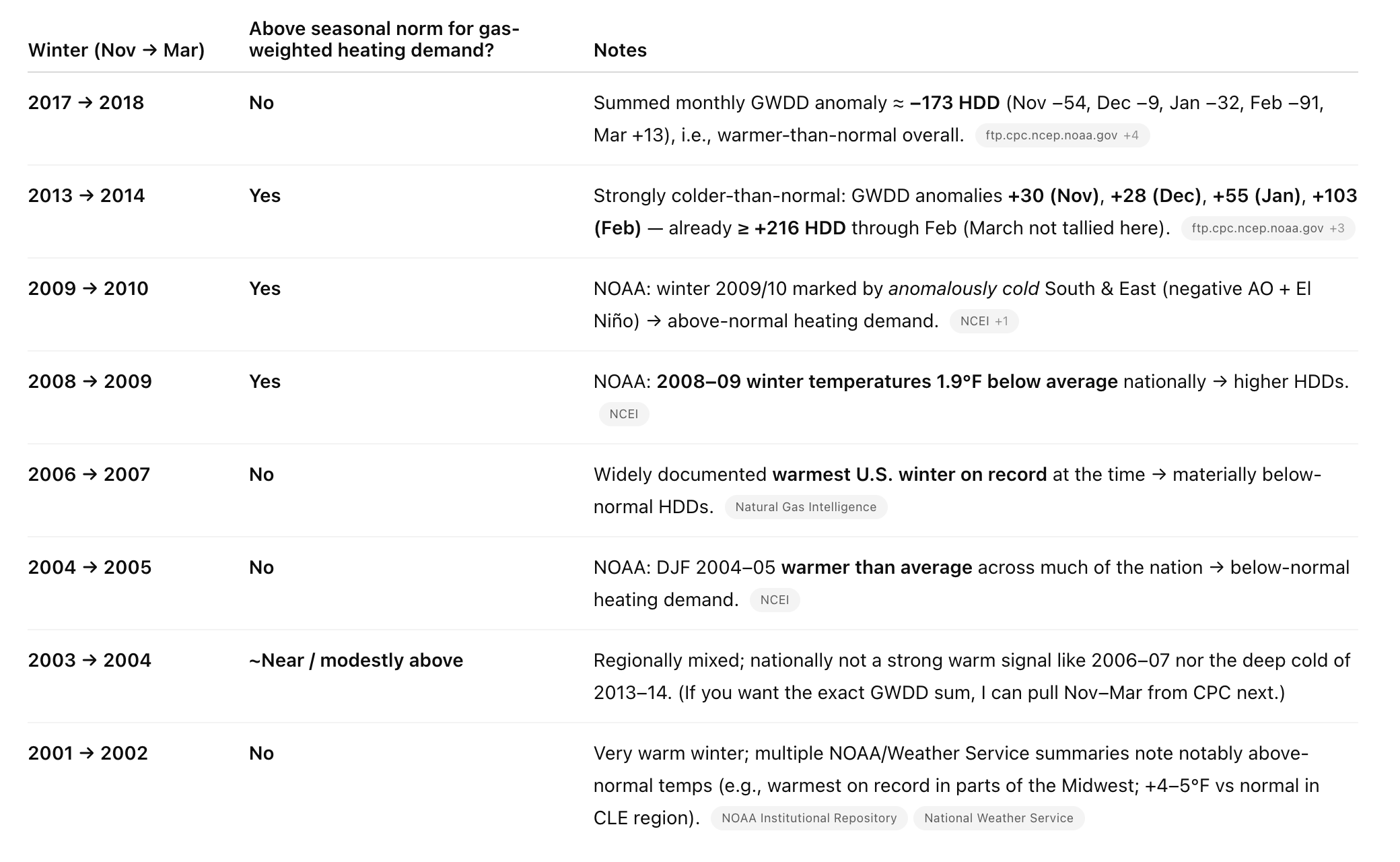

However, from the market's perspective, the probability of a colder-than-normal winter is a crapshoot.

In fact, here's an interesting datapoint.

Since 2000, every winter that followed a cooler-than-normal August resulted in a 50% probability that the following winter would be cooler than normal (thank you, ChatGPT).

So is there a reliable signal here? No, and that's the issue with weather forecasts. We won't know until we get there.

But what's the catalyst to spike natural gas prices higher?

Structural demand forces are increasing in the natural gas market. This is a certainty.

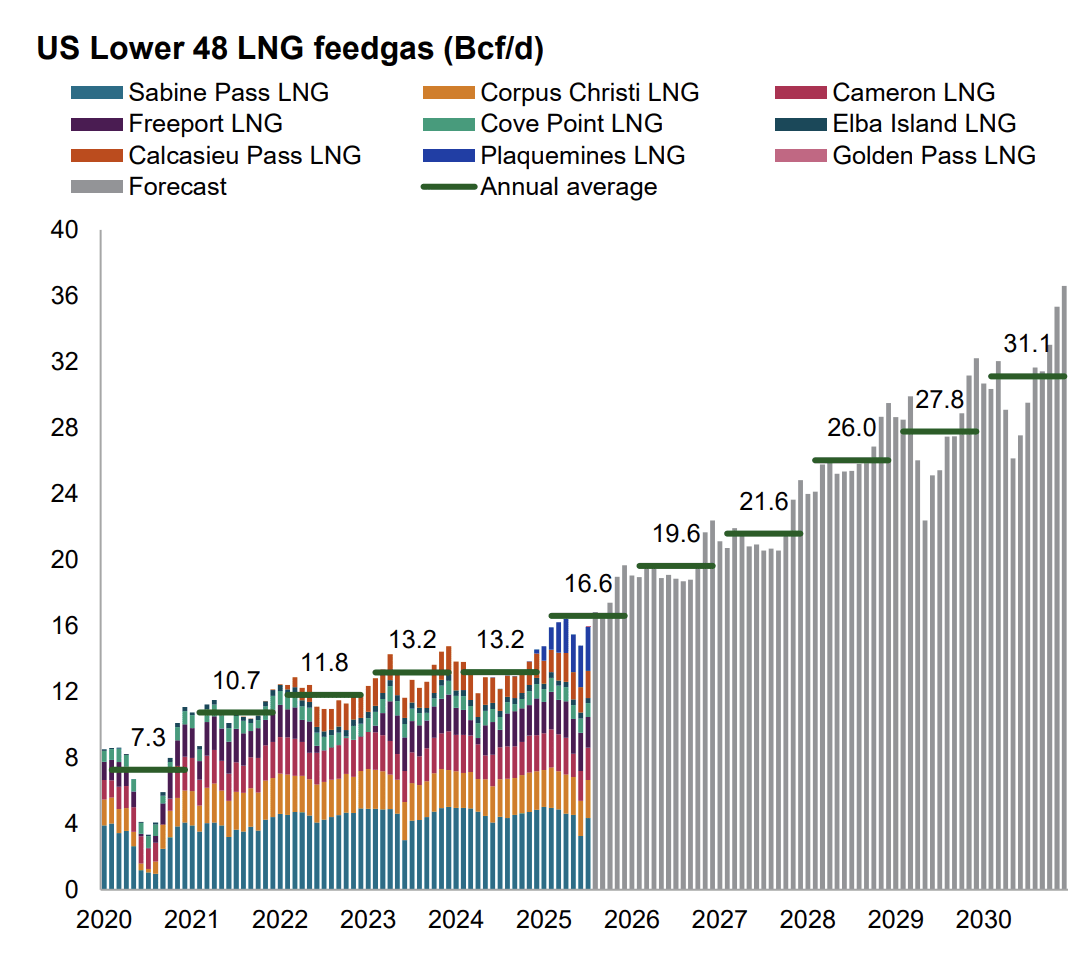

LNG

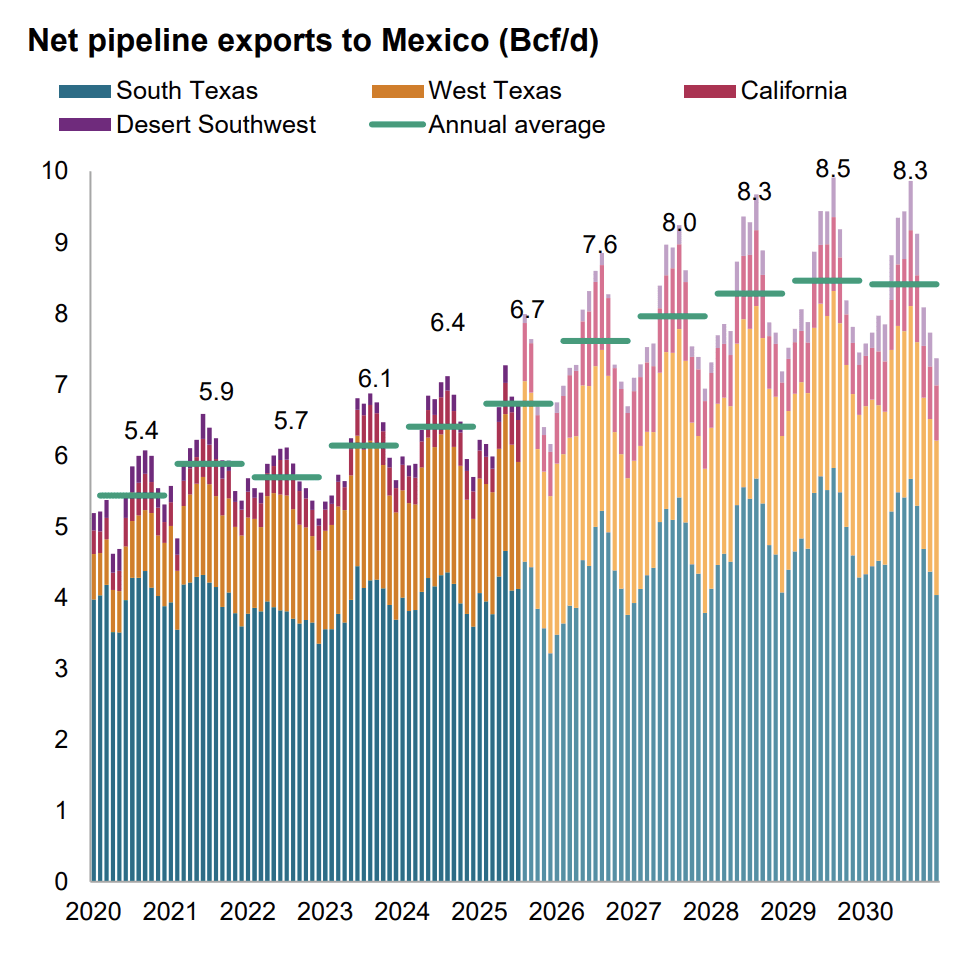

Mexico

Between LNG and Mexico gas exports, total structural demand will be +4 Bcf/d higher by this time next year.

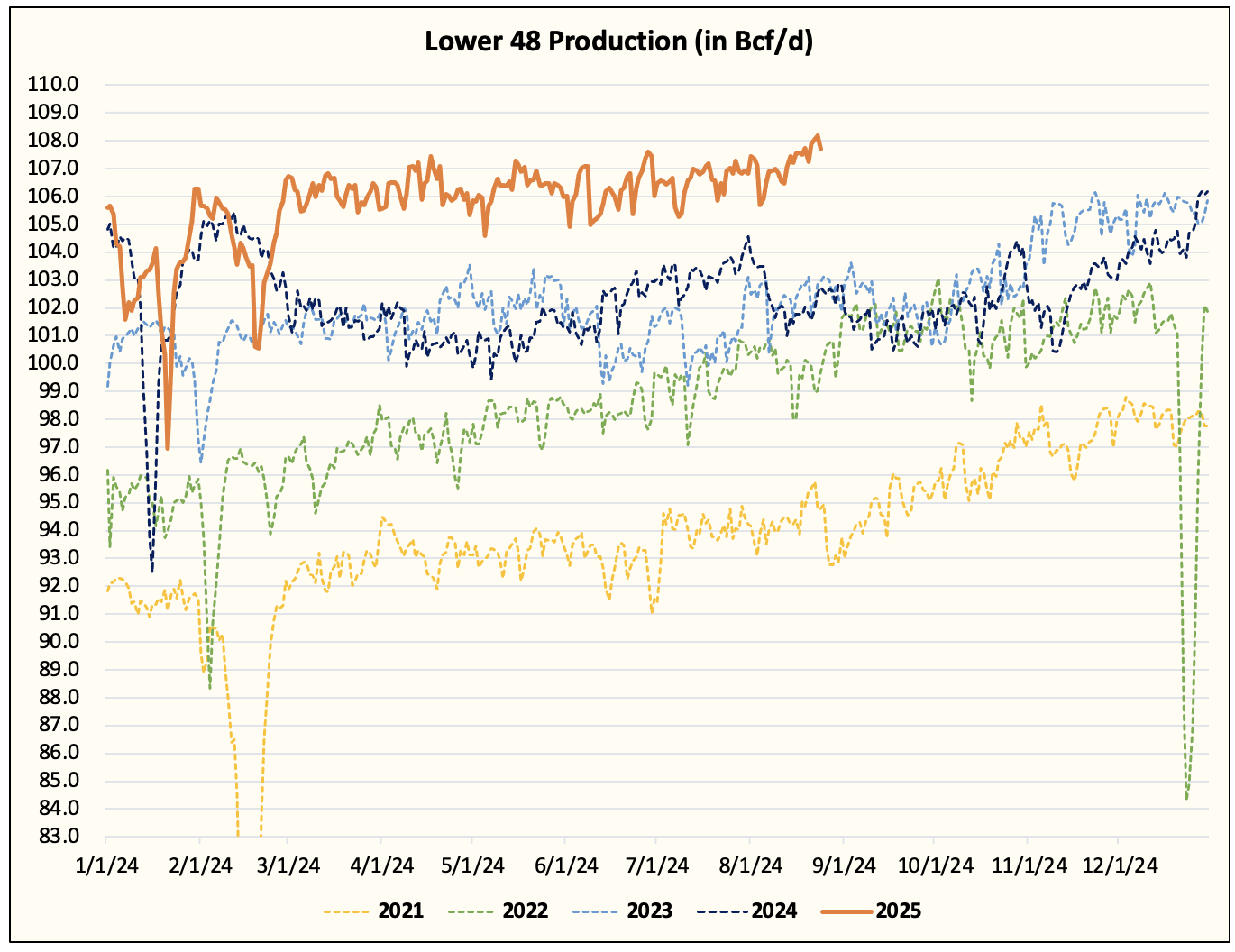

Lower 48 gas production will have to increase to ~111 Bcf/d to match that.

The issue?

Northeast and Permian gas production won't be able to match that in the next 12 months.

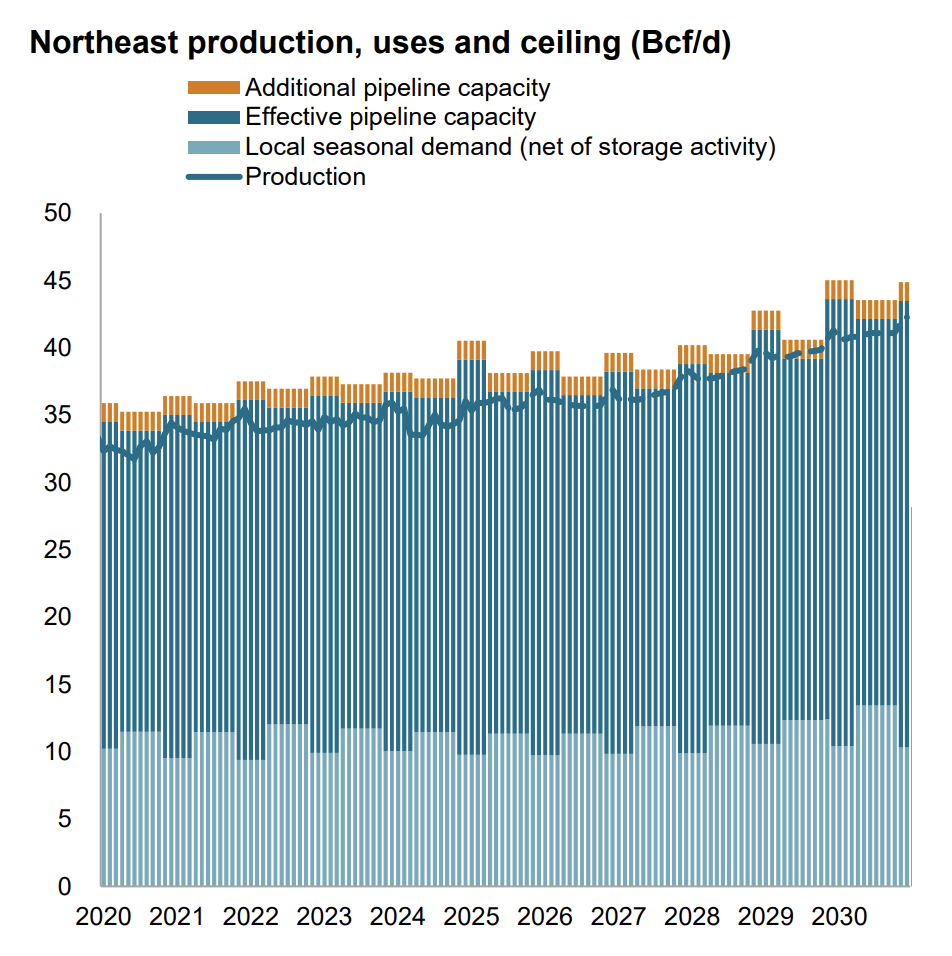

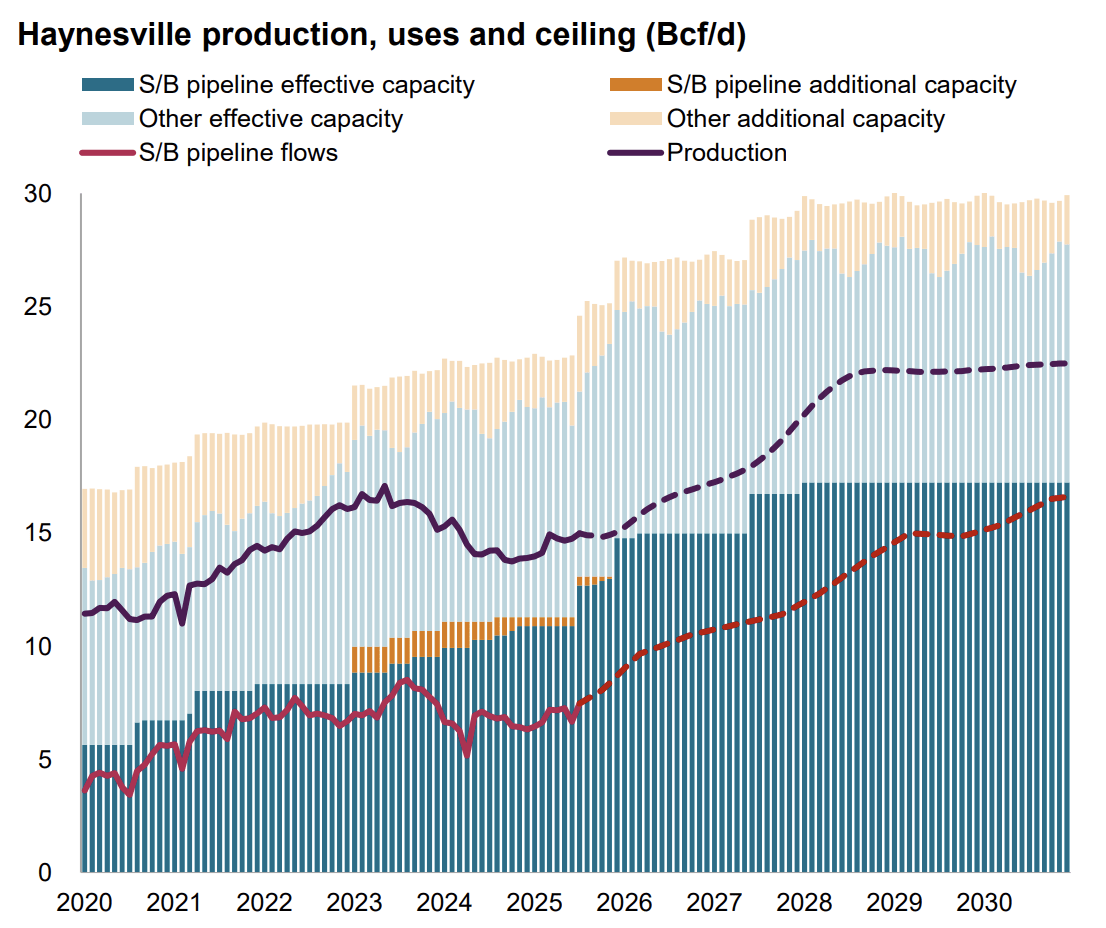

Northeast

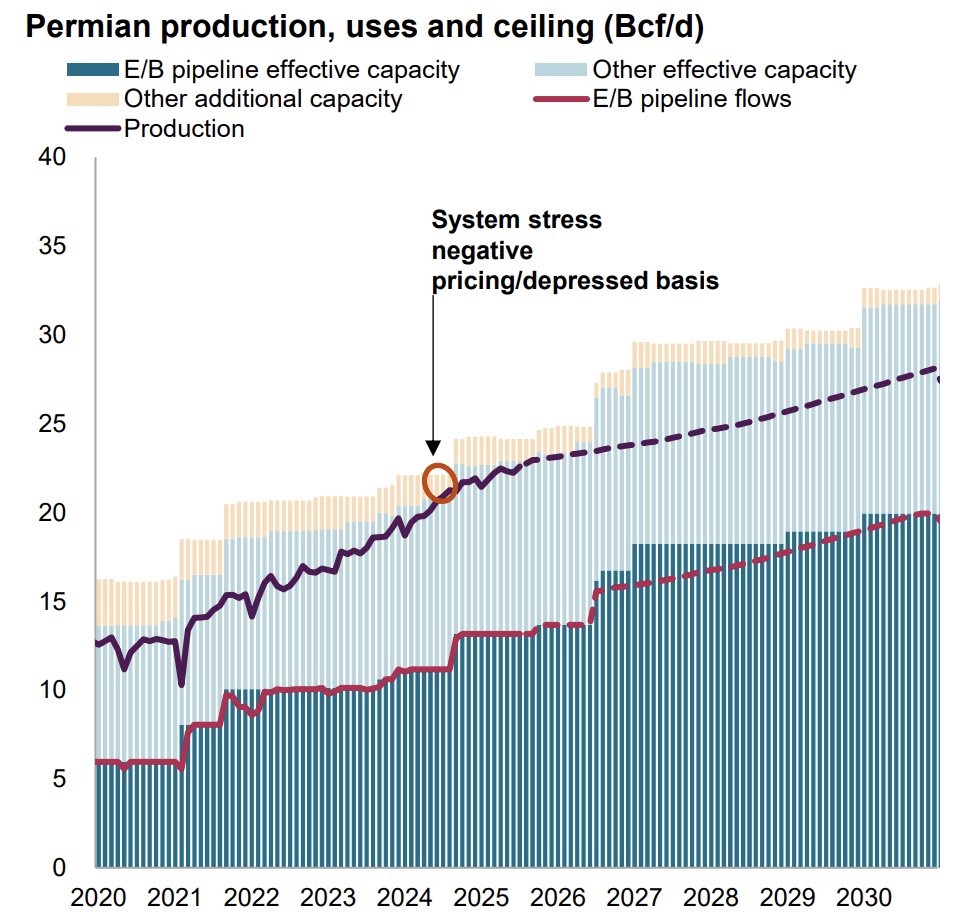

Permian

Both the Northeast and the Permian will face pipeline takeaway capacity constraints until late 2026.

For the other shale regions ex-Haynesville, there's not enough production velocity to meet ~4 Bcf/d of gas supply increase. This means the entirety of the production increase in the coming year will have to come from Haynesville if we are to avoid a mismatch.

And from everything we are seeing now, Haynesville has started to increase production, but we don't think it's at the pace of increasing ~4 Bcf/d by next year.

So even though the market is fixated on the elevated production level today (high ~107 Bcf/d), we are still well short of the production needed to meet the incoming increase in export demand.

This mismatch in timing, coupled with a false sense of belief that there's enough gas in storage, is what will create the recipe for a price spike in 2026.

In essence, because of the price drop we are seeing now, the probability of natural gas supplies surprising to the upside into 2026 is diminishing. With the demand variable as a 100% certainty and a reduced probability of more supplies, the outcome is becoming skewed to one side (price spike). All that needs to happen this winter is for heating demand to match the seasonal norm, and natural gas storage will finish April at 1.6 Tcf.

What happens... if?

Let's contemplate some scenarios here.

Let's first explore the bear case. What happens if the weather setup is very bearish this winter? What if heating demand matches that of the 2023-2024 winter (one of the warmest on record)?

Total storage withdrawal that winter was 1.55 Tcf.

LNG gas exports are going to increase by ~3 Bcf/d, and Lower 48 gas production will increase by ~1 Bcf/d. Delta is ~2 Bcf/d.

There are 22 weeks in the winter months, leaving the supply-demand mismatch at 308 Bcf.

This would put total storage withdrawal at 1.8 Tcf.

If we finish November gas storage at 4 Tcf, this would put April 2026 storage at 2.2 Tcf. This would be +330 Bcf higher than the 5-year average (1.87 Tcf).

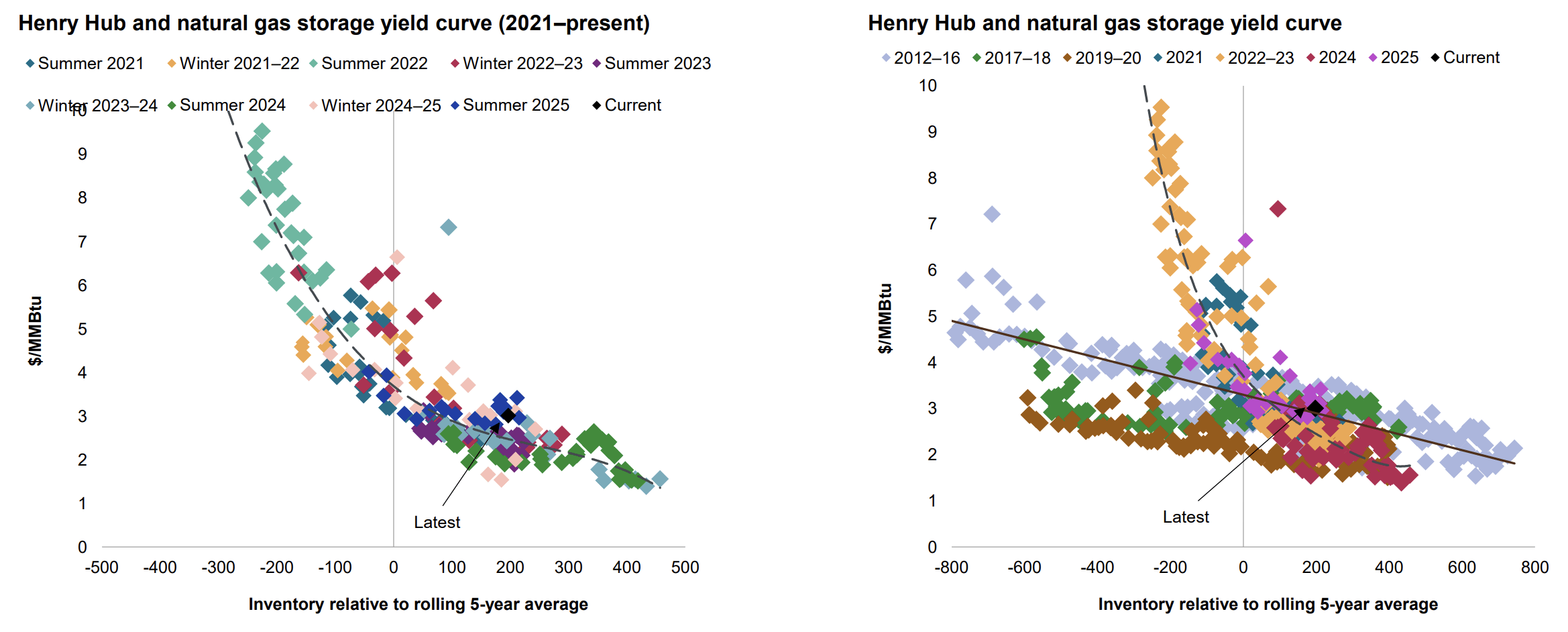

Now, if we use the 2021 to 2025 natural gas price curve, you can see that a +330 Bcf surplus would put natural gas prices in the low to mid $2/MMBtu range. If we are to use the historical yield curve (chart on the right), this would put natural gas prices around ~$3/MMBtu.

In essence, if the weather setup is very bearish, the downside scenario is between $2.5 to $3/MMBtu.

Conversely, if we have a normal winter (similar to the 2024-2025), total storage withdrawal is 2.132 Tcf.

Using the same supply-demand imbalance of 2 Bcf/d would increase total withdrawal to 2.44 Tcf.

This would put natural gas storage at 1.56 Tcf by April. This is -300 Bcf versus the 5-year average.

Using the 2021 to 2025 yield curve, this would translate into a price spike to $8 to $9/MMBtu! And if we are to use the historical yield curve (right chart), this would translate to a price target near $4/MMBtu.

In essence, in the event of normal to bullish weather, the upside is between $4 to $9/MMBtu.

But it doesn't end there. Here's where the math really gets crazy.

Because we will finish April at ~1.56 Tcf in storage, we will need to inject enough into gas storage to avoid another shortfall in the coming winter. Since we noted that Northeast and Permian gas production are largely capped until the end of 2026, most of the production increase will have to come from Haynesville.

Assuming that Lower 48 gas production manages to average ~110 Bcf/d for the next injection season (a tall task), this would still leave a deficit of ~1.5 Bcf/d during the injection season.

If we assume normal weather, this would translate to total injections of 1.935 Tcf. Now, if we add the 1.5 Bcf/d deficit, this would reduce total injections to 1.599 Tcf (36 weeks in injection season).

This would put natural gas storage by November 2026 at 3.159 Tcf!

Clearly, this is not a feasible scenario and something the natural gas market won't even contemplate testing.

In fact, even if you assume the bear case scenario of 2.2 Tcf, this would still only translate into a November gas storage of 3.799 Tcf or in line with the 5-year average.

So yes, the risk is skewed asymmetrically to the upside!

Buying...

We are now fully allocated in the HFIR Natural Gas Portfolio. We issued a trade alert today notifying readers of all the names we added.

We don't want to buy the dip in natural gas futures yet due to the contango in the curve, but we think the market is once again mispricing what's going to happen to fundamentals going into 2026.

Conclusion

The market is weighing the near-term bearishness too heavily. As we explained in this article, the risks are skewed to the upside because of the incoming demand increase. The only variable that can ruin the natural gas bull thesis is if natural gas production meaningfully surprises to the upside by year-end (~110 Bcf/d). Anything below this level implies that fundamental balances will be much tighter than what we saw coming into 2025.

We are now fully positioned for what we see coming.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of HFIR NATURAL GAS PORTFOLIO either through stock ownership, options, or other derivatives.