(WCTW) What To Make Of The Current Geopolitical Situation (Israel) And What It Means For Oil?

First and foremost, the situation in both Israel and Gaza is horrible beyond our wildest imagination. This article is not about politics, and it will not focus on what's right or wrong. Instead, we will do our best to think through what this means for oil market supply and demand, and how readers can use it to manage their portfolio/trading positions.

Geopolitical Risk Premium

WTI and Brent, as of this writing, are up ~3% with WTI trading above $85 and Brent above $87. Initially, at the close of Friday, WSJ published a report noting that the US is close to finalizing a megadeal between Saudi and Israel. It even contained a quote stating that the Saudis may increase production by early 2024 if prices are too high. Soon after, Hamas militants launched a surprise attack on Israel. If you want to thoroughly review the events, please read this article.

Some of you may wonder, what does this have to do with oil? Historically speaking, geopolitical risk premiums are usually embedded into the price of oil in case of supply disruptions. In this case, Israel is not a major oil producer, so what's the catch? The catch, in our view, has to do with Iran's potential involvement in this whole ordeal. WSJ published a piece noting that Iran's senior officials helped plan this attack months ago.

While the US has not condemned Iran or associated Iran in any way with these attacks just yet, it does make you wonder what this means in terms of oil sanctions on Iran.

Source: IEA

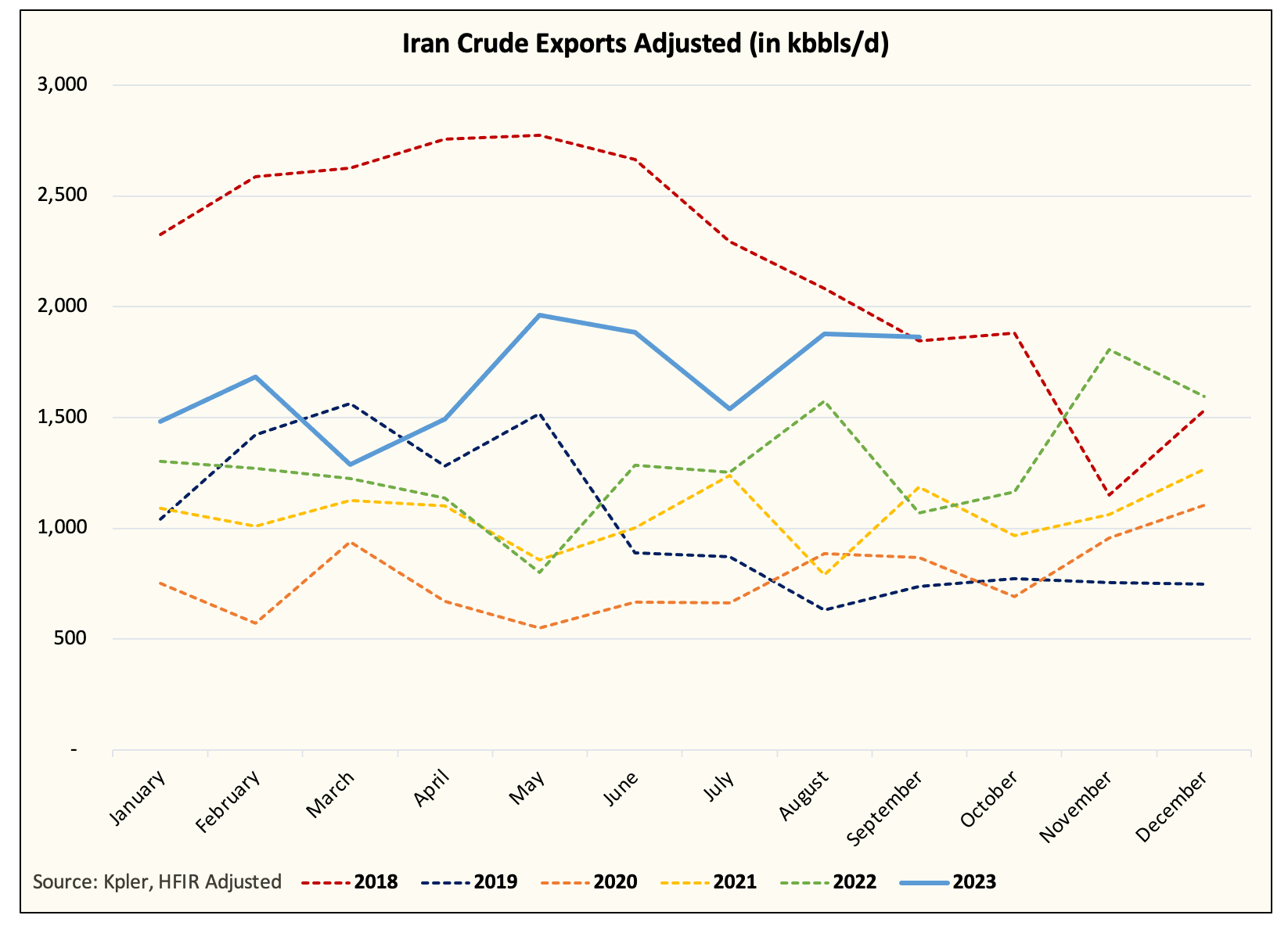

For starters, we need context to what we are writing. In June, we published a report noting that Iran is already back in the oil market. Since then, IEA has confirmed via its figures that Iran's oil production is close to ~3.1 million b/d. Our supply & demand model assumes ~3.3 million b/d, and official Iranian figures support that production is around ~3.3 million b/d.

Putting all of this together, Iran is exporting close to ~2 million b/d. Visible tanker exports account for ~1.5 to ~1.6 million b/d, while shadow exports account for ~400k b/d.

Since H2 2022, the Biden administration has turned a blind eye to Iranian crude exports. As we wrote earlier in the year, this was most notable in the rapid decline in Iranian floating storage.

With floating storage gone and crude exports back to ~2 million b/d (~500 to ~800k b/d below the previous peak), what's the chance that Iranian crude exports drop going forward? Perhaps the US does nothing and leaves Iran as is, but what probability would we assign to that?

In my view, while the risk of a major loss is low, we think Iranian crude exports would move lower in the following months. We think the average would fall from ~2 million b/d to ~1.6 million b/d. In terms of visible tankers, this means Iran's crude exports would drop closer to ~1.2 million b/d.

While it won't be much of a decline, it will be compounded by the fact that Saudi and Russia will continue with their voluntary cuts into year-end and possibly well into H1 2024.