This time is certainly different. Unlike the previous two conflicts between the US/Israel and Iran (April 2024 & June 2025), tanker traffic was never impacted.

This time around? Nothing. No movement.

The Strait of Hormuz hasn’t seen traffic trickle to a halt since... ever.

The closest historical analogs are:

1980s Tanker War (Iran-Iraq war): Traffic never ground to a halt.

1987-1988 Mine Episodes: Logistic jam, but never to a halt.

2019 Tanker Attacks in the Strait: No disruptions.

So yes, we are entering unprecedented territory. Rightfully so, the global energy markets do not know how to react to this appropriately. In this piece, I will explain the fundamental backdrop and the things that are preventing an oil price spike. I will also extrapolate the possibility of what it means to the global energy market if tanker flows remain depressed for longer than a week.

The Backdrop

Shipping

Source: Marine Traffic

Here is the latest tanker traffic data from Marine Traffic. Tanker flow is effectively zero. As Kpler noted in its blog post over the weekend, while the Strait of Hormuz is “technically” open, the lack of insurance coverage is making it very difficult to move vessels through the Strait.

Oil prices fell yesterday when the Trump Administration said it had directed the DFC (US International Development Finance Corporation) to offer political risk insurance and financial guarantees. Following the announcement, industry participants remained skeptical of the scale of the backstop. For starters, industry participants are confused as to what is covered, under what terms, and how fast. In a piece covered by FT today titled, “Gulf insurance costs soar 12-fold despite Trump guarantee.” It said:

London insurers were racing on Wednesday to understand how the proposal might work and whether it could help bring down prices. Several of the world’s largest insurance brokers said they were blindsided by Trump’s announcement.

“We’ve heard absolutely nothing more, other than that Truth Social statement,” said David Smith of specialist broker McGill, adding that insurers were unsure how broadly the support would apply, despite the pledge to insure “all” trade through the Gulf.

“Would it apply, for example, to a cargo of Chinese oil carried on a European tanker?” Smith said. “We don’t know.”

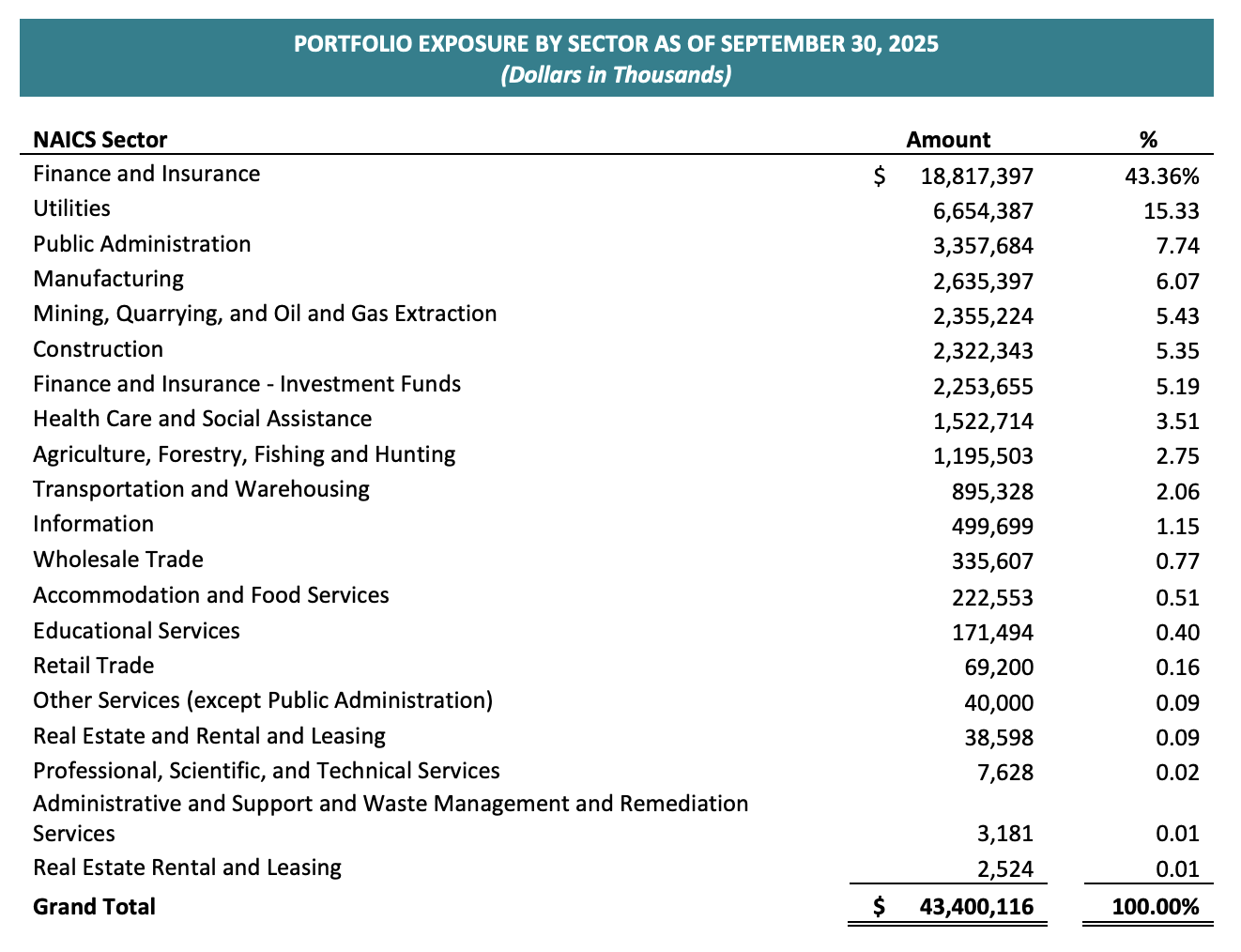

The other issue that the DFC will likely run into is the funding aspect. The current DFC Maximum Contingent Liability (MCL) cap is $205 billion.

Source: DFC

As of September 30, 2025, DFC had exposure on $43.4 billion. That leaves room for ~$160 billion. JPM estimated that there are currently 329 vessels operating in the Persian Gulf. If each ship required pollution, salvage, hull, and third-party liability insurance, this implies $352 billion of maximum insurance coverage.

To fund the difference, it would require Congressional action, which would require at a minimum 3-10 days. Obviously, DFC does not need to insure the entire exposure right away, but the timing delay is something we will analyze more later.

Finally, the Trump Administration said that it will use the Navy to help escort the tankers. This has been done in the past. Operation Earnest Will (1987-1988) saw the US reflag Kuwaiti tankers and escort convoys. Over the span of 14 months, there were 127 convoys/259 ships. In addition, Europe supported the minesweeping side. Even with protection + minesweeping, there will still be risk.

Oil Storage

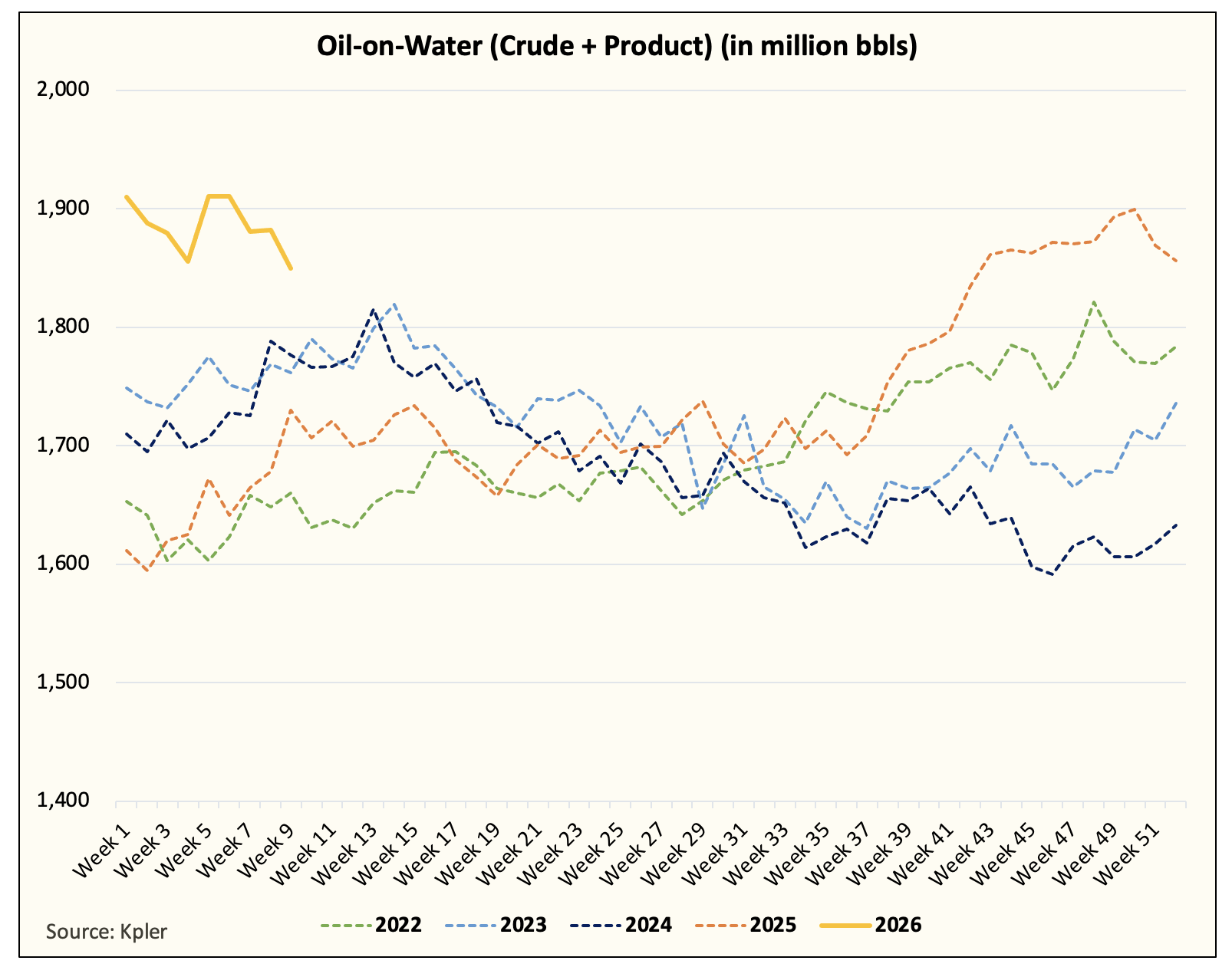

Q1 is seasonally the lowest oil demand quarter. We are also entering peak refinery maintenance season. Luckily for the global economy, we have an abundance of oil-on-water thanks to the sanctions imposed on Russia late last year.

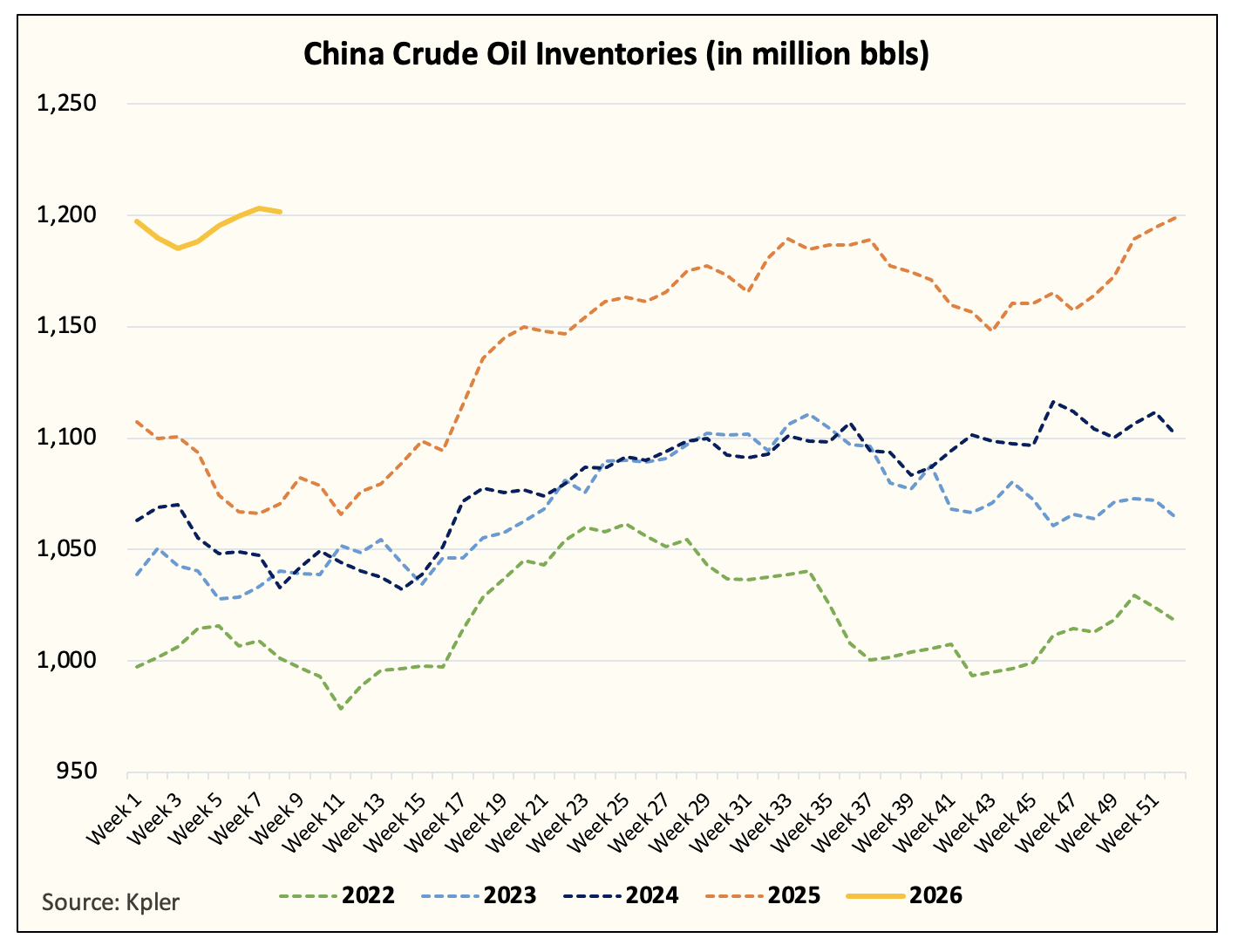

China has been relentlessly buying crude, and the current cushion gives them breathing room for 2-3 months.

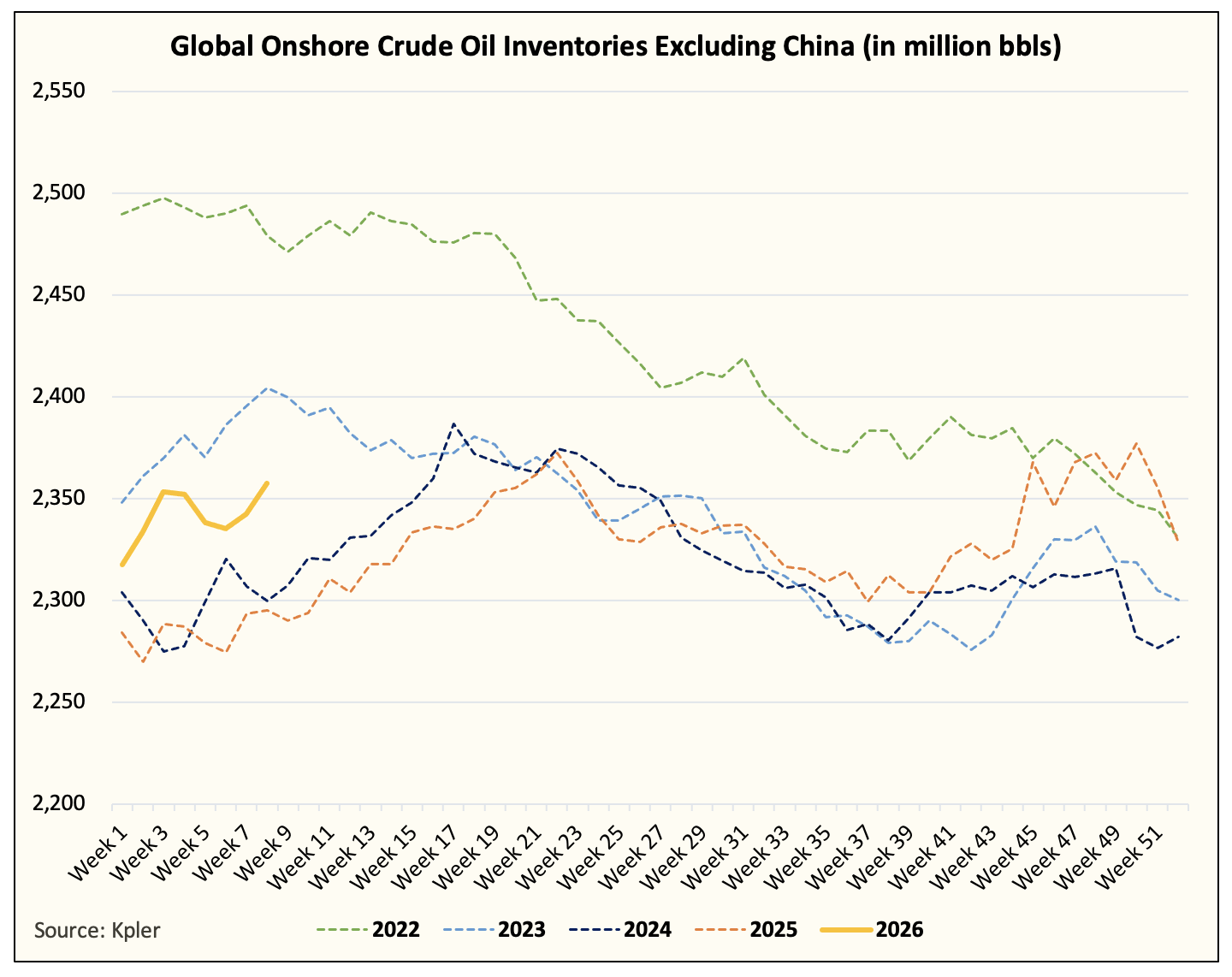

Meanwhile, the rest of the world isn’t so fortunate.

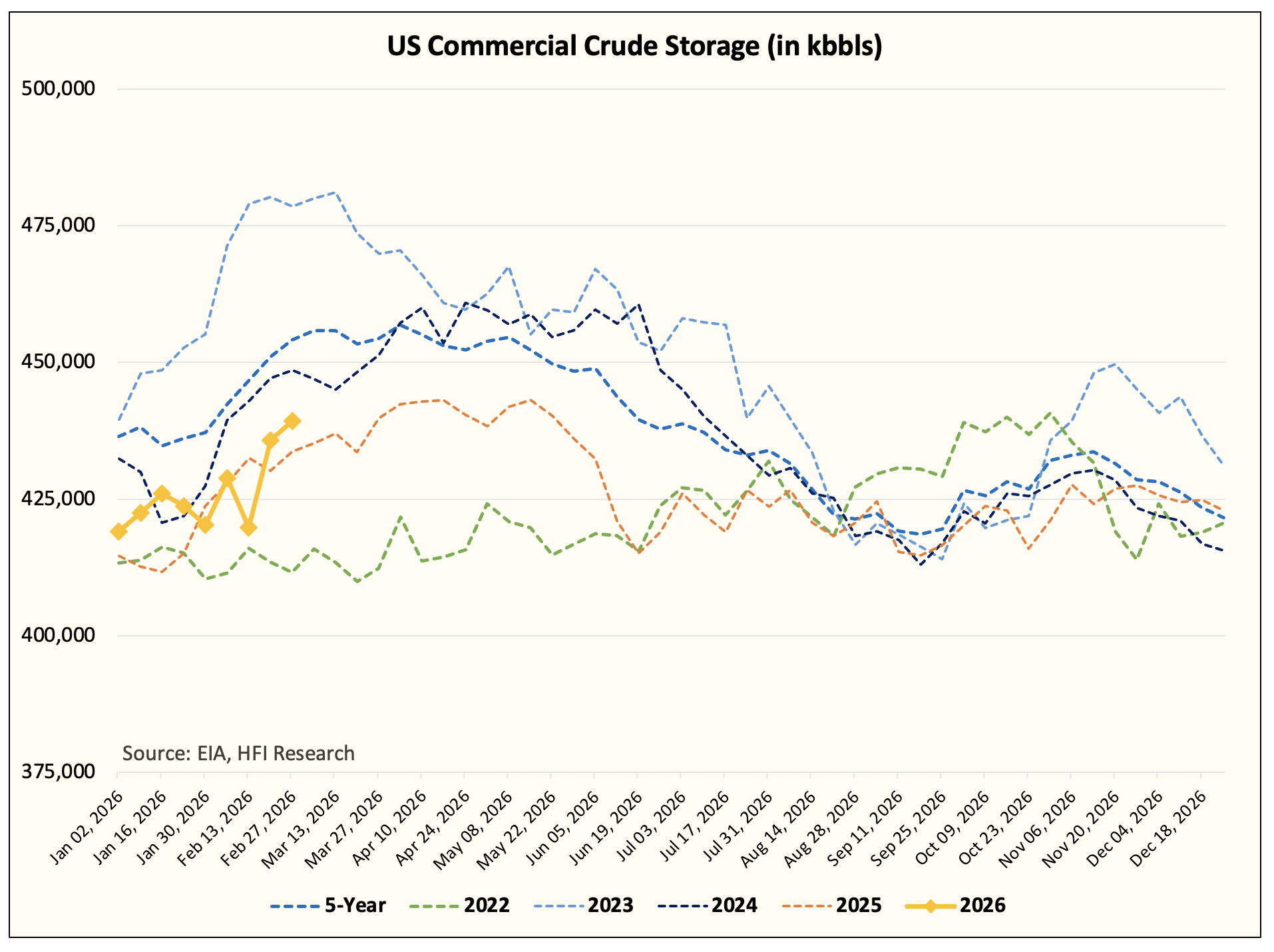

Onshore crude oil storage is only slightly higher than last year, so the absorption cushion is low.

The US does not import the same level of crude from the Middle East as a decade ago. With Canadian and Venezuelan crude serving as the source for the heavy barrels, the pull on US crude will remain elevated until the disruptions end. This should pressure US commercial crude storage lower and keep WTI timespreads backwardated.

How much storage do we have before the market starts to panic?

Well, here’s the math: