(WCTW) The Risk Is To The Upside

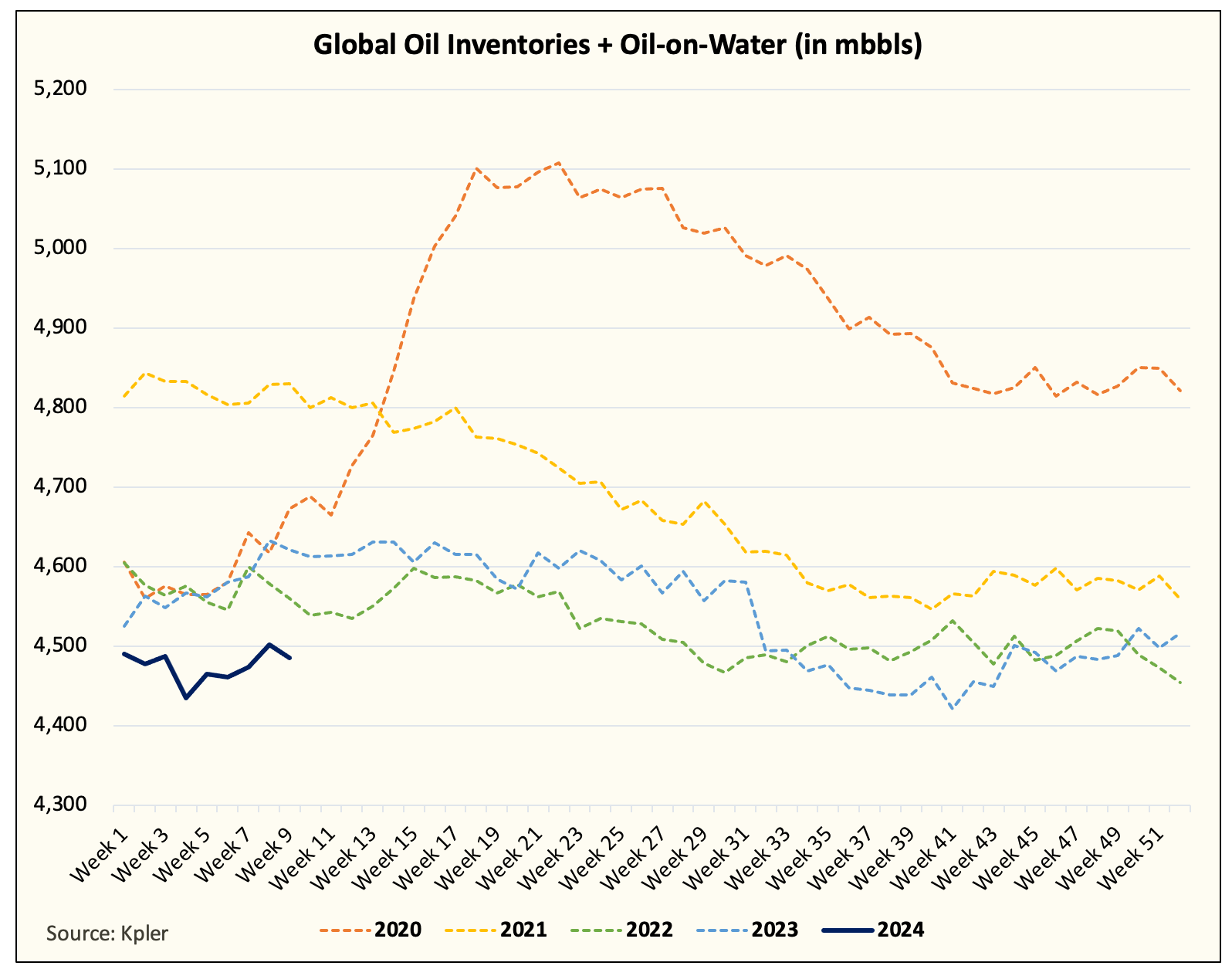

Coming into 2024, the consensus was skeptical that the OPEC+ voluntary cuts were going to push balances to the deficit. And with Q1 coming to an end, it's safe to say that balances have so far surprised to the upside.

What's particularly interesting about balances is that if you look at OPEC+ crude exports, we have not seen any meaningful decrease, which suggests that it's not a real cut (except for the Saudis, we have detailed this in this report).

In Q4 2023, OPEC+ crude exports averaged 28.811 million b/d. So far in Q1 2024, the average is 28.86 million b/d. Asking for a friend here, is this a cut?

While it's fair to point out that y-o-y, OPEC+ crude exports are down ~700k b/d, the entirety of the cut comes from the Saudis. Some are beginning to question if this cut is sustainable given the unilateral nature of it. The reality is that if we know the rest of OPEC+ is not cutting and the Saudis can single-handedly flip balances from deficit to surplus, then we know the Saudis are in control (i.e. sustainable). It's when there are upside supply risks from within OPEC+ that make the unilateral nature of the cut unsustainable (i.e. Iraq or Iran wanting to boost production, etc).