We Are 'Still' Going Full Speed Into The Wall

Product storage is about to get tighter unless China steps in and lifts the product export ban. If it does, expect a meaningful reversal in crude.

Please read part 1 of the report.

“Dude, you must be crazy.”

I probably am, but we are still going full speed into the wall. Yes, WTI is barely hanging on to $70 for its dear life, but please remember that consumers use petroleum products like gasoline and diesel; they don’t use crude oil. Refineries do, and this is why it was always important for us to pay attention to crack spreads along with crude timespreads.

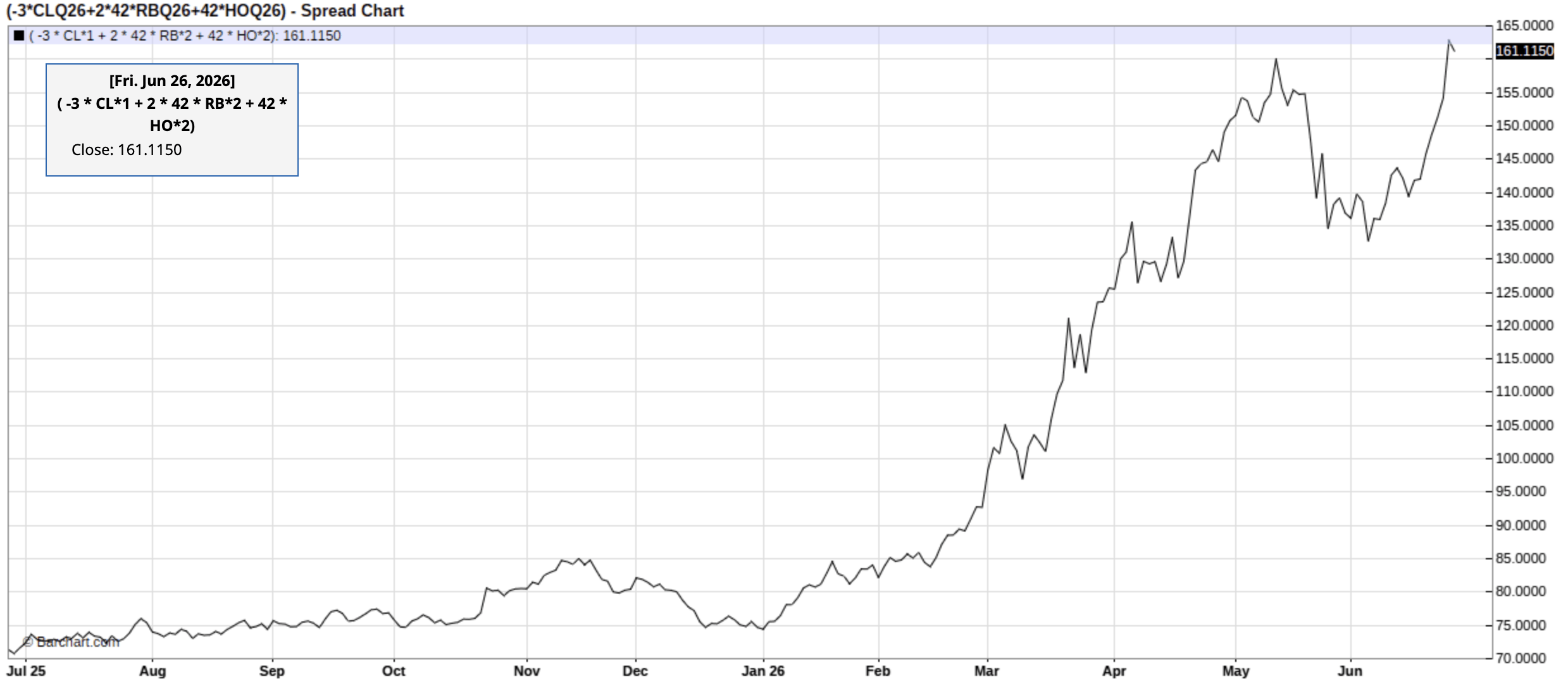

Note: Please divide it by 3.

The fever in the market today is that crude is oversupplied, but products are undersupplied. How can this be possible?

Well, China’s June crude import data so far is -4.7 million b/d y-o-y, and teapot refineries are operating at 50% utilization. Compared to US refineries operating at 95% and PADD 2 refineries operating over 100%, you can see where the disconnect is.

But here’s the thing. If end-user demand isn’t down and you still have a production shut-in of ~8 million b/d, you are losing barrels in one form or another. Yes, China might not be importing crude, but it is drawing down product inventory. No one has visibility into how much China has in products right now, but it can’t be far from very low levels.

The same could be said for product inventories across the globe. Elevated crack spreads are a sign that despite higher refinery throughput in the coming weeks/months, the world still doesn’t have enough products. You can see this in the price action in the spreads.