(WCTW) The Only Certainties

Amidst all this chaos. Our latest thoughts on the oil and natural gas market.

I was reluctant to write anything tariff-related at the start of this week because I wanted to see how this drama unfolded, and I'm glad I did.

Overnight, it became evident that the US and China wouldn't give in, but that left open the question of the ridiculous mathematical formula for reciprocal tariffs on the rest of the world.

Thankfully, cooler heads prevailed. President Trump announced via a post today that he has increased tariffs on China to 125% while imposing a 90-day pause on reciprocal tariffs on the rest of the world (with a minimum of 10% being imposed).

As of this writing, everything is massively higher because of the relief that the tariff war is over... for now.

The only certainties amidst the uncertainties

"The Battle of the Cabinet"

But even with the 90-day pause, this tariff saga is far from over. There is a deep fundamental misunderstanding from the Trump administration with regard to trade imbalance and tariffs.

Both Navarro and Lutnick seem to be incapable of understanding just how exactly tariffs work and are instead proposing them as a long-term solution to US trade imbalances. While Bessent and Musk appear to be urging Trump to use tariffs as a form of negotiation tool rather than a weapon.

There are three certainties out of what I've seen in the last week:

Either Navarro and Lutnick are both fired, and we can rest assured that a more diplomatic trade negotiation approach is pursued.

Or Musk and Bessent are out, which pretext even more chaos ahead.

The last option is for Congress to take away the tariff-mandating power of the President. This is going to be an arduous task and one that will take months.

If Navarro and Lutnick end up winning the "battle of the cabinet", then you should expect full-blown chaos for financial markets for the coming years. But if logic prevails, as it usually does, then Bessent and Musk will win, which will imply a calmer environment going forward.

The best case scenario is for Congress to do its job and take away the tariff-mandating power. In my view, this will gain more traction over the coming months.

US shale will decline

The second certainty amidst all of this nonsense is that US shale oil producers will reduce capex in the near term. The current whipsaw we are seeing in the oil market will imply meaningfully lower US crude oil production going forward.

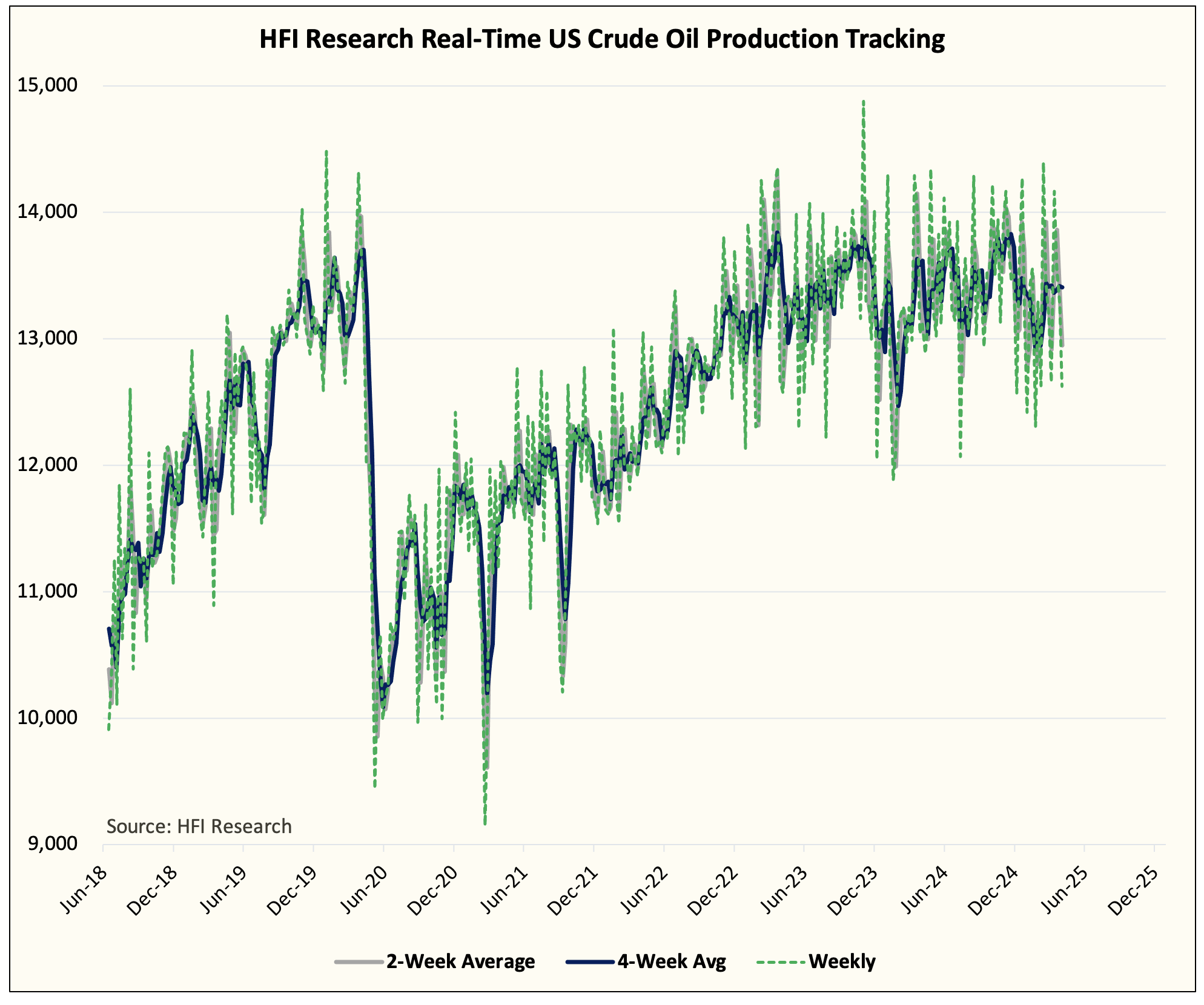

Using the latest real-time US crude oil production data, we are seeing an average close to ~13 million b/d, with this week's production coming in at ~12.5 million b/d.

With WTI trading around $63/bbl, we will not see US oil producers shut-in production, but we will certainly see delays in drilling and completion. This has the impact of allowing base production to decline (natural base decline), which is sizable.

We estimate that US crude oil production would decline ~225k b/d per month if producers throttle completion activities. At $60/bbl WTI, US crude oil production will average ~12.7 million b/d in Q2 2025 vs the consensus estimate for ~13.65 million b/d.

The -950k b/d delta will contribute meaningfully to global oil market balances.